Print and read offline instead.

- Fine wine saw a strong end to the third quarter as equities faltered.

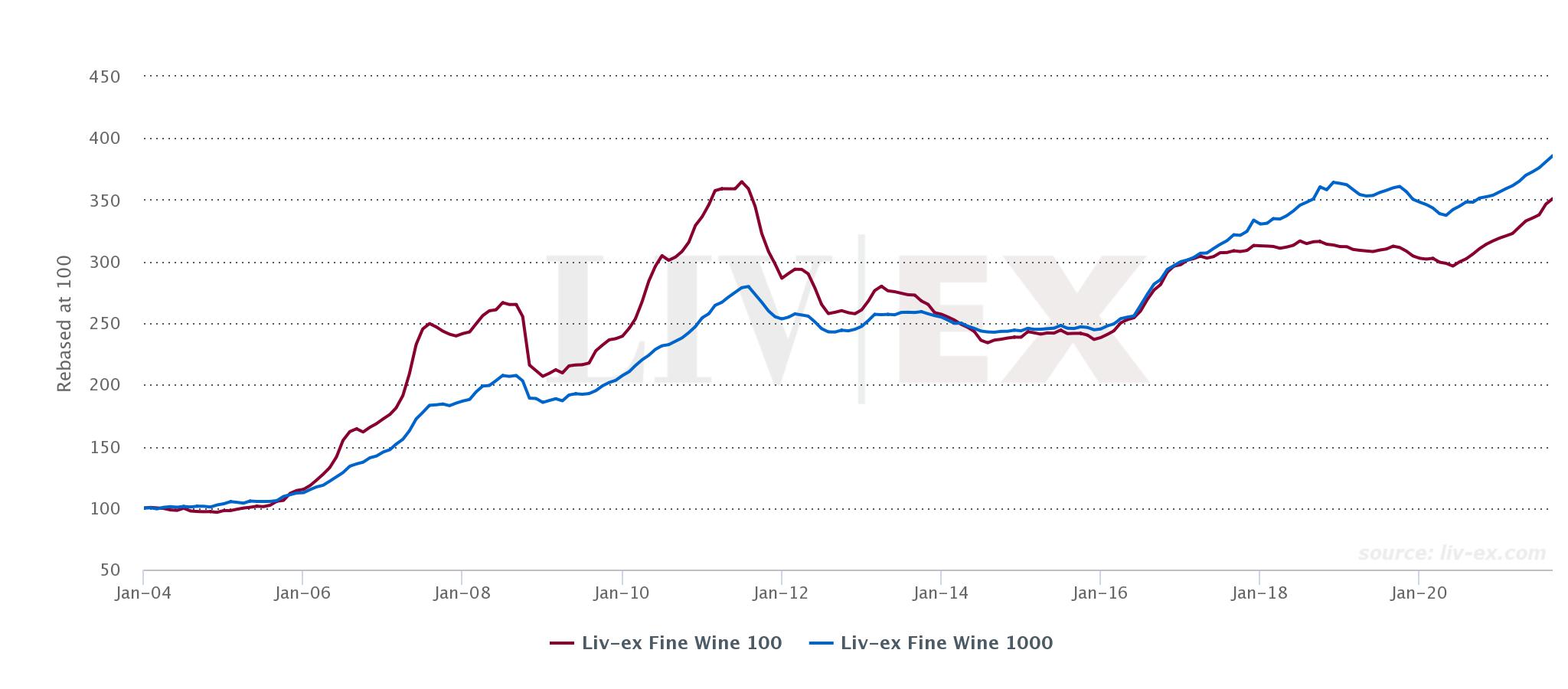

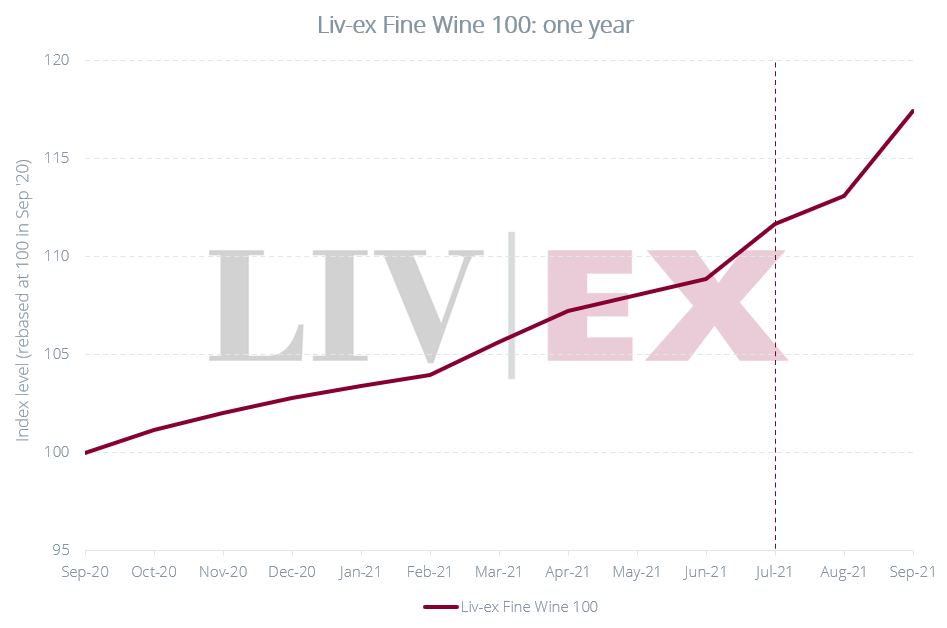

- The Liv-ex Fine Wine 100 ended Q3 just shy of its previous record of June 2011.

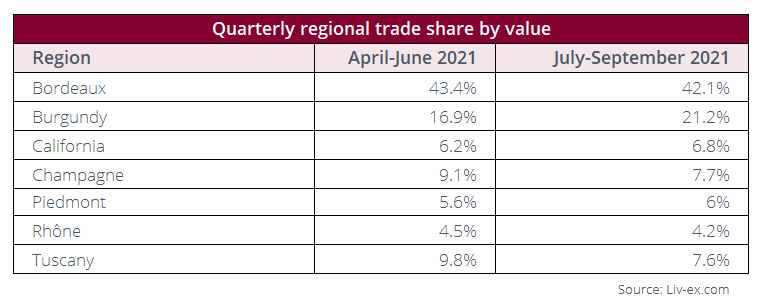

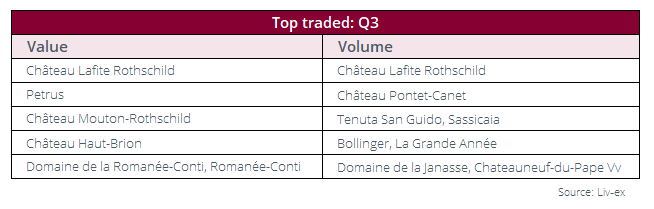

- Lafite Rothschild was the top traded wine by value this quarter.

- The Burgundy 150 and Champagne 50 were the best-performing sub-indices of the Liv-ex Fine Wine 1000

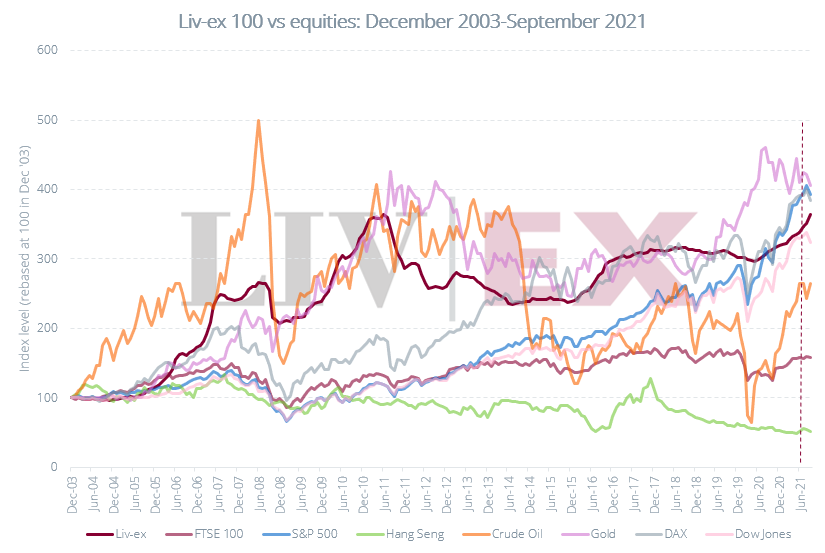

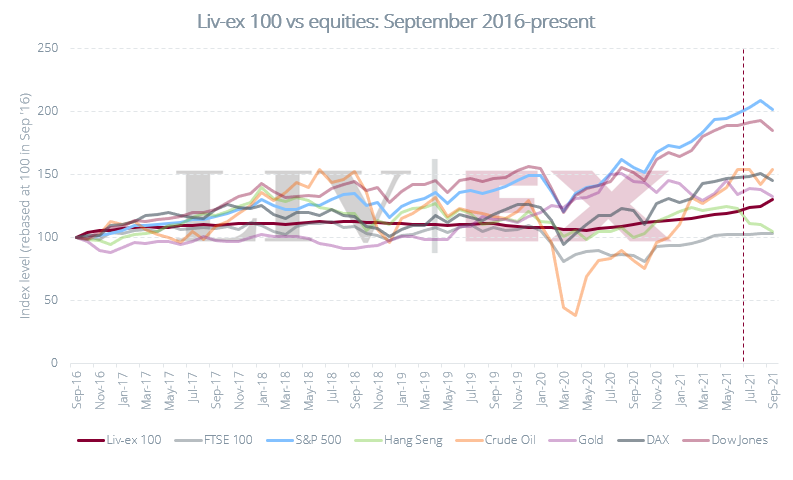

September was a bad month for equities as the third quarter of the year drew to a close. The S&P 500 was down 4.8%, its worst month since March 2020 when the pandemic began to bite.

September was a bad month for equities as the third quarter of the year drew to a close. The S&P 500 was down 4.8%, its worst month since March 2020 when the pandemic began to bite.

Rising interest rates (signaled by a weaker bond market) stoked by inflation fears (the result of supply chain issues) coupled with concerns about China’s indebted property market spooked investors in the mainstream markets but fine wine prices, remained robust. The key market indices, the Liv-ex Fine Wine 100 and Liv-ex Fine Wine 1000 have recovered strongly since the shock of Covid-19 in the first half of 2020 and are now at or near record levels.

The key market indices, the Liv-ex Fine Wine 100 and Liv-ex Fine Wine 1000 have recovered strongly since the shock of Covid-19 in the first half of 2020 and are now at or near record levels.

September saw the Liv-ex 100 cap off a decade of recovery by returning to its former peak. In June 2011 the index hit a record height of 364.69 before falling steeply as the previously bullish Chinese market unwound. In September 2021 it rose 3.8% to reach 364.44 – within a hair’s breadth of its peak.

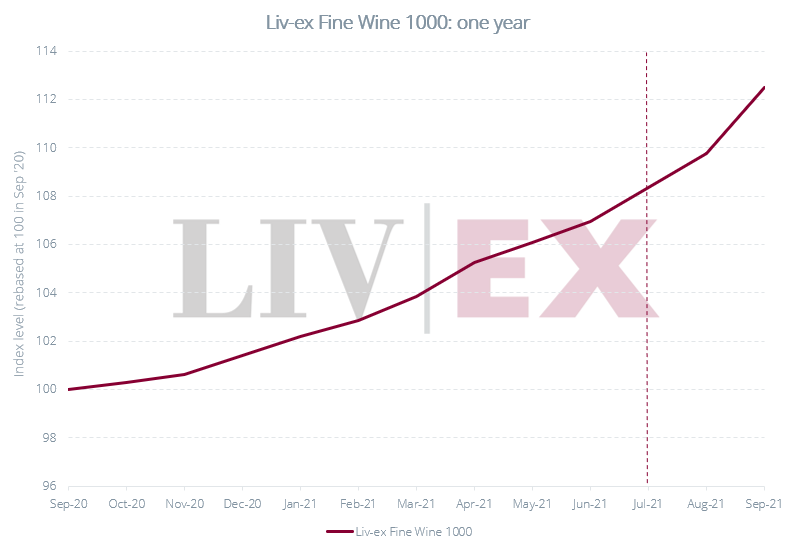

The Liv-ex 1000, the broadest measure of the market, posted its eighth consecutive month of gains to close at 395.36

made using the Liv-ex charting tool

Bordeaux saw a small decline in its share of total trade by value in the third quarter while Burgundy gained between Q2 and Q3. The number of Burgundy wines traded year to date has already surpassed the number traded in the whole of 2020, reflecting the continued broadening of the wider market.

Champagne’s trade share by value dropped in the third quarter but this belies the underlying positive sentiment – it was the second best-performing sub-index of the Liv-ex 1000 between July and September.

Indeed the quarter should be viewed in the context of the increasingly ‘unique’ nature of September – a month now dominated by an increasingly eclectic mix of en primeur releases via La Place in Bordeaux.

This year there were close to 40 wines released through La Place. Over a dozen of these were brand new additions to the distribution platform, from both Old and New World regions. These included Penfolds Bin 169, Yjar, Casa Real, Philipponnat’s Clos des Goisses, Daou Family Vineyards ‘Soul of a Lion’ and Castel Giocondo. You can read our recap of the campaign here.

Liv-ex 50

Performance

Performance

Q3: 6.6%

Year-to-date: 11.6%

One year: 14.1%

The Fine Wine 50 tracks the progress of the Bordeaux First Growths (Lafite Rothschild, Mouton-Rothschild, Haut-Brion, Margaux and Latour).

It rose almost 7% over the third quarter, buoyed by strong demand for an old market favourite, Château Lafite; which saw strong trade for multiple vintages, particularly the 2018, 2017 and 2015. The 2018 Lafite is currently the most traded wine by value so far this year.

Liv-ex 100

Performance

Performance

Q3: 7.8%

Year-to-date: 14.2%

One year: 17.4%

Up 3.8% in September and 7.8% overall in the 3Q, the benchmark index (which tracks the 100 most traded wines in the secondary market) has almost fully recovered from the shock of 2011, when the China-driven Bordeaux bubble popped.

Since then, the fine wine market has broadened considerably and become far less volatile. The strong performance of its constituent Italian, Burgundian and Champagne components, as well as the more recent rally in the First Growths has seen it recover all the lost ground of those post bubble years.

Liv-ex 1000

Performance

Q3: 5%

Year-to-date: 10.9%

One year: 12.4%

The Liv-ex 1000, the broadest measure of the fine wine market tracking wines from Bordeaux to Australia, bears witness to the huge shift in buying patterns over the last 10 years.

As collectors began switching to Burgundy, then Champagne and more recently, Italian, Californian and Rhône labels, so the market swelled and the Fine Wine 1000 rose.

It currently sits at an all-time high.

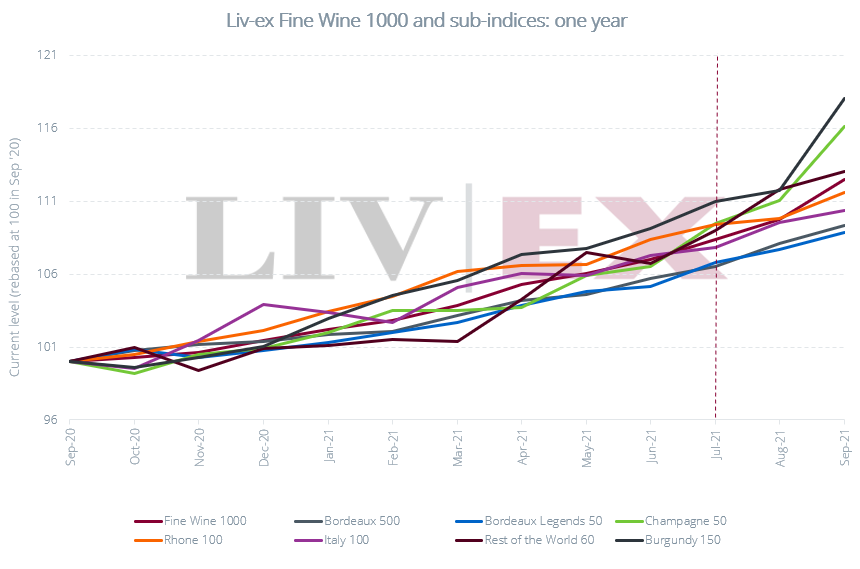

Liv-ex sub-indices

The Liv-ex 1000 is composed of seven sub-indices, covering the key fine wine producing regions and countries of the world.

Burgundy (especially renewed trade in Domaine de la Romanée-Conti) and Champagne were the main drivers of its performance in Q3, but all regions put in solid performances.

The Burgundy 150 is currently the strongest sub-index on the year-to-date (up 16.8%) and over one year (18%), followed by the Champagne 50, Rest of the World 60, Rhone 100 and Italy 100 over the same periods.

Conclusion

Conclusion

Despite appearances, the third quarter of 2021 perhaps leaves the fine wine market with more questions than answers.

The quarter began in the wake of an En Primeur campaign that never quite found its footing but still gave focus to Bordeaux. This was followed by a subdued trading period in August – the unlocking of Europe allowing collectors and merchants alike to finally escape from their desks.

After a pronounced summer lull, September trade came roaring out of the blocks. It was this final month of the quarter that pushed the market to new highs.

Amid all the releases from La Place that dominate September, the real activity was focused on the blue-chip names from the world’s leading wine regions.

Although the Liv-ex 1000 reached yet another record, it was the old warhorse, the Liv-ex 100, which emerged as the best-performing single index of the quarter. In fact it is the best-performing of the main indices both year-to-date and over 12 months.

As financial markets wobbled in September (rather earlier than the traditionally turbulent October patch) the blue-chip index took centre stage in what could be seen as a flight to quality. There is no doubt the market is in a bullish mood, but with macro-economic ill winds swirling through bond, equity and commodity markets, the final quarter of the year might prove the most interesting yet for the fine wine market.

Members of Liv-ex can explore the new charting tool here.

Non-members of Liv-ex can learn more and request a demo here.