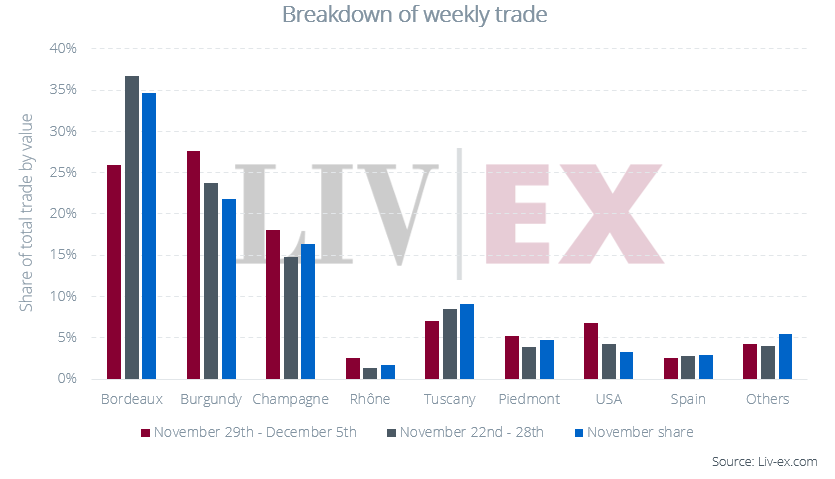

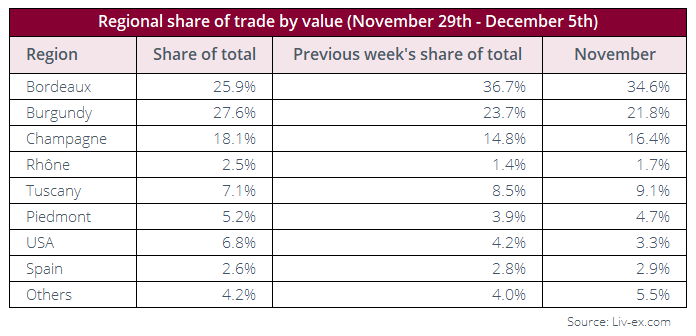

- Burgundy lead the market with a 27.6% share of traded value, followed by Bordeaux with 25.9% and Champagne with 18.1%.

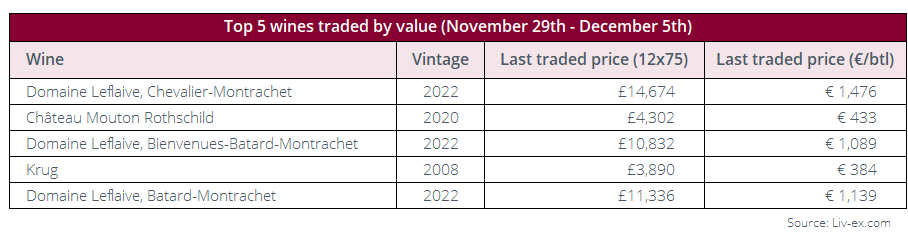

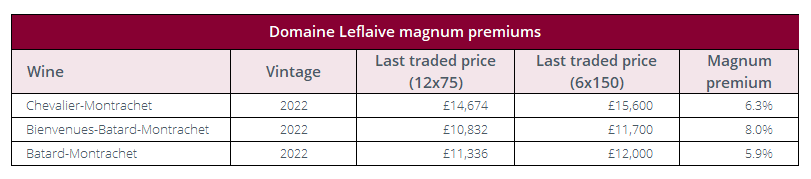

- Three 2022s from Domaine Leflaive were amongst the top-traded wines by value.

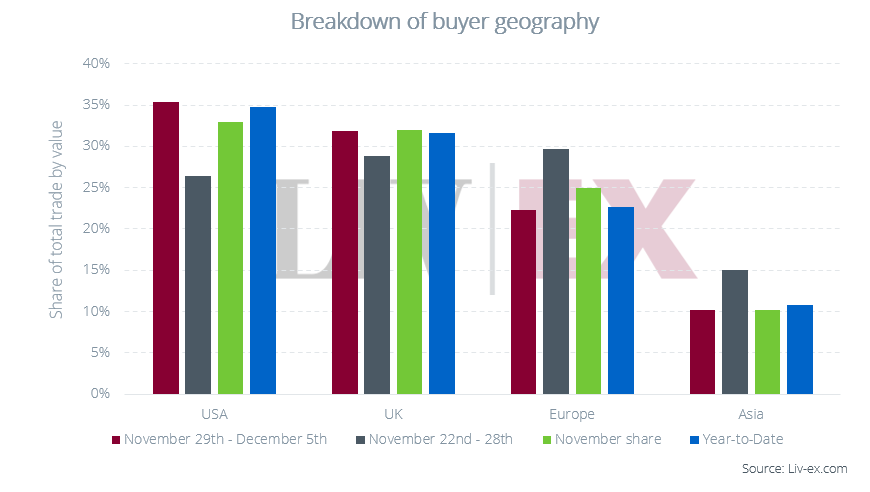

- Post thanksgiving, US buyers have returned to the market, with European and Asian buyers less dominant than last week.

- This week, Liv-ex published its annual update of the Power 100 – a list and analysis of the most influential brands in the wine industry, considering factors such as price performance and trading activity.

With a 27.6% share of traded value, Burgundy has overtaken Bordeaux to lead the market. This has been largely driven by trades of Domaine Leflaive’s 2022s (further analysis below).

Champagne enjoyed a strong week, taking an 18.1% share of the market. While Krug 2008 was the only champagne to appear amongst the top five wines by traded value, the region dominated the top five by volume. In previous years, Champagne has seen an uptick in trade in the months leading up to Christmas and New Year. As with trade in general, volumes generally fall slightly towards the middle and end of December as many in the industry take time away.

While Château Mouton Rothschild 2020 featured amongst the top five wines by traded value, Château Lafite Rothschild was the top traded producer overall. Alongside trades of the more recent vintages of the Grand Vin (such as the 2019, 2018, 2017, 2014 and 2010), the 2000, 1986 and 1970 vintages also changed hands.

The US had a strong week, up from its close at 4.2% last week to 6.8% this week. While trade of Screaming Eagle has been relatively quiet in recent weeks, several vintages of the flagship Oakville Cabernet Sauvignon saw trade this week, including the 2018, 2020 and 2021.

In the realm of spirits, Glenfarclas, The Family Casks S21 (Sherry Butt Single Cask No 13007 Bottled 2021) traded several times, at around £485 per 70cl bottle.

Breakdown of buyer geography

Following several weeks of inconsistent trading from US buyers – presumably a consequence of focus shifting to the election and, last week, thanksgiving – they have returned to their YTD purchasing share of c.35%.

European and Asian buyers took a back seat this week, while UK buyers held strong with a 32% share.

What were the week’s top-traded wines?

Three Domaine Leflaive 2022s were amongst the top five wines by traded value, with the Chevalier-Montrachet taking the top spot. All three traded in both regular and magnum formats (premiums shown below). While Burgundy more recently has suffered as the consequence of sometimes opportunistic price inflation combined with robust release prices, these three Leflaives all traded above their ex-London release prices.

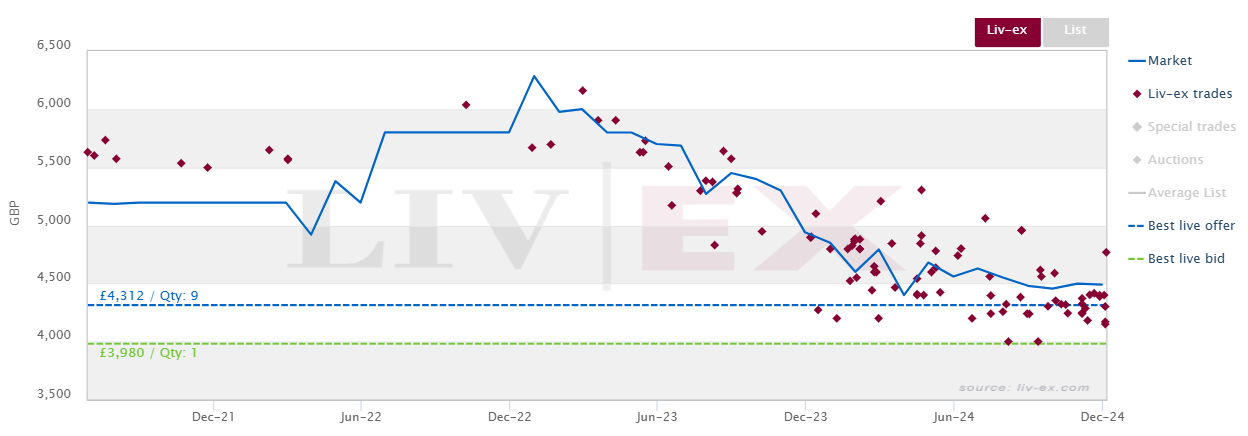

Château Mouton Rothschild 2020 featured amongst the top five by value for the second week running. Prices have remained fairly stable since the start of the year, trades taking place this week around £4,200 per 12×75. The recent sustained uptick in trade volumes without significant upward or downward price movement suggests a market comfortable at the current price (down 15% on UK release).

Liv-ex trades of Château Mouton Rothschild 2020

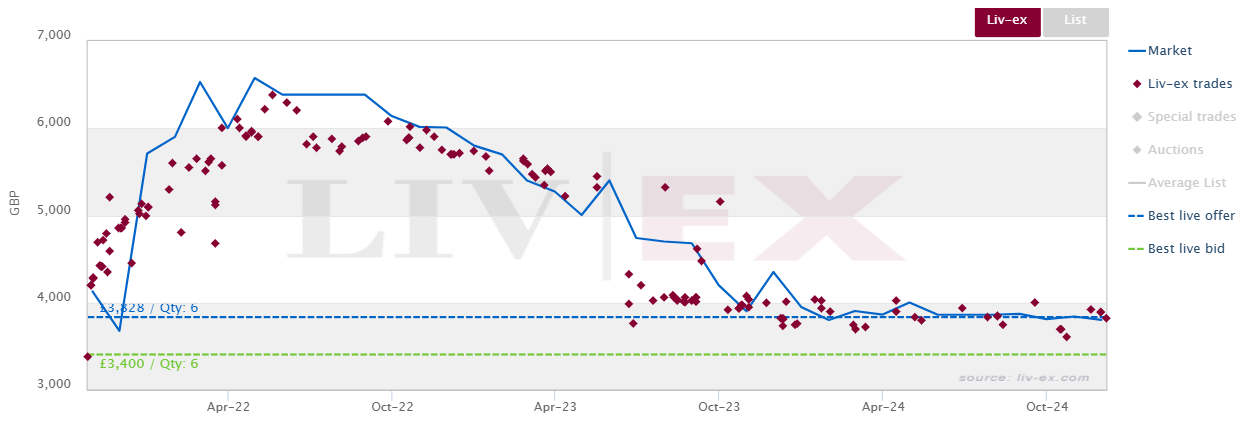

Krug 2008 came in as the fourth top-traded wine by value. Both its Market Price and trade prices have been remarkably stable since October 2023. This week, it traded in high volumes at £1,910 per 12×75 and, in low volumes, at £1,945.

Liv-ex trades of Krug 2008

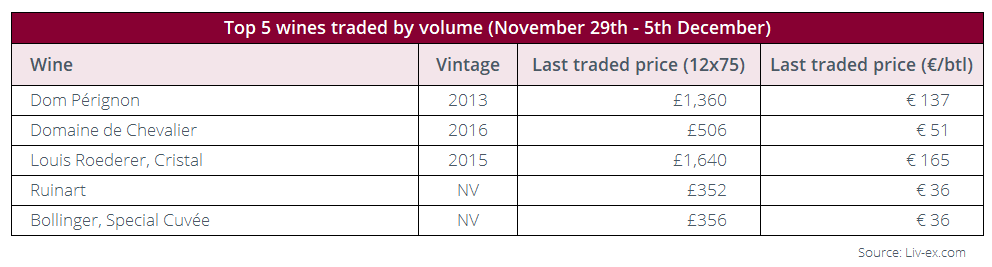

Top-traded wines by volume

Champagne dominated the top traded wines by volume, with Dom Pérignon 2013, Louis Roederer’s Cristal 2015, Ruinart NV and Bollinger Special Cuvee all featuring. Cristal 2015 has featured amongst the top five by both traded value and volume for the past three weeks, but this week has traded slightly less actively, its transaction prices decreasing from c.£1,730 to c.£1,670.

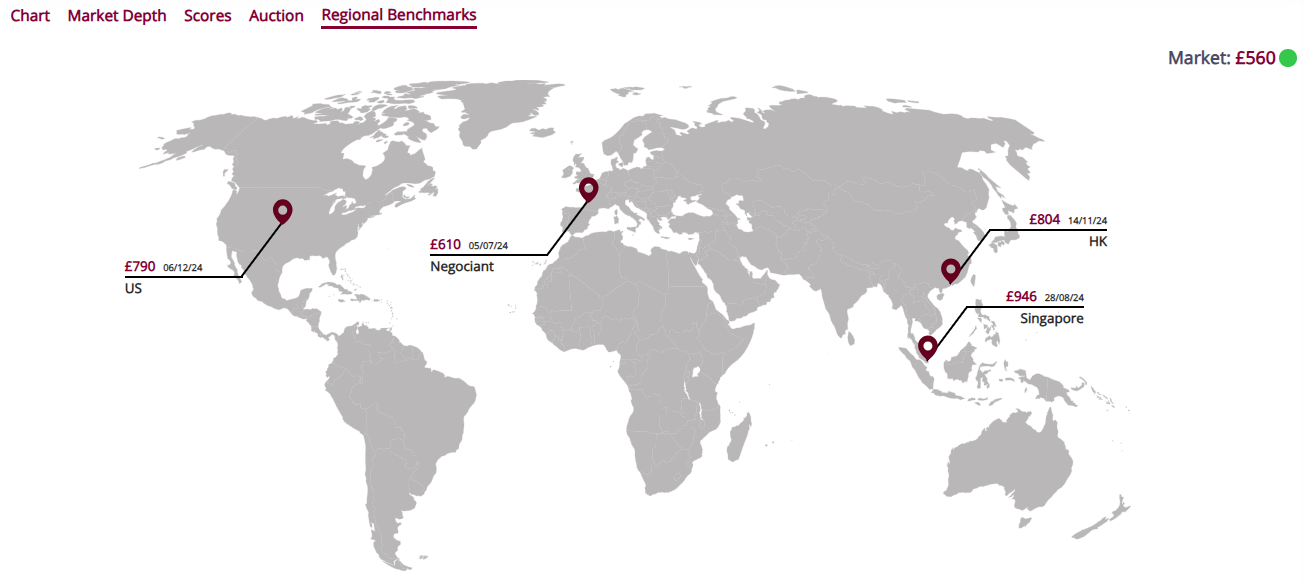

Domaine de Chevalier 2016 came in as second top-traded wine of the week by volume. It changed hands at £506 per 12×75, 9.5% below its Market Price of £560 and 20% below its international release price. Receiving 96 points from Lisa Perrotti Brown MW (The Wine Independent) and 97 from both Neal Martin (Vinous) and Jeb Dunnuck, buyers are recognising value. Regional Benchmarks in Hong Kong, the US and Singapore are a decent clip higher.

Regional Benchmarks of Domaine de Chevalier 2016

Weekly insights recap

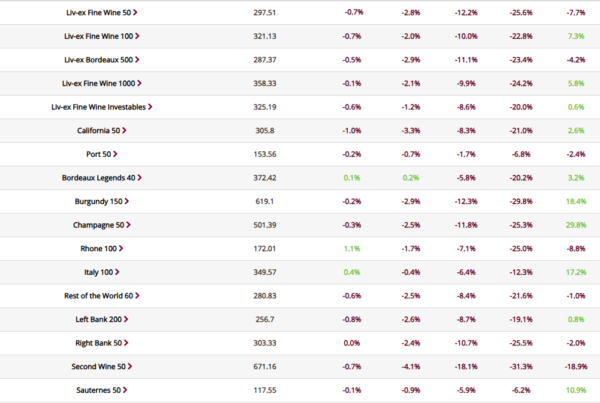

This week, Liv-ex published its annual update of the Power 100 – a list and analysis of the most powerful and influential brands in the wine industry, considering factors such as price performance and trading activity. A free copy is available here. Members were sent an additional analysis of the Power 100’s top 10 by traded value and volume. An update on the movements of Liv-ex’s major indices over the course of November was also published and is available for all to read here.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £140m of bids and offers across 20,000 wines.

Independent data, direct from the market.