What’s happening in the market?

Though down from its close at a 39.1% share of trade value last week, Bordeaux has continued to lead the market this week. Château Mouton Rothschild and Château Lafite Rothschild have traded most actively, with several vintages of each changing hands.

Thanks in part to high volume trades of Taittinger, Comtes de Champagne Blanc de Blancs 2013 and Dom Pérignon 2008, Champagne has largely recovered from its weak close last week, up from 8.6% to 14.0%.

Tuscany has performed well so far this week, taking a 16.2% share of traded value. While Super Tuscans drew the region to its strong close last week, Brunellos have since taken center stage, with Argiano 2018 and Biondi-Santi Riserva 2016 in the lead.

Today’s deep dive: when will list prices adjust to the market?

- Merchants are less responsive to downward than upward movement in the market.

- The difference between Average List Prices and Market Prices for the Liv-ex Fine Wine 50 is at an all-time high.

- Merchants are increasingly feeling the pressure to adjust prices to market conditions.

In an August Market Update, we noted that trading prices, Market Prices (best listed case price) and Average List Prices (a volume-weighted mean of EU and UK SIB listings) of Château Lafite Rothschild 2016 have been diverging since the turn of the market. To gain an understanding of the behavioral interactions between the primary and secondary market, we have conducted an analysis of the varying difference between Market Prices and Average List Prices of the Bordeaux First Growths over time. While the full analysis will later follow, an excerpt has been provided for today’s deep dive.

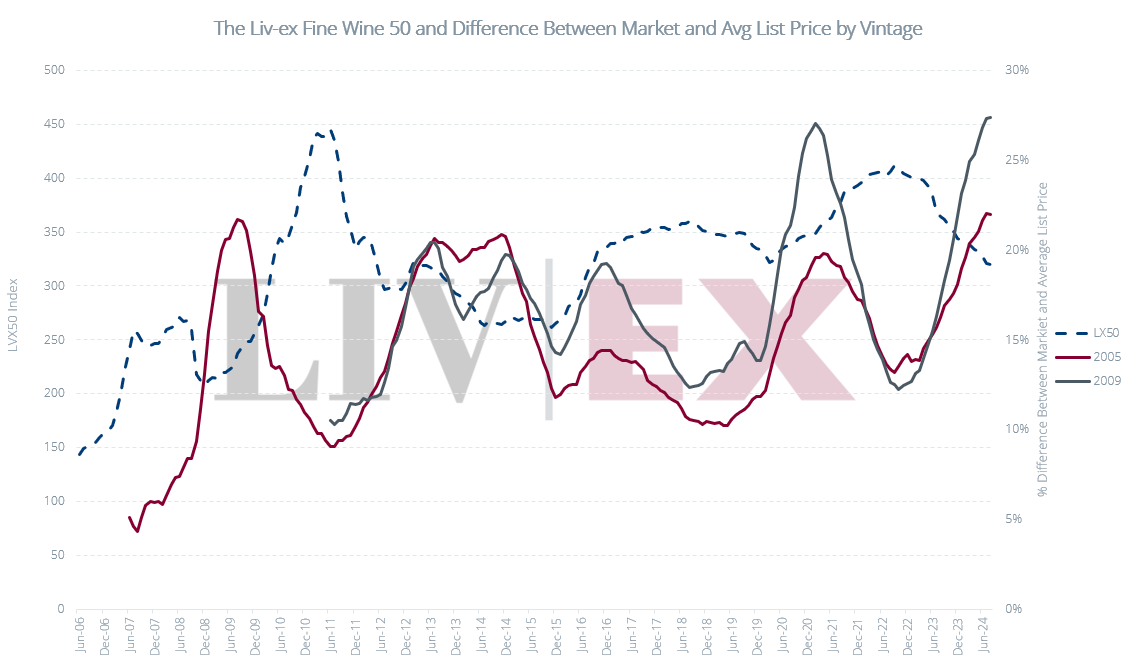

In the chart below, the Liv-ex Fine Wine 50 is represented by the dotted line. The average difference between Market Price and Average Listed Price for the 2005 and 2009 vintages of the First Growths (minus Château Latour) are represented by the burgundy and grey lines respectively. To capture broader trends rather than spikes, we have opted for a 3-month rolling average. In general, we observe an inverse relationship between the index and the price differential — in upward moving markets, the Average List Price falls closer to Market Price than in downward moving markets.

Merchants are less responsive to downward movement in the market than they are to upward movement. While understanding that the market is bearish, many will continue to list their stock at high prices. This is especially true now – the difference between Market Price and Average List Price is higher than ever across all vintages. At the peak of the market in April 2011, for example, the average list price for Lafite 2005 was 6% higher than the Market Price. By February 2013, the Average List Price sat 25% above market.

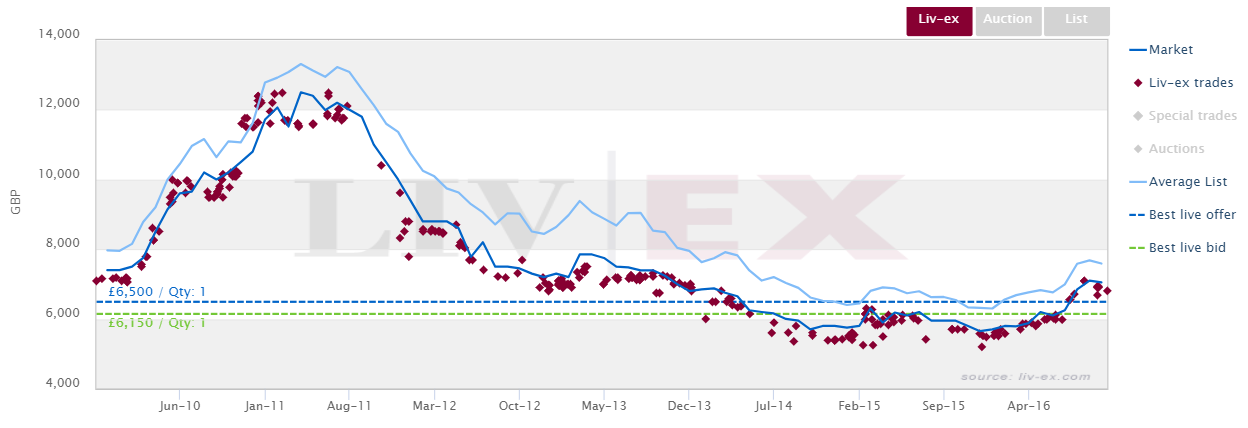

Liv-ex trades, Market Price and Average List Price of Lafite 2005

As shown in the chart above, while Average List Price of Lafite 2005 decreased between mid 2011 and late 2013, it did so less sharply than Market Price. Only when Market Price and Average List Price began to converge in February 2015 did the market show signs of recovery. With Market Prices falling in a down market, merchants are invariably eventually faced with enough competitive pressure to force their prices down. When prices on the primary market fall low enough to present value to buyers, demand will increase, thereby reinvigorating the secondary market.

The questions remain: when will merchants feel enough pressure to lower their prices, and how will the secondary market react? A full-length analysis of the current state of the market will be published by Liv-ex in the coming weeks.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.