Burgundy closed the first half of 2021 with 20.2% share of trade by value – its best start to a year ever.

Trade share for the region was helped by a rise in Burgundy Blue Chip prices (the Burgundy 150 is up 8% year-to-date) and a broadening of trade for high priced wines, which was highlighted in an April blog post.

- In H1 2021 the number of distinct Burgundian LWIN7s traded was up 54.4% against the first six months in 2020.

- Distinct LWIN7s traded for wines greater than or equal to £5,000 per 12, was up 81%.

- The number of wines with Market Prices over £100,000 (12×75) traded in 2021 is six times greater than in 2017.

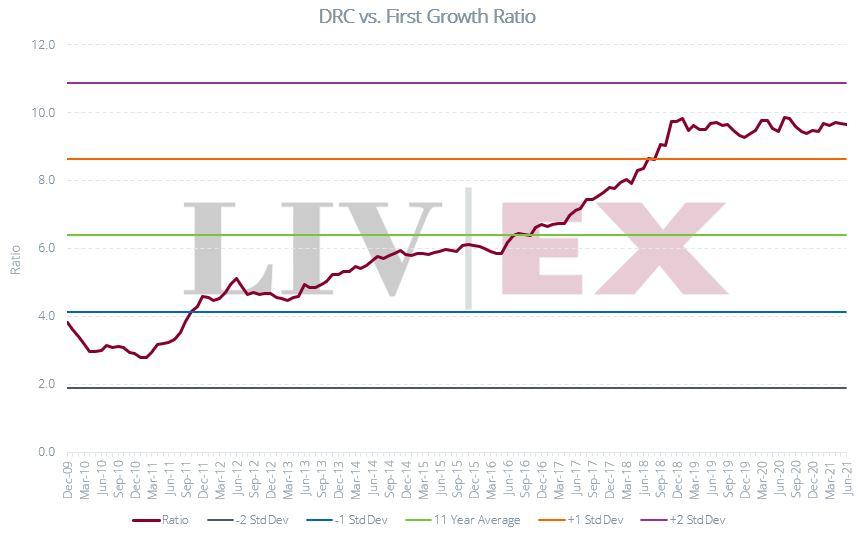

What about DRC?

The DRC to First Growth ratio, found by dividing the average price of the six wines in the DRC index by the Liv-ex Fine Wine 50, has been relatively stagnant since the end of 2019.

In November 2020, we pointed out that, “a breakthrough in the 10x upper resistance might point towards further movement but for now DRC seems to have found a plateau”.

That plateau has remained, but this does not take away from DRC’s continued price performance. The DRC index is up 10.9% over the last year, the wines are just no longer outperforming the First Growths, a trend we saw happen for nearly a decade.

Burgundy remains the high-priced corner of the fine wine market and although we saw a small stutter in 2020 (Burgundy 150 down 1%), the region has bounced back in 2021.

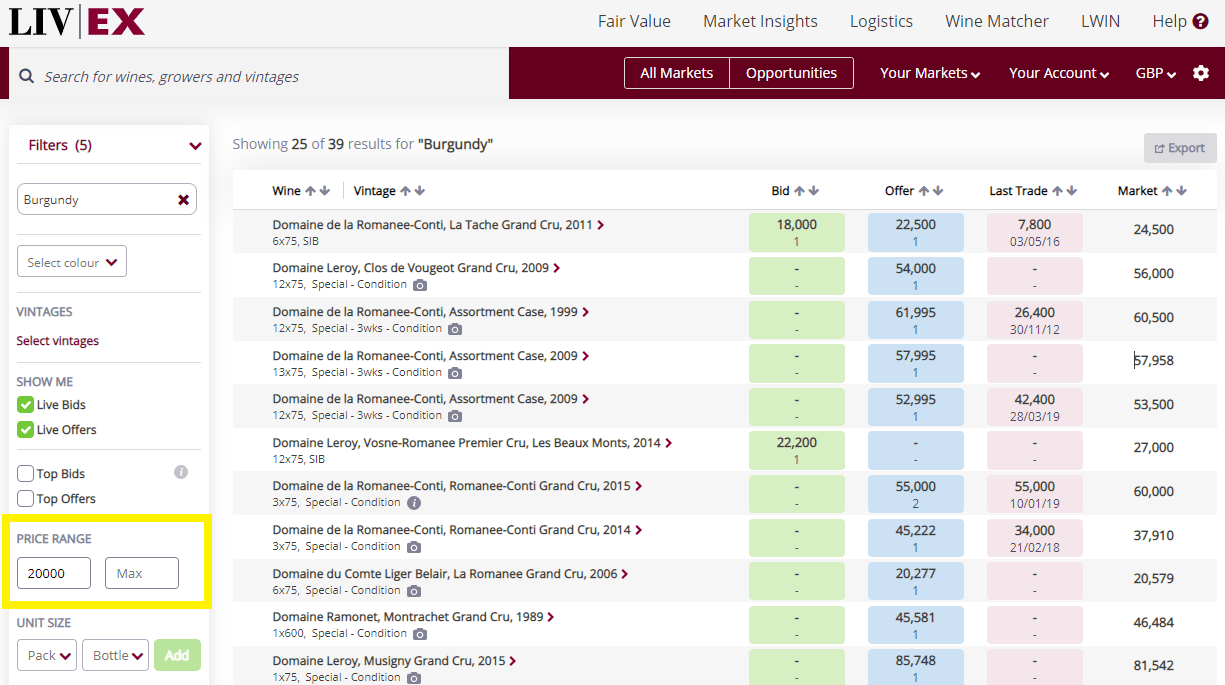

There are nearly 40 offers of Burgundy’s wines offered at a minimum of £20,000. If you’d like to change the minimum or maximum offer value, you can do that on the Filters side bar, seen in the screen capture below. Click on the exchange to search for your exact price bracket.