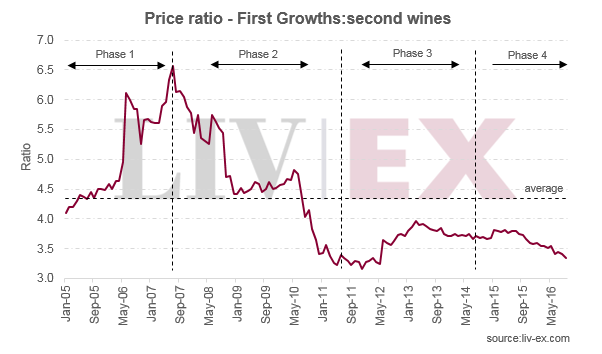

Back in July 2007, it was possible to buy 6.6 bottles of second wines – more than a standard six pack – for every bottle of the Grand Vin on average. That number now stands at half – 3.3.

The chart above shows the relationship between prices of First Growths and their second wines going back to 2005. This relationship has seen a number of phases. In the first, through to the end of the summer of 2007, “traditional” fine wine buyers from the UK and Europe were leading the market. Prices for First Growths were rising, but the brand appeal didn’t trickle down to their second wines, and the price gaps between the two groups broadened.

The second phase was characterised by the increased significance of Asian buyers in the fine wine market. A series of regulatory changes culminated in the complete removal of duties and tariffs on wine in Hong Kong in February 2008 – a major catalyst for Asian investment in the sector.

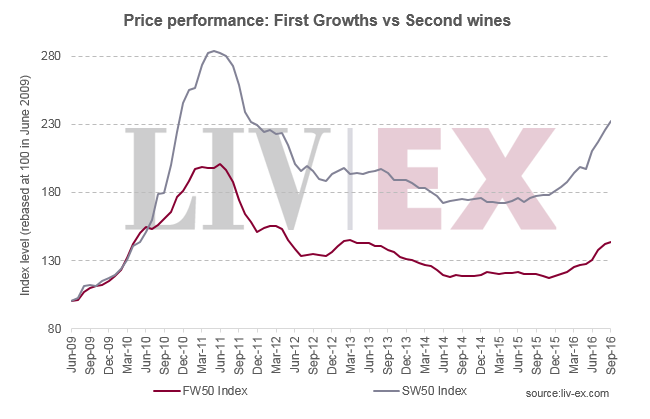

At this time, Chinese brand buying began to push Bordeaux prices higher, with First Growths and their second wines in focus. As prices for Lafite Rothschild and its peers reached dizzying heights, the second wines increasingly looked more attractive as entry levels to these popular brands at much lower price points. As the chart below shows, by mid-2010 the second wines were skyrocketing. Between June 2009 and June 2011, the Liv-ex Fine Wine 50 index – representing price movements of the First Growths – increased by 101%. The Second Wines 50 index soared 183%. By December 2011, first wines were just 3.2 times higher than their second wines on average.

The third phase marked a period of market decline, but the price gap began to creep higher. Prices for both groups dipped – the second wines a little further as mainland China all but abandoned the market. The market bottomed in July 2014.

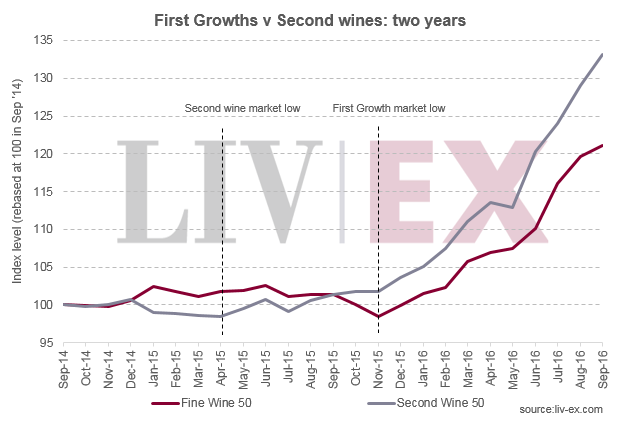

The Bordeaux market has recently seen another boost. Once again, the second wines of the Bordeaux First Growths have been among the top performers. The Second Wines 50 index has gained 28.5% year to date* compared to a 21.3% move for the Fine Wine 50. The broader Bordeaux 500 index is up 17.7% over the same period. Their strong showing has once again been linked to Asian brand buying which has become increasingly powerful with Sterling weakened.

The average price of a First Growth is now 3.3 times the average price of a second wine. As the first chart shows, this number is dropping – but for how long?

*end Dec 2015-end Sep 2016.

[mc4wp_form id=”18204″]