The Fine Wine 100

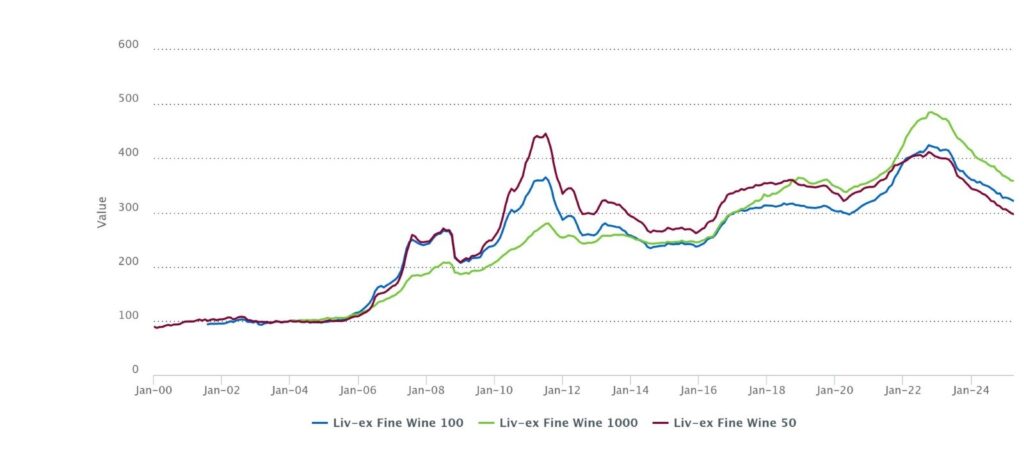

The Liv-ex Fine Wine 100, the industry leading benchmark, fell 0.7% in March, closing at 321. Domaine Trapet Pere et Fils’ Chambertin 2020 and Bartolo Mascarello’s Barolo 2019 were the index’s best performers, up 12.5% and 8.5% month-on-month respectively. Clos de Tart 2016 and Château Mouton Rothschild 2016 were the index‘s worst performers, down 12.2% and 9.1% respectively.

The Fine Wine 1000 and sub-indices

Looking at the wider market, the Liv-ex Fine Wine 1000 (which tracks 1,000 wines from across the world), fell 0.1% in March. Château Suduiraut 2021 is the index’s best performer, up 27.2% month-on-month. While the 2021 vintage was not a winner for still reds (receiving a recent slamming from Jancis Robinson via the Financial Times), the damp and cool weather proved beneficial for Sauternes. Still, they were not exempt from the effects of frost and hail in the early spring: yields were very low. This combination of low yield and high quality has likely been helpful in driving Suduiraut 2021’s promising price performance. At the bottom of the list comes Soldera Case Basse, 100% Sangiovese 2011, down 23.4% month-on-month.

The Rhône 100 was up 1.1% in March, making it the best performing index. Over a five year period, however, it is one of the worst performing indices, second only to the Second Wine 50.

The Italy 100 saw a 0.4% month-on-month increase. Though not immune to market conditions, the index has been a beacon of stability through the downturn, its long-term trendline still very much intact. This month, it was Barolos that performed best, with Bruno Giacosa’s Falletto le Roche 2001 and 2003, and Giacomo Conterno’s Monfortino Riserva 2002 up 12.4%, 11.8% and 10.9% respectively.

The Bordeaux Legends 40 rose slightly (0.1%) this month. This is in contrast to the falls of the Bordeaux 500’s sub-indices, likely as a product of recent vintages facing corrective phases following too-high release pricing.

The Bordeaux 500 and subindices

The Bordeaux 500, which tracks the 10 most recent physical vintages of 50 of Bordeaux’s top châteaux, fell 0.5% in March. 200 components saw price increases, 234, including nine vintages of both La Mission Haut-Brion and Château Lafite Rothschild saw declines and the remaining 66 fell flat.

The Bordeaux indices are continuing to fall, but a number of components are approaching or bouncing from key support levels. Cheval Blanc 2016, up 6.7% month-on-month, provides such an example.

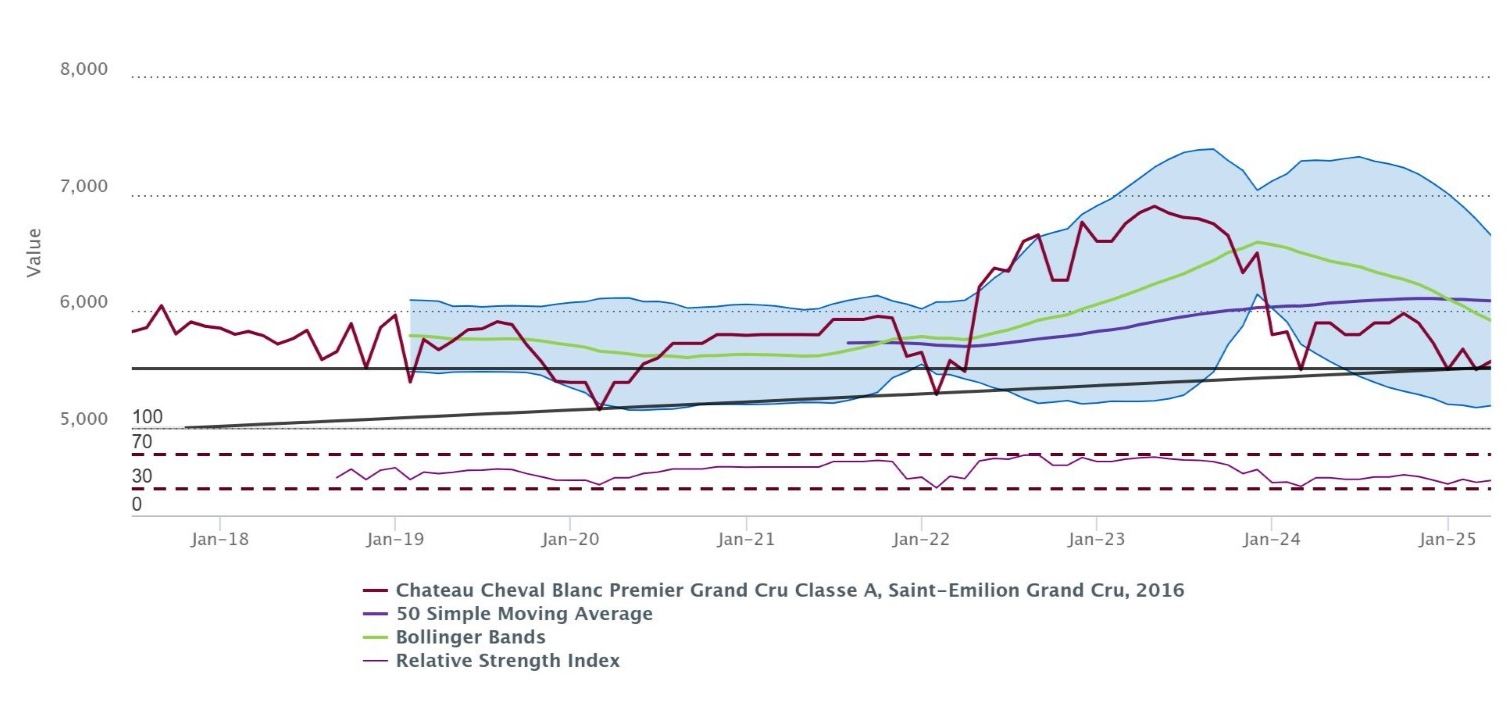

Technical analysis of Cheval Blanc 2016

Technical analysis presents a promising outlook for Cheval Blanc 2016. Its Market Price has recently bounced twice at the convergence of its horizontal support (2024 low) and long-term trendline, forming a double bottom pattern. Moreover, a weak bullish divergence has arisen between its price and Relative Strength index (a slightly lower low for the index and a higher low for the RSI in February this year). Paired with decreasing volatility, as indicated by the narrowing Bollinger Bands, a breakout now appears likely. Historically, bullish divergences (as seen in March 2020 and March 2022) have been precursors to upward price movement for Cheval 2016.

Cheval 16 is not alone here. There are several Bordeaux 500 wines with prices reaching (and sustaining at / bouncing from) key support levels. Technically inclined readers may also take interest in Cheval Blanc 2019, Château Pichon Baron 2013, Château Duhart-Milon 2012, Château Lafleur 2015.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £140m of bids and offers across 20,000 wines.