What’s happening in the market?

With many from the trade (especially the Bordeaux-focused) attending En Primeur tasting week, the start to the week has been slow. Nevertheless, this has allowed for other regions to shine. The top-traded producers of the week so far are Domaine de la Romanee-Conti, Harlan Estate, Chateau Margaux, Henri Boillot and Vega Sicilia.

US wines are faring well this week, taking a 9.2% share of traded value. While US buyers remain cautious, their buying has picked up slightly.

Today’s deep dive: European demand

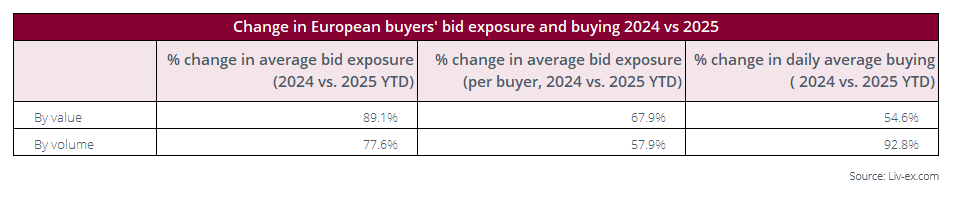

With US buyers taking a back seat for the time being, EU buyers have stepped up to the plate, accounting for 50.6% of traded value so far this month (up from 31.2% in Q1 2025). This is not purely a reflection of trade values dropping – daily average purchasing accounted for by EU buyers has increased by 22.7% over the same period.

EU buyers have been much more active on the exchange this year than last year. Their bid exposure – by both value and volume – has increased more than any other buying region.

European offer exposure has also seen significant increases. By volume, European offers are up 52.2% in April 2025 on April 2024.

French buyers

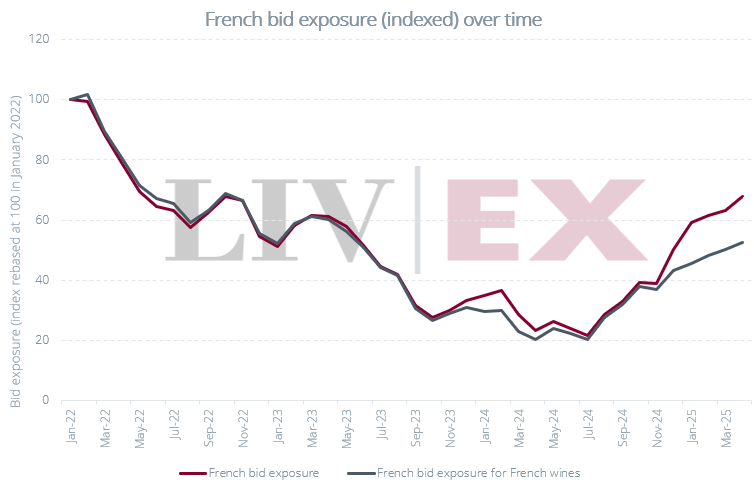

French buyers, who have accounted for more than a third of all European purchasing this year, have historically bought primarily French wines. While their scope has broadened somewhat — Italian wines are increasingly in demand — March nevertheless saw a c.90% increase in French purchases of French wine compared to February.

Prior to the imposition of tariffs earlier this month, we had identified a pattern of US buyers taking advantage of foreign exchange rates to acquire US wines at lower prices abroad than they would have been able to through domestic options. With the Euro gaining against both the US Dollar and Pound Sterling in April, this may be the case here. This, however, is a recent development. French bid exposure rose through Q1 2025 despite USD and GBP strengthening against the Euro.