What’s happening in the market?

US buyers’ share of the market has continued to decline following tariff announcements. Between Friday and Wednesday, they have accounted for only 8.0% of purchasing – down from 30.0% for Q1 this year. Champagne – often propped up by US buyers – is already suffering, taking a 6.8% share of traded value so far this week.

Comte Georges de Vogue is the top-traded brand of the week so far, followed by Château Lafite Rothschild and Château Mouton Rothschild.

Today’s deep dive: where is the demand?

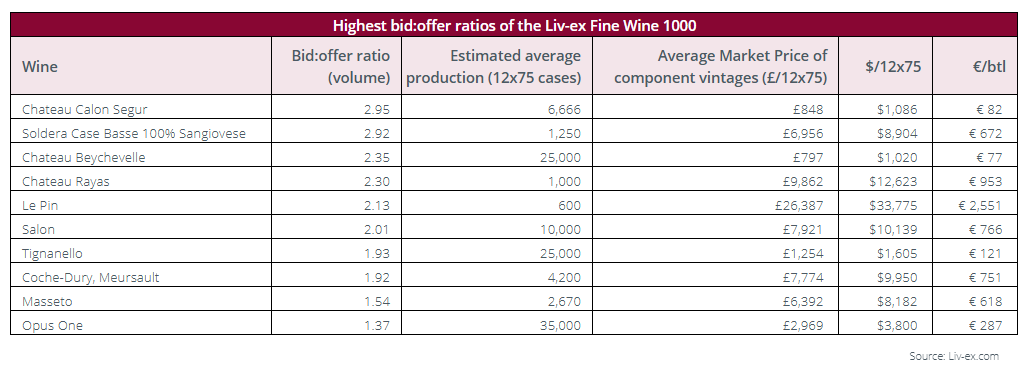

Bid:offer ratios can provide some insight into the demand-supply balance for indices and wines. It is no secret that we are in a buyer’s market. Sellers are increasingly willing to reduce prices, and they by far outnumber buyers. As such, bid:offer ratios, across the market, are very low. The Liv-ex 1000’s (by volume) sits at 0.64, down from a high of 4.61 in late 2021. Nevertheless, there are certain wines retaining a healthy balance. In a down market, what kinds of wines draw demand, and which are sellers reluctant to let go of?

The wines on this list fall into three separate camps (with some overlap):

1. Small production and high prices

2. Larger production and lower prices (relative to value)

3. Selectively allocated, or more difficult to come by

In Bordeaux, Château Calon Segur and Château Beychevelle head up the list. Both are priced under £1,000 per 12×75 and regularly receive scores in excess of 94 points. This appears to be a sweet spot for Bordeaux buyers in this difficult market. They are representative of the type of value Bordeaux used to offer – high quality wines produced in large volumes, available for relatively low prices. The prices of these wines have not been driven upward by brand name like those of the First Growths have been. Rather, their prices are justified by their quality.

Le Pin falls into both the 1st and 3rd camp – it is not an easy wine to come by, especially at its En Primeur release.

Tuscan wines are well represented. Soldera Case Basse and Masseto are both low production and known for their impressive quality. Tignanello, on the other hand, while receiving high scores, is produced in large quantities and is priced closer to Bordeaux’s Second Growths.

Château Rayas is notoriously tightly allocated, which has gone some way towards diminishing the volume offered on the secondary market, in turn driving up demand. Coche-Dury’s Meursault is a similar case.

While Salon and Opus One are produced in larger quantities, they are both cult names in their respective regions. Both are allocated (though not especially difficult to come by). It may strike readers as odd that Screaming Eagle does not feature. This is perhaps a case where prices have risen beyond a level that small production and tight allocation can justify.

Both high quality:price ratios and ‘hard to come by’ reputations can drive bid:offer ratios up. With an ever-increasing pool of options through which to source wines, however, ‘hard to come by’ might not hold true forever. Buyers and sellers looking for pockets of resilient demand might be better off looking for a healthy balance between quality, price and status.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £140m of bids and offers across 20,000 wines.