Bordeaux 2024 – a factory reset?

Introduction

In the run up to En Primeur 2024, news out of Bordeaux has been resoundingly negative — demand waning, generic vines being pulled, less wealthy châteaux closing their doors and, most recently, a hefty 20% tariff on US exports. In an unfortunate turn of pathetic fallacy, growers were met with the wettest year since 1992. And yet, the market looks on hopefully — a damp growing season has afforded low yields and presumably middling quality, but there may, in this, be a silver lining.

Over the past decade, the En Primeur system has lost its way. It no longer serves its original purpose – to generate working capital for châteaux in return for an opportunity to buy their wines at their lowest-ever prices. Consistently, prices have been falling post release, leaving not just private collectors, but merchants and négociants in the red.

With the broader fine wine market continuing to decline – the Liv-ex 1000 down 24.1% over the past two years – participants in the En Primeur system can no longer afford any missteps. This year, prices will need to be attractive, or allocations will be left on the table. Relationships between the system’s participants, however strong and longstanding they might once have been, will not turn negative operating margins positive.

Last year, châteaux dropped their prices by 22.5% on average. While this made for good marketing material, these decreases were generally insufficient – there remained better-rated, ready-to-drink vintages available on the market. To increasingly savvy collectors, the 2023s were a hard sell, despite being cheaper than the 2022s. Moreover, with demand declining, there is no shortage of Bordeaux available once physical – buyers will almost certainly be able to obtain these wines at a later date, and, importantly, at lower prices.

This is not to say that buyers are turning away from Bordeaux altogether; it remains the single most important growing region. En Primeur used to be an exciting time, presenting serious opportunities. Bordeaux buyers want this campaign to be successful. For many merchants and négociants, the success of their business depends on it. Releasing the 2024s at the right prices will do more than reinvigorate the En Primeur system – it may be the catalyst needed to end the current market downturn.

Undoubtedly, bringing ex-château prices down will make for lower margins. Just as the underwhelming 2013s allowed for châteaux to take a hit on a small vintage that was unlikely to perform well anyway, it is perhaps a blessing that the 2024 will not go down as one of the greats.

Bordeaux’s châteaux have again been presented with an opportunity to reset the market. Should they choose not to take it, the system may reach breaking point.

The fine wine market today

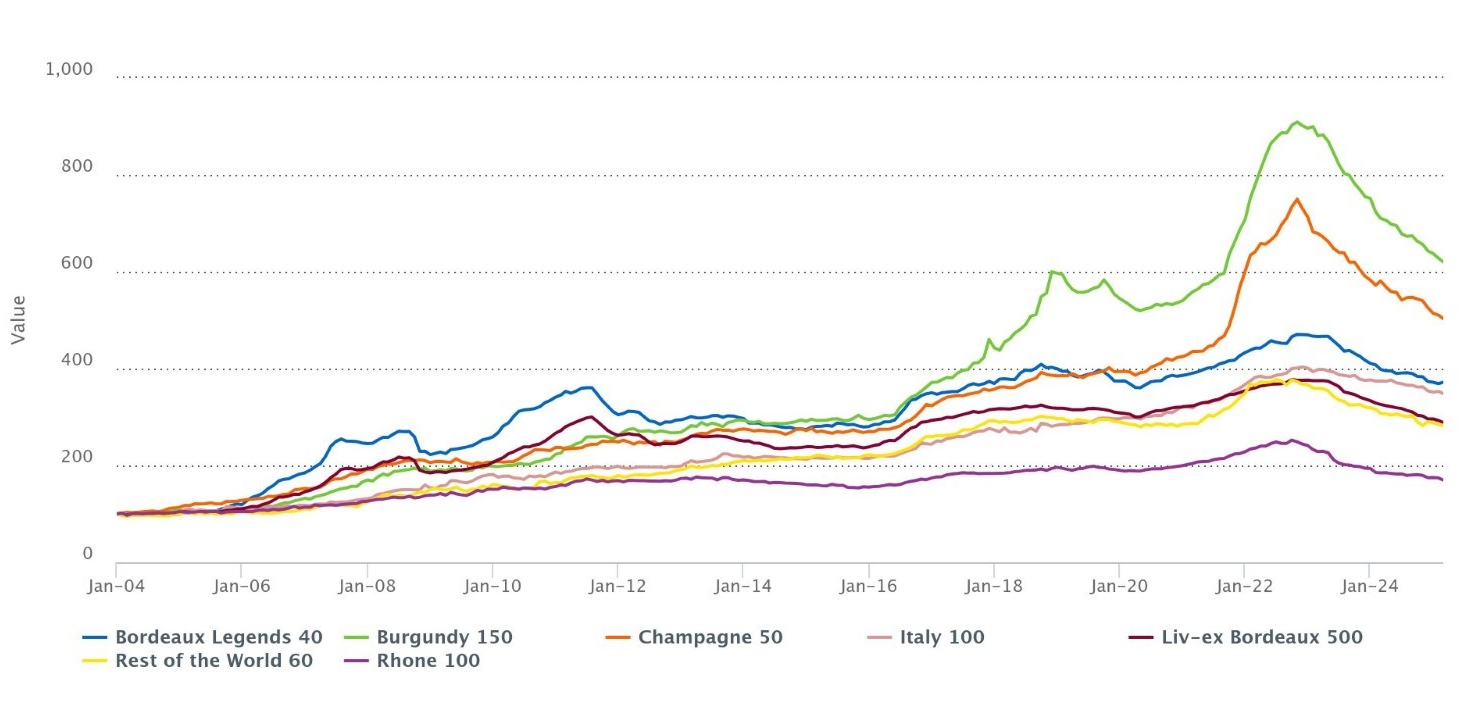

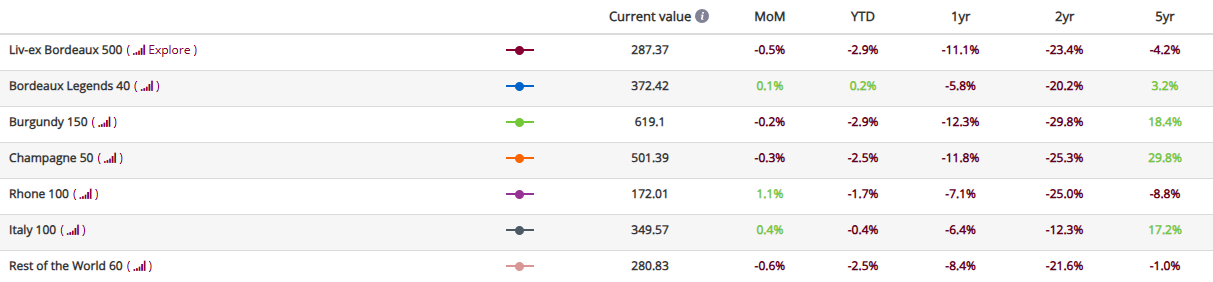

With the broader market well into its third consecutive year of a downturn, the Bordeaux 500 is by no means alone in recording a steady decline over the past few years. Prices across the regions have increased too far too fast for the market to absorb. While there remains hope that other indices will find support at their 2020 lows, however, the Bordeaux 500 crossed below this threshold in November 2024. Technical analysis would suggest that the index may find some support at its 2013 highs, 9.7% below its current level. Failing this, the next critical support, its 2015 low, sits an unsettling 9.1% further below.

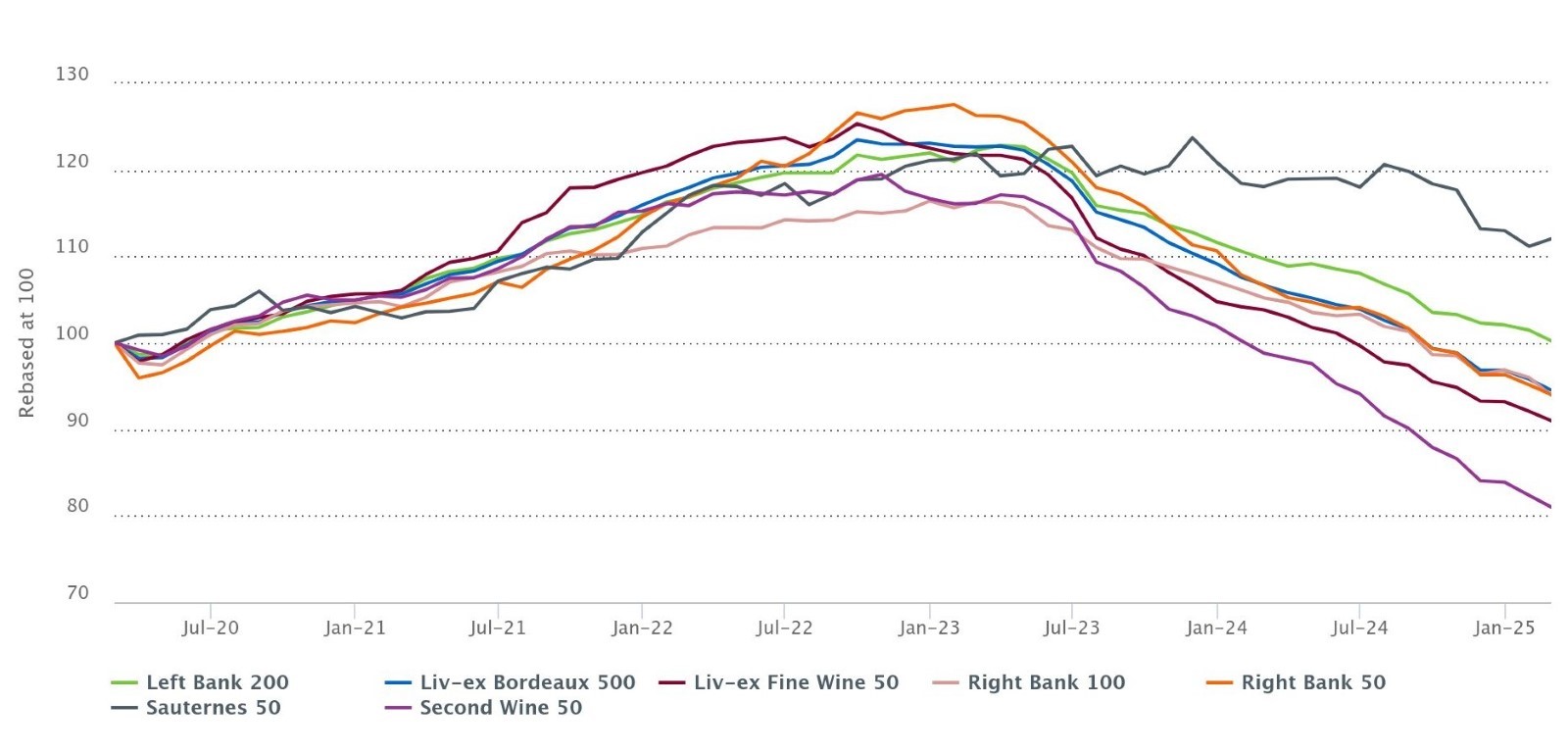

The Fine Wine 50, tracking the price movements of the 10 most recent physical vintages of the First Growths, is down 25.3% since March 2023 and has now decisively crossed below its 2020 lows.

The Second Wine 50 has taken the hardest hit over the past two years, down 30.2%. Its fall, relative to the comparative stability of the Sauternes 50 and Left Bank 200, highlights a growing sentiment amongst Bordeaux drinkers – they are less concerned with brand than they are with quality.

Though the Sauternes 50 appears the most stable, it is the worst performing Bordeaux index over the long term. Even now, the Bordeaux 500 is up 188.9% since its inception in 2003, while the Sauternes 50 is up only 17.7% over the same time frame. With Sauternes falling out of fashion and the production process very expensive, producers have been forced to pivot towards dry white wines.

Bordeaux has long been renowned for its singular ability to produce excellent wines in very high quantities. It is this high production that has historically allowed for Bordeaux to be more affordable, and crucially, more accessible, relative to regions such as Burgundy. Prices of the First Growths and their Second Wines have risen beyond a level most buyers can justify.

There is still value to be found in Bordeaux, however. We are seeing continued interest in the second, third, fourth and fifth growths. The Left Bank 200, the second best-performing sub-index over a two-year period, is representative of this pool of highly rated, lower-priced wines.

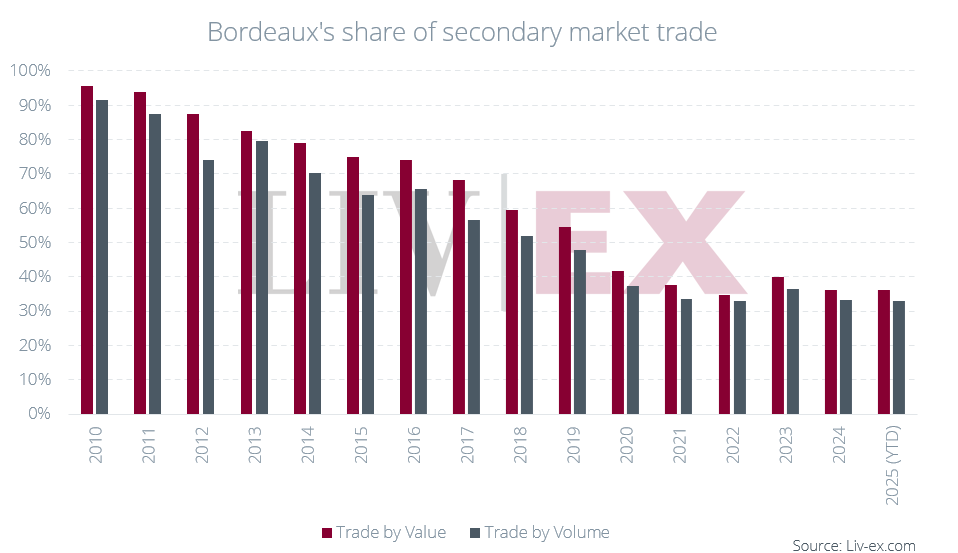

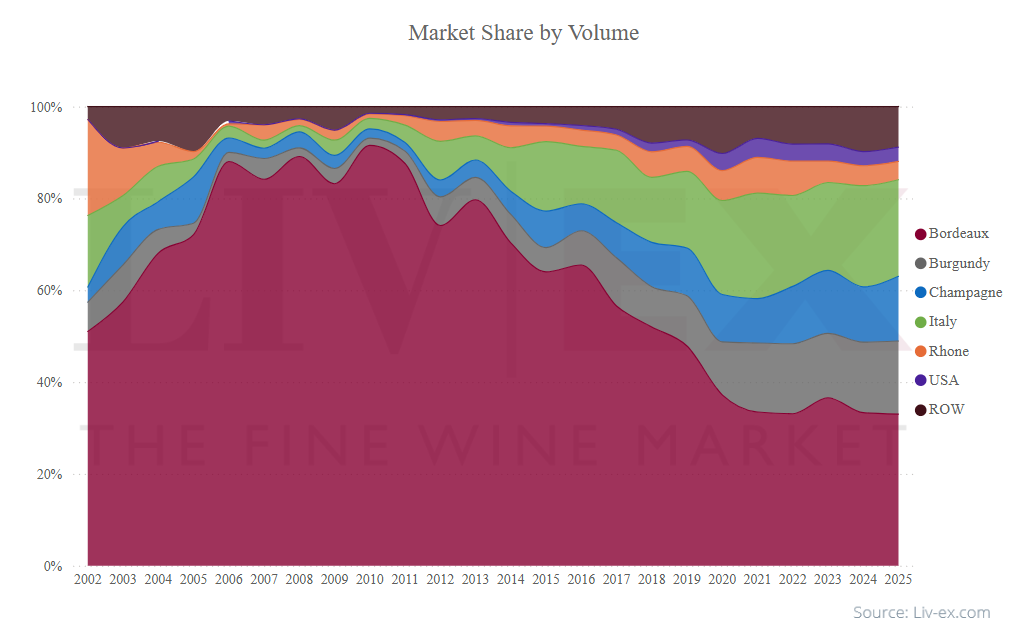

Bordeaux’s share of the market

Once accounting for over 90% of trade, Bordeaux’s dominance over the market has slipped. It remains the top-traded region, but now shares its stage with Burgundy, Champagne and Tuscany, amongst others. Until 2019, the First Growths (occasionally joined by Petrus) consistently comprised the annual top five brands by traded value. This year, Domaine de la Romanée-Conti and Dom Pérignon have joined their ranks, eclipsing Château Margaux, Château Latour and Château Haut-Brion.

Since 2020, Bordeaux’s share of the market has hovered between 30% and 40%, by both value and volume.

Who’s buying Bordeaux?

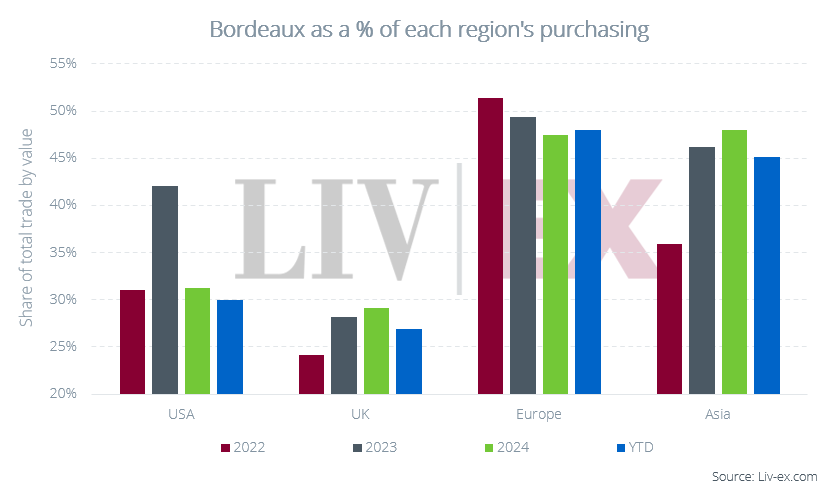

According to FEVS, French wine exports declined in 2024 for the second consecutive year. The value of exports of still wines to the US increased by 8.4% — an increase similarly reflected in our breakdown of buyer geography – while the value of wine exports to the UK saw a 3.9% decline. The report notes that, by volume, exports to the UK, increased by 5.4%. This discrepancy is, in part, explained by falling prices. On the secondary market, UK buyers increased their traded volumes of Bordeaux by 15.4% and decreased their traded value by 18.2% between 2023 and 2024.

European buyers’ share of Bordeaux purchasing fell between 2022-2024 but has risen to 41.4% year-to-date. This is not explained merely by the buying trends of other segments shifting away from Bordeaux. By volume, EU buyers purchased 14.6% more Bordeaux in Q1 2025 compared to Q1 2024. Historically, EU buyers have procured their wines domestically, buying from either négociants or châteaux. With the vast majority of Liv-ex’s European Bordeaux buyers hailing from France, it is possible that the increase in trade volumes is representative of a rejection of traditional purchasing avenues rather than of renewed interest in domestic wines. Year-to-date, French buyers alone have accounted for 26.2% of Bordeaux buying. Négociants, for whom ex-chateau purchasing was once the most profitable method of sourcing, are well-represented in this figure.

The UK market

UK buyers, holding steady with a c.25% share of the Bordeaux market from 2022-2024, have taken a back seat this year. This is representative of their buying habits overall – more than other regional segments, they have exercised caution.

The Asian market

Bordeaux makes up a large portion of Asian buying, but this share has been eroded since the early 2010s, peaking in 2011 at 95.5%, falling below 75% for the first time in 2017 and decisively breaking below 50% in 2021. Amongst Asian buyers, it is not a Lafite vintage, but Sassicaia 2020 in first place as the top-traded wine by value for the year so far. Bordeaux, which once monopolised Asian demand, now has strong competition.

The US market

While US buyers are generally less involved in En Primeur than UK buyers, they have played an increasingly important role in Bordeaux buying. The threat of tariffs should not be taken lightly. If, for example, tariffs reduce US spending on Bordeaux by 25%, the direct impact would be a c.6% reduction in traded value of Bordeaux. The indirect impacts, while harder to quantify, would likely be more damaging. The market has come to count on the presence of US buyers. Should there be a sudden exodus, internationally, many businesses will suffer. The first step merchants will take in protecting their profits will be to cut their spending, and with Bordeaux’s pricing so contentious, it is an unlikely region to remain safe within budgets.

Sentiment

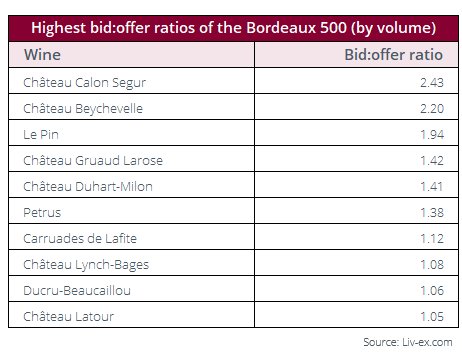

The bid:offer ratio of the Bordeaux 500 provides some insight into the demand-supply problem facing Bordeaux. In late 2021, bids (by volume) for the Bordeaux 500 component wines outweighed offers three times over. Now, for every two cases of Bordeaux 500 wines offered on the exchange, there exists demand for only one.

Hitting a new low in January at 0.28, sentiment has since improved over February and March. It is too early to say, however, whether this will persist. If the ratio rises above 0.65 (the high in June 2024), this will constitute a ‘higher high’, providing stronger confirmation that tides are turning. For the bid:offer to improve, stocks will need to be depleted – either at their current prices, or should buyers not find value at this level, lower still.

In 2024, the volume of Bordeaux 500 offers increased sharply – the monthly average more than doubling between June and December. This was likely a response to the relatively unsuccessful En Primeur 2023 campaign. Realising that prices had further to fall and conceding any hope of returns on recent En Primeur purchases, sellers began to yield, listing their stock live and lowering their prices. While sellers can be hesitant to realise losses, such a capitulation is necessary for prices to find their floor and for the market to begin to recover.

Le Pin and Petrus, produced in tiny quantities and tightly allocated, are perhaps unsurprising entrants onto this list. What may strike readers is the underrepresentation of First Growths — Château Latour is the only to feature. Choosing to leave La Place de Bordeaux in 2012, the château has more control over the supply of their wine. Indeed, only 5,000 cases of its most recent release, the 2016, left the property.

Though Château Lafite Rothschild’s Grand Vin fell further down (with a bid:offer ratio of 0.99), Carruades sits in seventh place. Asian buyers, accounting for 84.4% of the wine’s bid exposure, are driving this ratio up.

The list is largely populated by Second, Third, Fourth and Fifth Growths. Buyers are concentrating on wines with higher quality:price ratios.

Château Coutet and Château Rieussec have the lowest bid:offer ratios of the Bordeaux 500, reflecting the shift in consumer preferences away from sweet wines. Pomerol, with some of the lowest production numbers in Bordeaux, counterintuitively has three entrants on the list – L’ Église-Clinet, L’Évangile and La Fleur-Petrus.

What can we expect from the 2024s?

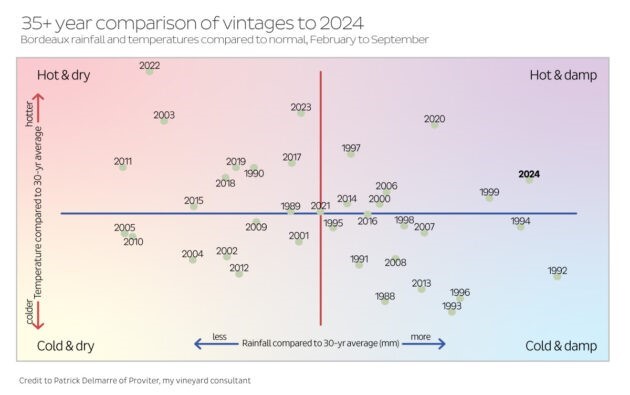

According to Gavin Quinney’s annual Bordeaux weather and crop report, ‘2024 is another in a series of small harvests since 2020 – indeed, the smallest crop overall since 1991’. While a warm, dry summer had a moderating effect on an otherwise wet and cool vintage, there will be wines that have suffered at the hands of mildew and poor fruit set.

The weather and the wines

The 2024 vintage is marked by heavy rainfall – the highest levels since the ‘unwanted’ 1992 vintage. A very wet March heightened the risk of mildew, which Quinney estimates may account for 20-25% of the reduction in yield. While ‘a rainy vintage’, he says, ‘a really good summer from mid-July to the last week of August… certainly improved the quality of the wines’. The cool and damp start to the growing season, however, resulted in ‘fewer bunches and loss of yield through poor fruit set’. He notes that poor fruit set makes grapes particularly susceptible to millerandage and coulure (malformed berries and gaps in bunches). Still, technological advancements in the vineyard and winery mean that producers are better prepared for inclement weather patterns.

For the 2023 vintage, many critics noted that the need for green harvesting and careful selection – both expensive practices – created a rift in the quality of wines produced by châteaux with cash on hand and those without. Quinney’s assessment of the 2024 growing season hints that this may again be the case.

The yields and the crop

2024 saw low yields across Bordeaux’s top appellations, with Margaux, St. Julien, Pauillac, St. Estèphe and Pomerol coming in over 20% below their 20-year average. ‘We haven’t seen the average yield in Pauillac being below 30 hl/ha in over 20 years apart from in 2013’, says Quinney, though adding that ‘the quality in 2024 is better than that difficult year’.

While poor weather was to blame for the lower-than-average yields, the crop — at least for regional level wines — was further diminished by a reduction in vineyard size. In 2024, 94,700 hectares of vineyard were declared for Bordeaux AOPs, down from 193,200 for the 2023 vintage and 107,700 for the 2022. 6,000 hectares of vines were pulled up in 2024 under the French government’s subsidised scheme. Other growers, in an effort to retain more control over their land, pulled vines outside of the scheme. Quinney raised concerns over some other ‘vineyards that have simply been abandoned because the work can be expensive’.

State of play

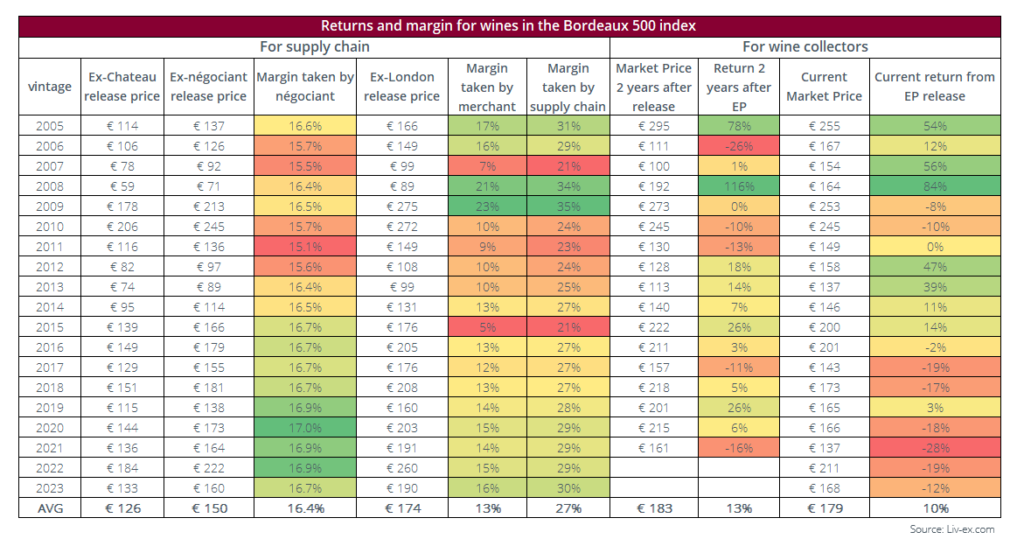

Buying En Primeur is not without risk. Scores in bottle often differ from scores in barrel and even once bottled, the wines will generally not be ready to drink for at least another five years and, for Bordeaux’s elites, not in their prime for another 10. As such, En Primeur should offer buyers a corresponding reward. Producers are provided with cash flows prior to bottling – the founding basis of En Primeur – and buyers at each step of the supply chain, from négociants to private collectors, should be provided with an opportunity to buy these wines at their lowest-ever prices. This, for close to a decade, has not been the reality. On average, buyers would have been better off buying all vintages from 2016-2023 (with the exception of the 2019) today than at their En Primeur release prices.

The 2019 vintage is an exception here. With economic uncertainty high, and since critics were unable to attend En Primeur due to COVID-19 travel restrictions, châteaux played it safe. On average, they priced the 2019s lower than the 2018s, despite them being superior in quality. What might have been considered too conservative has so far turned out to be the sole recent example of reasonable pricing. Even though average returns are positive, many (70% of Bordeaux 500 components) have fallen below their ex-London release price. When storage costs are taken into consideration (€ 12+ per case annually), returns on the 2019s are firmly negative.

Nevertheless, buyers of the 2019s had more luck than buyers of other recent vintages. Of the 236 Bordeaux 500 components hailing from the 2016, 2017, 2018, 2020 and 2021 vintages, 202 (85.6%) are on the market below their ex-London release prices. 29 of the 44 components from the 2021 vintage are on the market below their ex-château release price.

It is not just private collectors losing out at En Primeur. The Market Prices of the 2017, 2018, 2020, 2021 and 2022 vintages sit, on average, below ex-négociant release prices. Of course, if merchants were able to sell on their allocations quickly, releases were not unprofitable. With successive vintages falling in price after release and consumers increasingly savvy, however, merchants have struggled to sell on their stock. Last year, several UK merchants refused their allocations – a decision that would have been unthinkable 10 years ago.

For UK merchants, maintaining relationships with négociants – in the form of taking full En Primeur allocations at the given price — used to be a necessity. There was no other way to secure access to Bordeaux’s top wines with guaranteed providence. These days, with demand down significantly, there is no shortage of Bordeaux on the market. Moreover, with improvements in verification technology, there exists an ever-growing pool of reputable stockists.

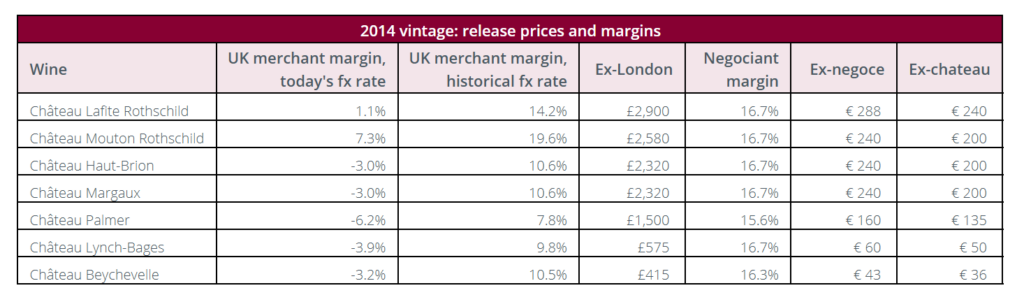

A return to 2014 pricing?

Rumours out of Bordeaux suggest that some châteaux are considering a return to their 2014 release prices.

Given the depreciation of the pound against the euro over the past 10 years, UK release prices would necessarily be higher. To generate a 15% margin on a Lafite priced at € 288/btl ex-négociant, EU merchants would have to price at € 338.8/btl, and UK merchants would have to release at £3,374 per 12×75. In either currency, this would make the 2024 vintage less expensive than any other available on the market. In other words, it would present serious value to buyers at each step of the supply chain.

Best and worst performers

Of the Bordeaux 500 components, Château La Mission Haut-Brion comes in as the worst price performer relative to release. Market Prices of all vintages from 2015-2021 have now fallen below their ex-château release price. The 2021, having had only two years on the market, last traded at £1,386 per 12×75 – 27.8% below its ex-château release price (€ 188/btl, then equivalent to £1,920 per 12×75).

Petrus is by far the top performer relative to ex-London release price, but an allocation is not easy to secure. The lucky few purchasers have seen returns in excess of 45% for the past 10 vintages.

Château Carmes Haut-Brion is the second-best performer on average. Market Prices of the 2012-2019 vintages all sit above ex-London release prices.

Supply chain

Creditsafe financial data (for five of Bordeaux’s top négociants) shows that on average, debt:equity ratios are decreasing, and stock days are rising. The average debt:equity ratio is not concerning (remaining well below two) but this ratio alone doesn’t tell the whole story. The ratio is falling mainly due to inventories growing. Since sales revenues are down, this inventory growth is unlikely to be intentional. By any standard, stock days are far too high. Given that some UK merchants rejected their allocations for the first time last year, this is unlikely to have improved in 2024.

Of even greater concern are the average operating margins for this same pool of négociants. While breaking even in 2022, they averaged a loss in 2023. It goes without saying that this is not sustainable. Globally, few merchants have been spared from the repercussions of current market conditions. With a business model reliant on realistic release pricing, négociants have been hit doubly hard.

Conclusion – what’s in it for the Châteaux?

In last year’s Bordeaux EP closing report, after a largely unsuccessful campaign, we asked how important the success of the campaign was to châteaux. Since the wealthier châteaux (who often lead by example with price reductions or increases), have little need for additional cash flow, it could be argued that, for them, En Primeur serves largely as a marketing tool. This may be the case – if their wine doesn’t sell, they can afford to store and release it once physical. Châteaux do, however, rely heavily on négociants, who in turn rely on the success of En Primeur. With négociants now at a tipping point, correct ex-château release pricing could make or break several businesses

Cutting out the middleman is perhaps not as simple – nor profitable – as it might appear. Château Latour has seen some success with releasing independently from En Primeur and holding back stock, but spending extravagantly on storage is a luxury that very few can afford. Moreover, were châteaux to remove themselves from La Place altogether (or if La Place were to break down), they would have to build their own distribution networks. To do so would require significant time and investment from châteaux, many of whom are still financing debts from winery improvements and renovations.

With demand already down, a new 20% tariff imposed on all and global economic uncertainty high, now is not an attractive time to go solo. Négociants are in hot water, and unless this year’s releases are attractively priced, they may be unable to weather the storm. Should this be the case, châteaux may, in turn, find themselves in a difficult position.

The positive effects of well-considered pricing don’t just trickle down to châteaux via the benefit to négociants and merchants. Strong performance on the market has a direct, positive impact on brand image. At the right price, there is demand. Where there is sufficient demand, there is room for positive returns. This room is a necessity – capital, storage and insurance are not free. Significant drops post-release creates suspicion amongst buyers, making room for further downward price movement. According to Allan Sichel, CEO of Maison Sichel and president of the CIVB (via The Drinks Business), châteaux are committed to making this year’s campaign a success. A successful campaign – one that generates value at each step of the supply chain as well as for the end consumer — is in everyone’s best interests. To make it happen, châteaux, négociants and merchants will need to be aligned.