April Market Report

- The fine wine market in March

- Each major index fell in March. The Liv-ex Fine Wine 100 was down 0.7% to close at 321

- March market activity

- Average transaction value rose 14.7% in March, driven by an uptick in higher value Burgundy trade than the first two months of the year

- US market activity since the announcement of tariffs

- Since the threat of 200% tariffs on March 13th US buyers have pulled their bids. While the situation is extremely volatile, we consider possible next phases

Indices overview

The Liv-ex Fine Wine 100, the industry leading benchmark, fell 0.7% in March, closing at 321. Looking at the wider market, the Liv-ex Fine Wine 1000 (which tracks 1,000 wines from across the world), fell 0.1% in March. The Italy 100 continues to show resilience, recording a 0.4% rise.

The Bordeaux 500, which tracks the 10 most recent physical vintages of 50 of Bordeaux’s top châteaux, fell 0.5% in March. 200 components recorded rises, while 234, including nine vintages each of La Mission Haut-Brion and Château Lafite Rothschild, recorded declines and the remaining 66 were flat.

March market activity

The impact of Donald Trump’s threat of 200% were writ large on the fine wine market in March. US purchase share fell from 33.3% in February to 21.3% in March, a reduction of 35.5% in nominal terms.

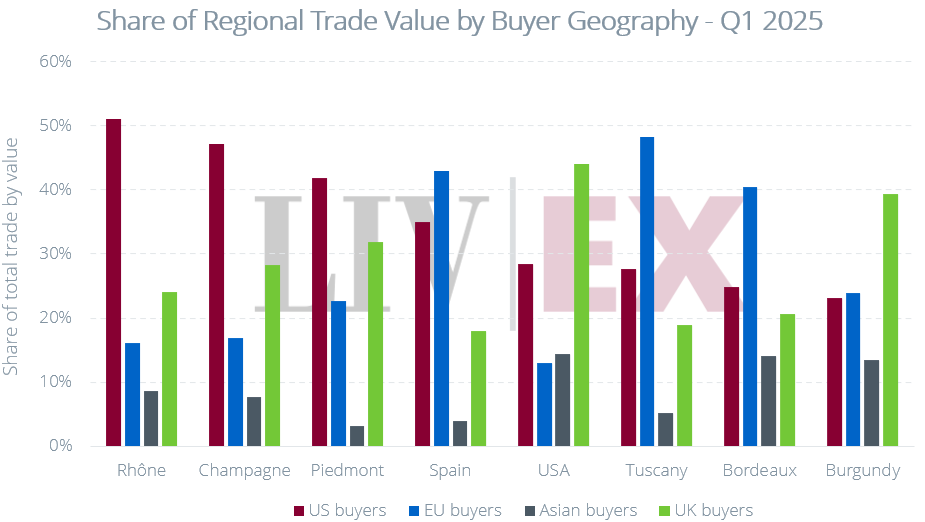

Breakdown of buyer geography – Q1 2025

However, despite this sharp slump in US purchases, March rounded off an active first quarter. While prices continue to fall, total trade value, trade count, and trade volume were all up compared to Q1 2024.

Trade evolution – Q1 2025

Notably, March saw average transaction value rise 14.7% on February. While January and February saw the average transaction value sit 9.5% below their 2024 levels, the average transaction value in March 2025 was 2.0% above the March 2024 average.

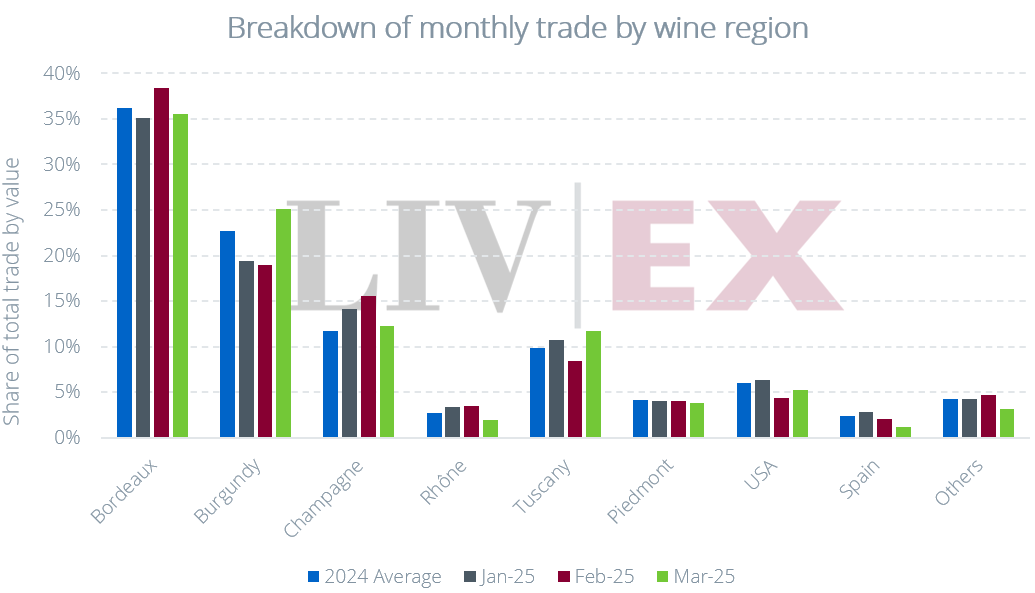

This can be largely attributed to an uptick in higher end Burgundy trade. In March the average cost per 12×75 case of Burgundy traded was 9.8% above the February level. With Burgundy trade volumes also rising 24.2% in March, total Burgundy trade value was up 39.0% month-on-month. This resulted in Burgundy trade share rising to 25.1% in March from 19.0% in February.

Market Share by Wine Region – Q1 2025

Sentiment check

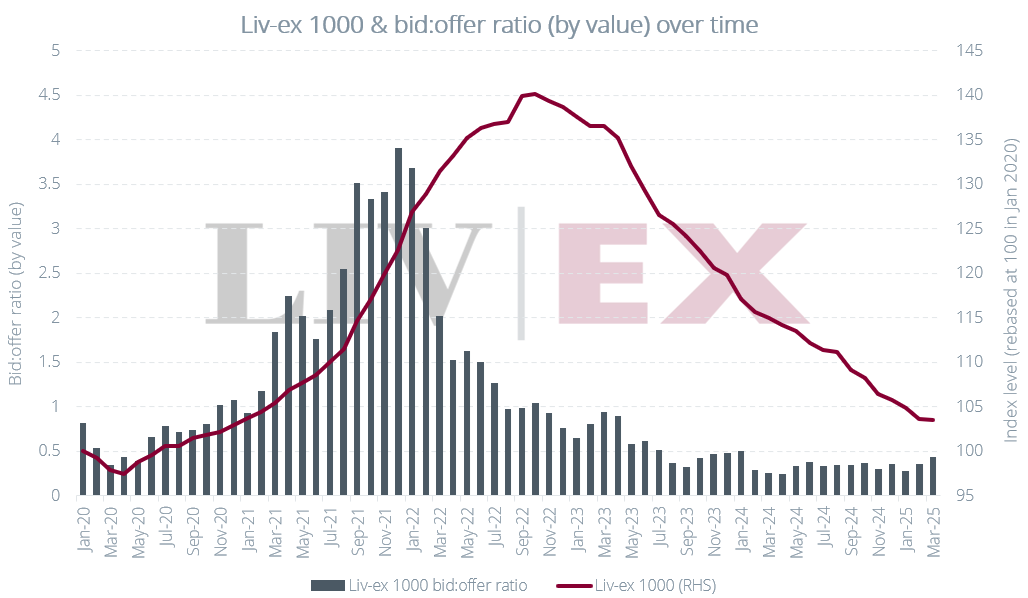

At the end of March the bid:offer ratio by value for the Liv-ex 1000 sat at 0.43, the highest level since January 2024. March saw the value of bids rise 11.1% on February, while offer value fell 6.8%.

Liv-ex 1000 bid:offer ratio by value

However, the already risk-averse market was dealt a blow on March 13th, with the threat of 200% tariffs. While tariffs at that level were very unlikely, it knocked the wind out of the US market.

Final thought – Recent US market activity overview

The imposition of 20% tariffs (reduced to 10% on 9th April for 90 days) on EU wine imports into the US has had an immediate impact on the wider market. Before diving into the data, a brief recap of the role US participants have played in the fine wine market:

- In 2024, for the first time ever, US buyers accounted for the greatest share of total purchase value (35.5%)

- This is despite US merchants accounting for just 11.7% of market participants

- US buyers have played an important role in the fragmentation of the fine wine market, increasing the market share for major Italian regions and the Rhône

- US buyers have historically over-indexed on Champagne buying, accounting for 47.4% of total Champagne purchase value in 2024

As the buyer geography chart above shows, US buyers have taken a backseat since March 13th. While the threat of tariffs created uncertainty, April 2nd brought some degree of clarity, and the market reacted immediately.

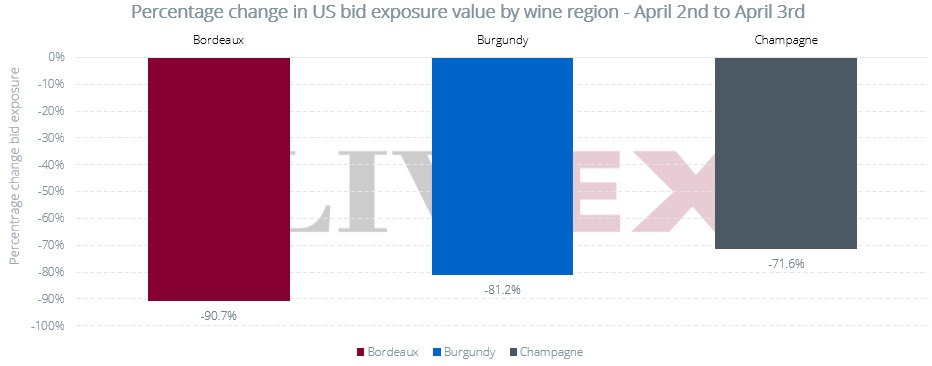

Overnight from the 2nd to the 3rd, US bid exposure fell 80%. US Bordeaux bid exposure was the worst affected, down 90.7%.

Percentage change in US bid exposure by value by wine region – April 2nd to April 3rd

In short, US buyers were more likely to keep their Champagne and Burgundy bids live than they were Bordeaux.

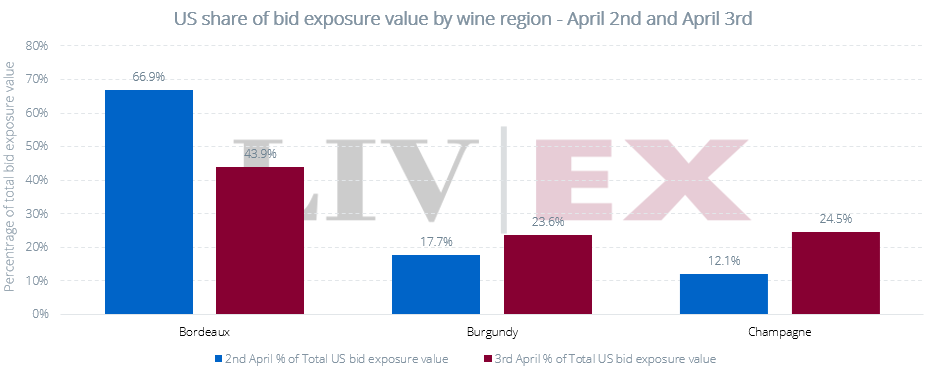

US share of bid exposure by wine region – April 2nd and April 3rd

What comes next?

While the outcome is far from clear, there are some possible phases:

- US greatly reduces buying for a period. This is where we are now

- The reduction in demand prompts a further fall in prices

- US buyers come back when stock is required

Let’s address these in turn.

Phase 1 – US greatly reduces buying for a stock cycle

As we move beyond this holding phase, it is almost certain that US buying will fall while there is still enough stock on US soil. However, this is unlikely to have an equal impact on trade for every wine region. Regions that have seen significant US demand such as the Rhône, Champagne, and Piedmont look particularly exposed.

Breakdown of regional wine purchases by buyer geography

In particular, buying for stock is likely to dwindle, with the majority of remaining demand likely to come directly from consumers who are willing to absorb the tariff.

Phase 2 – The reduction in demand prompts a sharp fall in prices

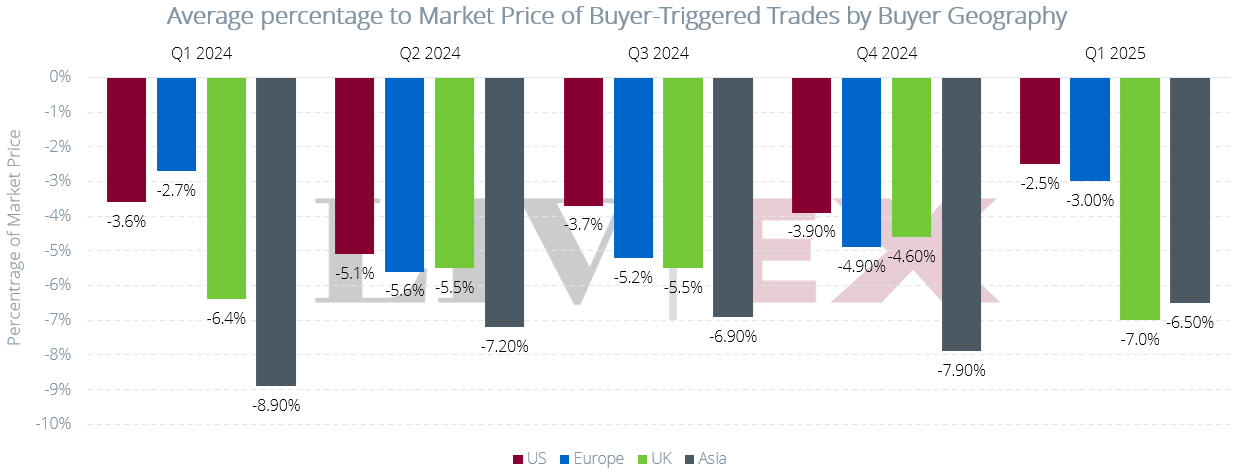

In a market that continues to be blighted by a demand-supply imbalance, a 35.5% reduction in purchase value from the most important buying geography of recent times presents a severe problem. Moreover, US buyers have supported prices, tending to trigger trades closer to Market Price than buyers from other geographies.

Percentage to Market Price of Buyer-Triggered Trades by Buyer Geography

However, while painful for the wider market, this might end up mitigating the effect of tariffs for US consumers. For example, all other things being equal (which is a big caveat given the current volatile macroeconomic situation), if prices were to fall 5%, then a 10% tariff becomes more manageable.

Phase 3 – US buyers come back when stock is required

Fine wine is not fungible. As such, US buyers will return to some extent when they need to refill their cellars with European wine. When tariffs were last imposed, they were not applied to all EU wines. This time they are, which levels the playing field. As such, one would expect a focus on the least risky bets. This would likely take the form of brands with proven US demand and also those where US merchants could still make a margin. With US fine wine prices tending to be higher than in the UK and Europe, there may well be opportunities for US buyers to still make margin while holding prices to end consumers.

The question of who will absorb the tariffs does remain. With the three-tier distribution system and then end consumers, there are multiple participants in the supply chain that can shoulder part or all of the tariff. It is likely that there is not one clear outcome here, and it will differ by merchant, wine, and tariff level.

Other considerations

Beyond wider macroeconomic concerns (ie. will US consumers be better or worse off), US dollar strength is a key consideration. Since April 2nd, the USD has weakened against the Euro. Moreover, it seems that the US government will aim to devalue the USD. This would clearly put a dent in US wine imports.

Conclusion

As the above shows, the outcomes are currently far from certain. But as long as the situation remains volatile, it is likely that US buyers will continue to take a back seat. Beyond what this means for US consumers, EU producers and merchants that sell to the US will be waiting nervously.