What’s happening in the market?

Sassicaia 2020 and Soldera Case Basse 2019 are the top-traded wines of the week so far by value, leading Tuscany to a 16.2% share of the market.

Taittinger, Comtes de Champagne 2013 is following in third place, trading in low volumes at £1,132 per 12×75 and high volumes at £1,086. While seeing a downward trend in 2024, its trade prices have held steady since the start of the year

Today’s deep dive: the Lafite premium and Haut-Brion discount

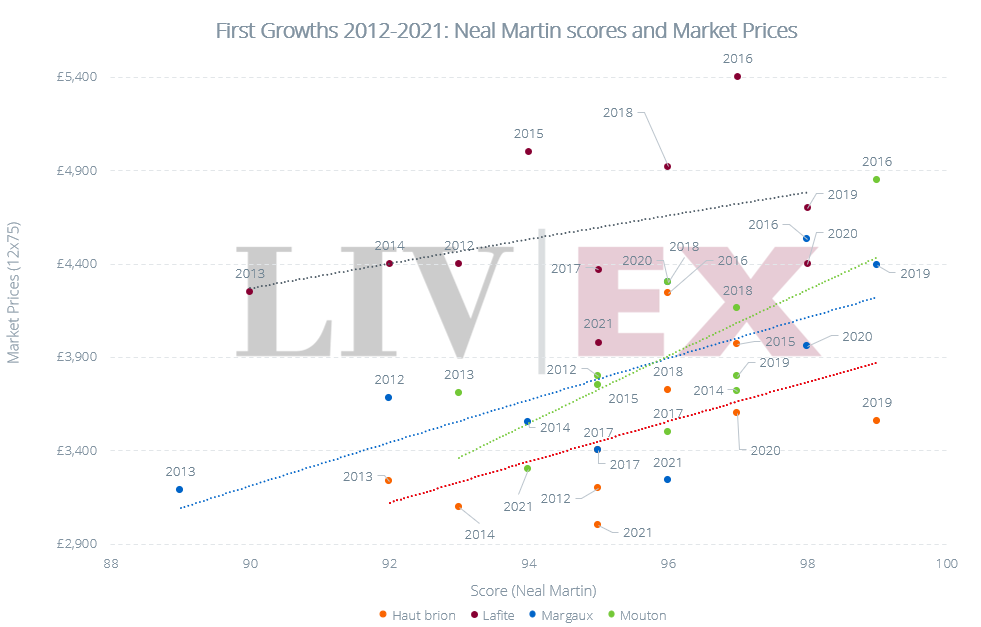

Margaux 2015, double the price of most other vintages, has been omitted from this chart to preserve scale.

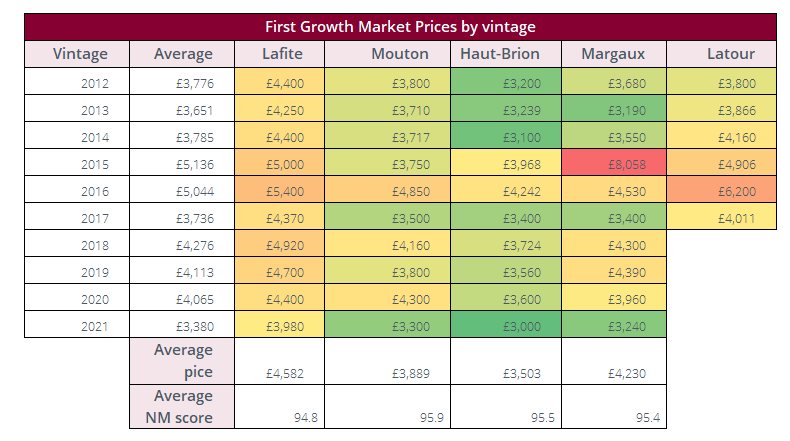

The past 10 physical vintages of Chateau Lafite Rothschild (2012-2021) have an average Market Price of £4,582 – a premium to all of its First Growth peers (excluding Latour) — and an average Neal Martin score of 94.8. While this average score is undoubtedly impressive, it is the lowest in its peer group. Still, scores are not the only determinants of price. Buyers of Lafite are buyers of its history and heritage, and of its distinct essence. Lafite has held court as the top-traded brand on the secondary market every year since 2004.

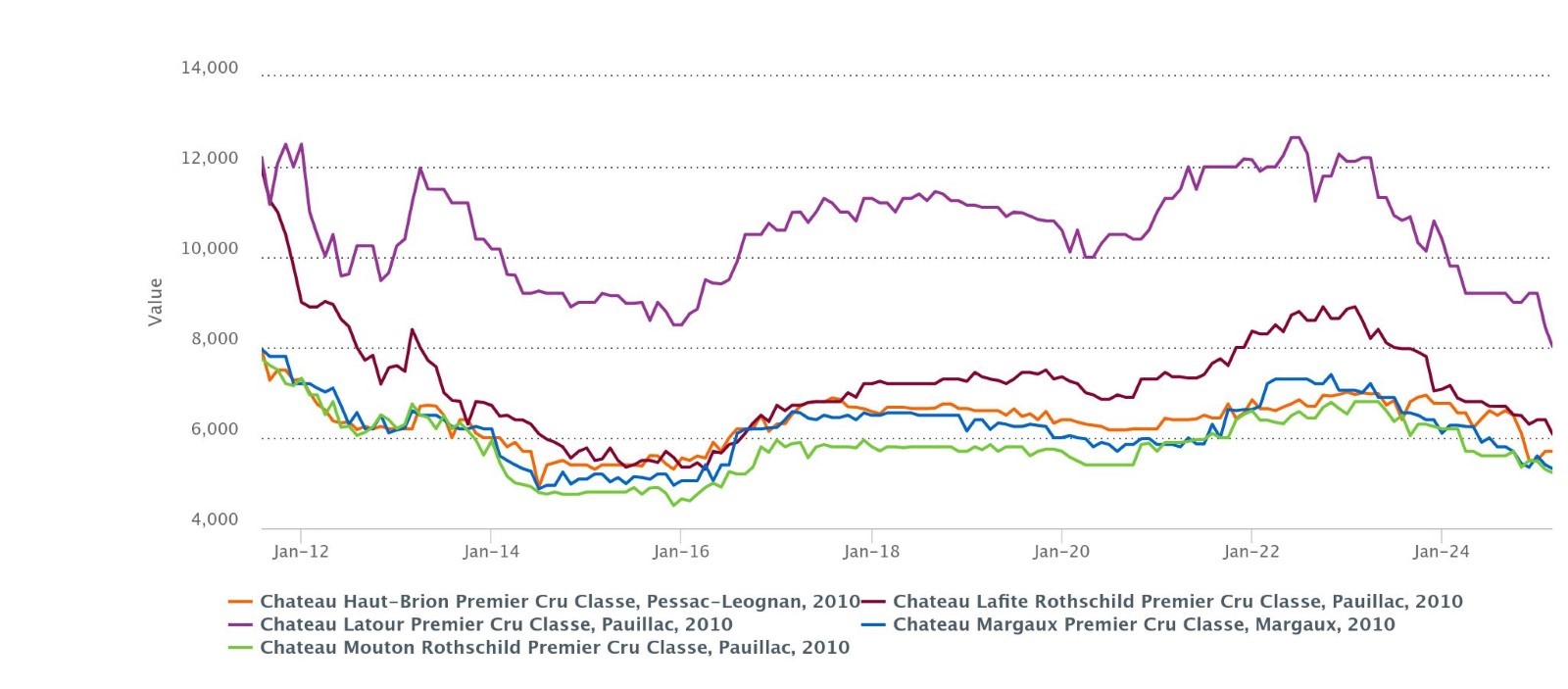

Some of this premium, however, can likely be attributed to Lafite’s price increases in the late 2000s. During this time, Lafite and Latour found immense popularity on a very active Chinese market. With demand at an all-time high, prices of Lafite, Latour and their Second Wines (Carruades and Les Forts) were driven steeply upward. Both chateaux upped their release pricing considerably. Lafite 2009 and Latour 2009 were both released ex-London at £11,000 per 12×75. For Lafite, this represented 494.6% increase on the 2008’s release price (£1,850) and for Latour, a 598.1% increase (2008 released at £1,590). Lafite again raised their price for the 2010’s release, bringing the ex-London up to £12,000, while Latour held at £11,000. Prices were driven up not just by Chinese demand and willingness to pay, but the subsequent lack of supply in Europe.

By mid-2012, the Chinese market had subsided and the price of Lafite and Latour 2010 had fallen to £7,599 and £10,250 respectively.

Made using the Liv-ex charting tool

Latour 2010 received far more critical acclaim than Lafite 2010, earning several 100-point scores. This likely went some way to stabilising its price at a higher level. In recent years, with Latour releasing their wines outside of en primeur, the total supply has been artificially restricted, further propping its prices up above its peer group.

Chateau Haut-Brion, on average, comes at a discount to its peer group, with an average rating of 95.5. In 2009, at the peak of the Chinese market’s dominance, Asian buyers accounted for 27.7% of Latour purchasing, 20.1% of Margaux 20.0% of Mouton, 18.0% of Lafite, but just 10.2% of Haut-Brion. As such, the supply of Haut-Brion faced less pressure, and its prices remained low relative to its peers.

While the table below (Market Prices / Neal Martin scores) does not take into account the exponential price growth associated with moves towards the end of the 100-point scale (the price difference between a 98 and 99 point wine will be smaller than that between a 99 and 100 point wine), it may go some way towards helping buyers identify opportunities.

Haut-Brion 2012 and 2014, and the 2021 vintages of Mouton, Margaux and Haut-Brion, whose prices have tumbled since release, stand out as particularly good opportunities. Haut-Brion 2021 last traded at £2,800 per 12×75, 20.2% below its ex-chateau release price. Unless in response to changes (manufactured or autonomous) in supply and demand, attempts to increase release prices tend not to be successful.

There are another 25 six-packs available at the same price (£1,400 per 6×75). As these are not listed live, please reach out if you are interested.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £140m of bids and offers across 20,000 wines.