March Market Report

- The fine wine market in February

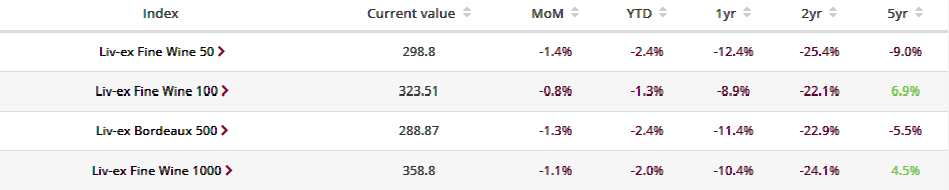

- Each major index recorded a decline in February. The Liv-ex Fine Wine 100 now sits 2.2% above its 2018 peak, which acts as its next support level

- 2025 year-to-date trade overview

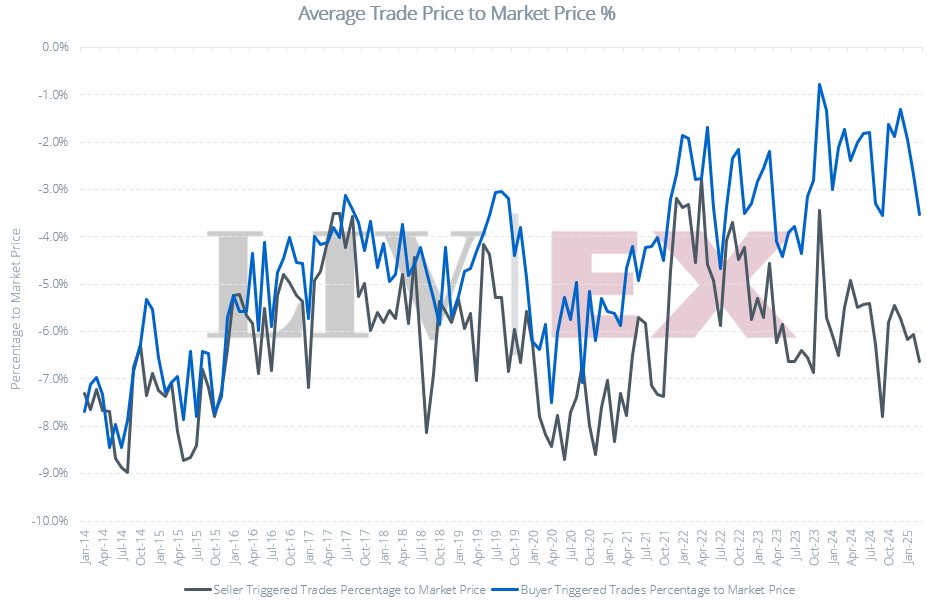

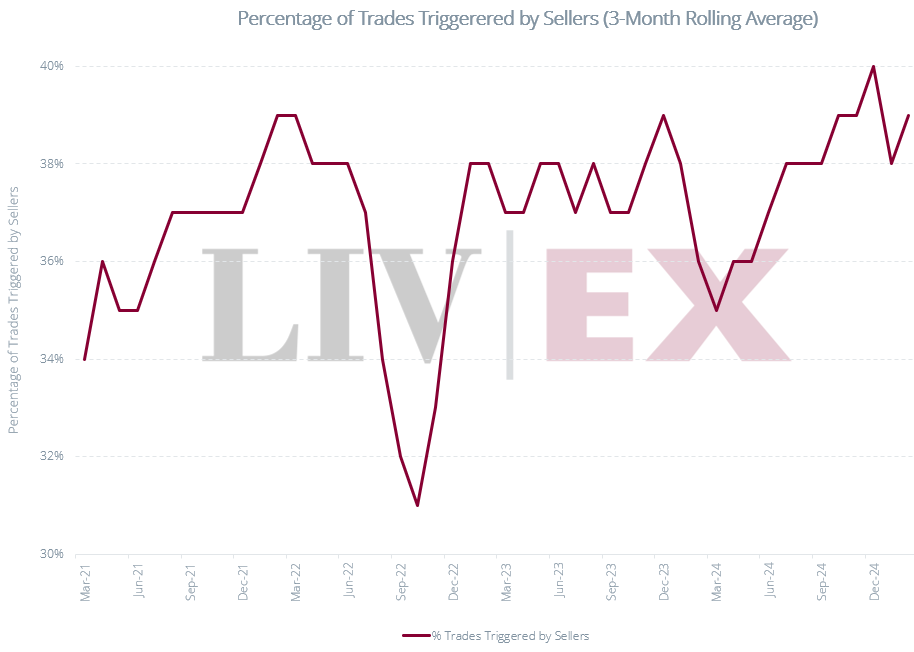

- 2025 trade has been characterised by a significant rise in trade volumes, with sellers triggering a higher proportion of trades. Trades are also occurring at greater discounts to Market Price

- Burgundy trade analysis – who’s driving increased trade volumes?

- Regional Burgundy has seen a steep rise in trade volumes so far this year. Sellers are driving this trend, triggering 70% of trades in February

Market Overview

March saw each of the major Liv-ex indices record a decline. The Liv-ex Fine Wine 100, the industry leading benchmark, fell 0.8% to close at 323.51. The index now sits 2.2% above the 2018 peak, which acts as its next support level.

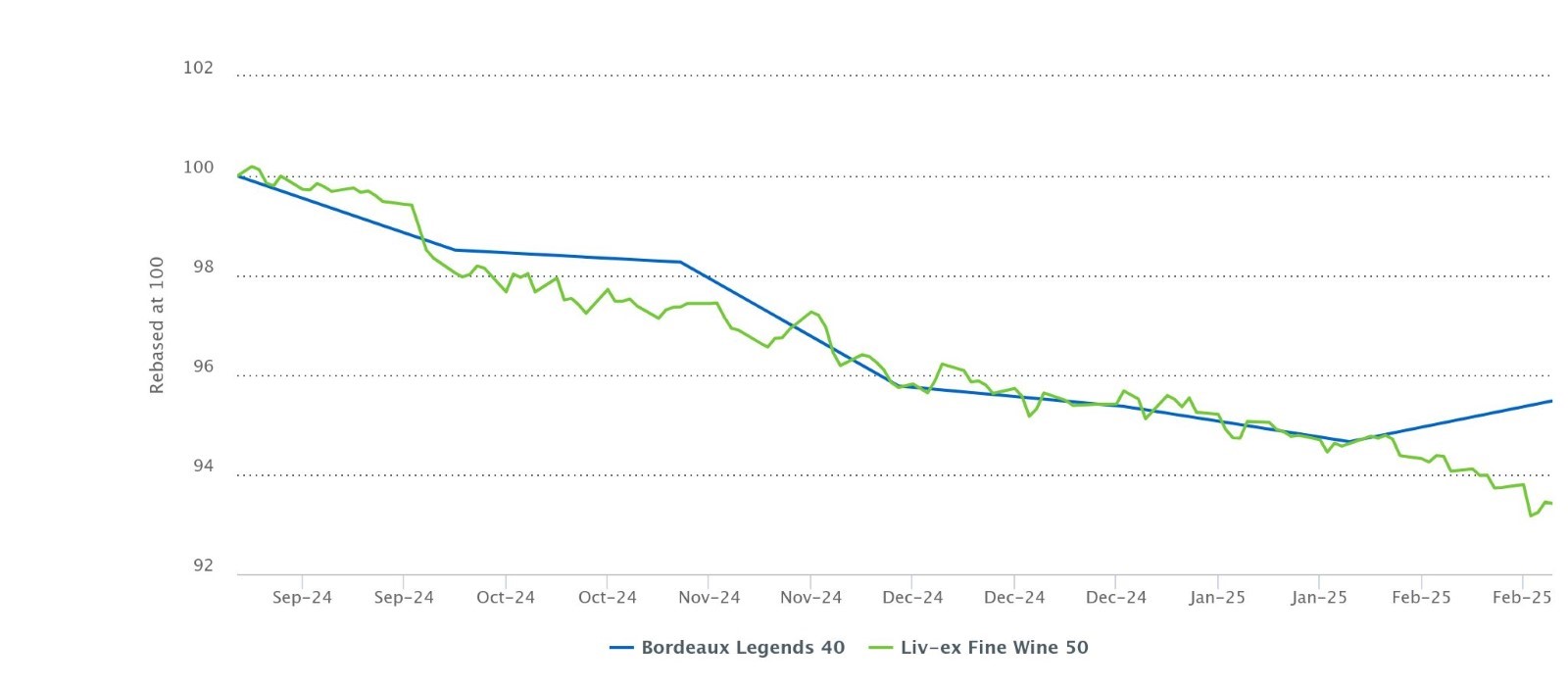

Looking at the wider market, the Liv-ex Fine Wine 1000 fell 1.1% to close at 358.8. The Bordeaux Legends 40, which tracks the performance of blue chip back vintage Bordeaux, was the only sub-index to record a rise (+0.9%). There was a marked contrast in its performance compared to the Fine Wine 50, which tracks the 10 most recent physical vintages of the First Growths (-1.4%).

Bordeaux Legends 40 vs Fine Wine 50

2025 year-to-date Trade Review

2025 has so far been characterised by an uptick in market activity. Compared to the same period in 2024, trade count is up 17.4%, trade volume is up 31.6%, and trade value is up 6.3%

Notably, the average trade price has been falling further below Market Price since the start of the year, both when buyers and sellers are triggering the trade.

Average Trade Price to Market Price

This has been accompanied by a rise in the percentage of seller-triggered trades. While a similar trend was seen at the start of 2024, there are two notable differences. First, the uptick in seller-triggered trades has started earlier this year than last. Secondly, it has started from a higher baseline proportion of all trades. This is perhaps indicative of mounting pressure on stockholders and tighter purse strings for buyers.

Percentage of Trades Triggered by Sellers

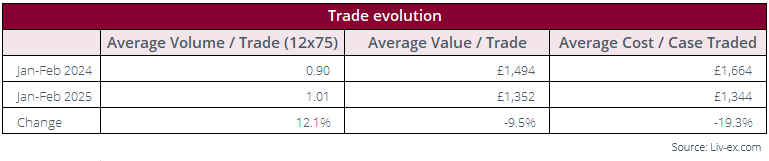

Trade Evolution – January-February 2024 vs 2025

Trades are happening in higher volumes, but while the fall in average value / trade is broadly in line with average price decreases over that period (the Liv-ex 1000 is down 10.4% over the past 12 months), the greater fall in average cost / case traded indicates that lower price wines are currently trading.

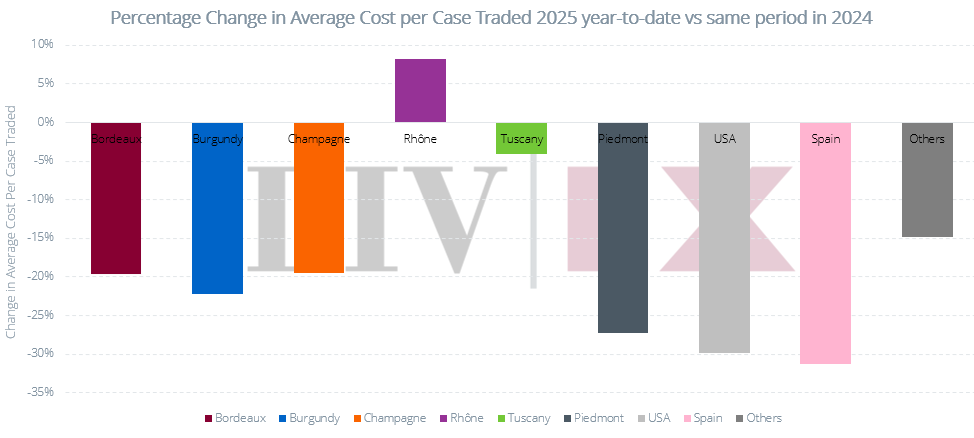

Percentage change in average cost per case traded by region – 2025 year-to-date vs same period in 2024

In Bordeaux, the initially mispriced 2021s now account for the greatest share of trade volume. Having come under increasing pressure over recent months, the most recent trade price across all Bordeaux 2021s was on average just 3.8% above ex-chateau. In Burgundy, as we will return to later on, the 22.2% fall in the average cost / case traded is courtesy of a sharp rise in trade volumes of Regional Burgundy.

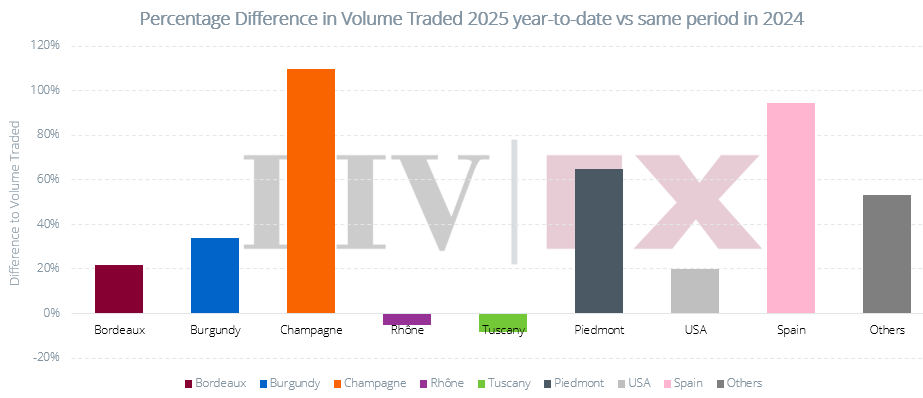

Percentage change in volume traded by region – 2025 year-to-date vs same period in 2024

Champagne trade volumes are more than twice the level they were this time last year. While this has been supported by high volume trades of the likes of Perrier Jouet Belle Epoque 2015, leading producers Dom Perignon and Louis Roederer have both seen trade volumes rise significantly (up 158.8% and 68.4% respectively). Spain’s uptick is overwhelmingly down to Vega-Sicilia, whose trade has risen dramatically over the past 12 months.

Final Thought – who’s driving Burgundy trade

In our annual Burgundy Report, published last month, we noted that 2025 has seen an uptick in Burgundy trade, particularly for regional wines. Today we drill down further into what’s driving this.

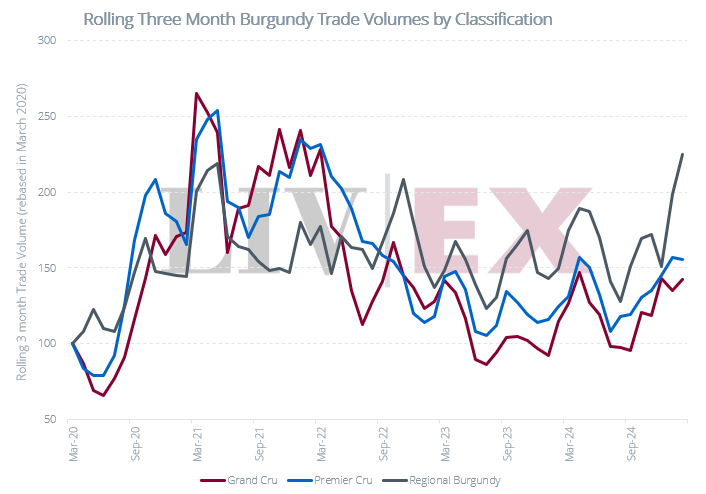

Liv-ex Burgundy Trade Volumes by Classification

While indexed trading volumes for each of the three categories had tracked each other relatively closely since the turn of the market in late 2022, Regional Burgundy has broken out since the start of 2025.

48.2% of Burgundy trade volumes year-to-date have been for Regional Burgundy, up from 39.4% last year, 39.1% in 2023, 34.3% in 2022, 29.0% in 2021, and 34.4% in 2020.

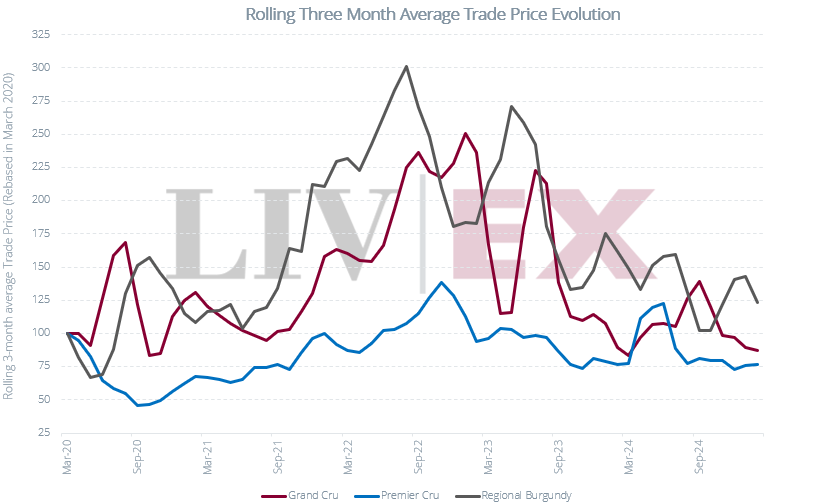

Average trade prices for Grand Cru Burgundy have consistently fallen over the past six months. Meanwhile Premier Cru trade prices have flatlined, 23.5% down on where they were in March 2020 and 44.7% below peak. Regional Burgundy trade prices, while more volatile, have not fallen quite so far, but fell in February.

Average Burgundy Trade Price Evolution by Classification

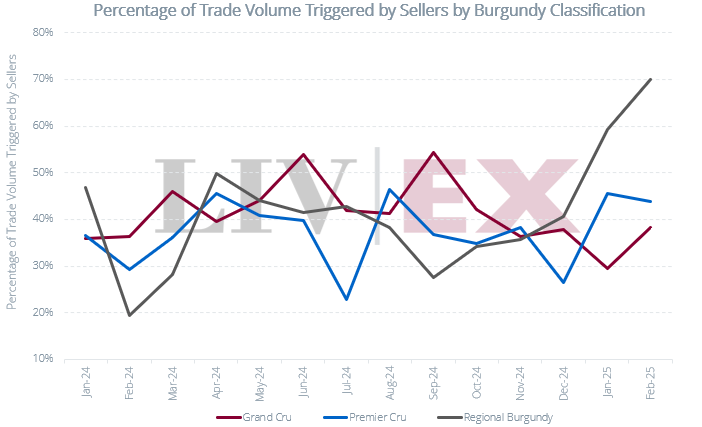

All of this raises the question – is it buyers or sellers who are driving this rise in Regional Burgundy trade volumes?

Percentage of Trade Volume Triggered by Sellers by Classification

Since September, sellers have been increasingly responsible for Regional Burgundy trade volumes, triggering trades that accounted for 69.9% of volume in February.

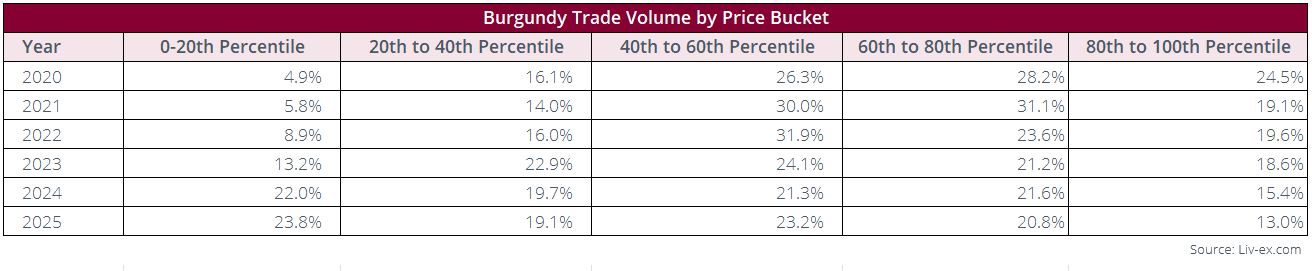

In February 2024, this was just 19.4%. Stockholders appear to be committing to clearing out cheaper Regional Burgundy from their cellars before they turn their attention to their more expensive lines. This is reflected in the cheapest 20% of Burgundy wines (0-20th percentile in the table below) accounting for the greatest share of any price bucket year-to-date.

Burgundy Trade Volume Share by Price Bucket

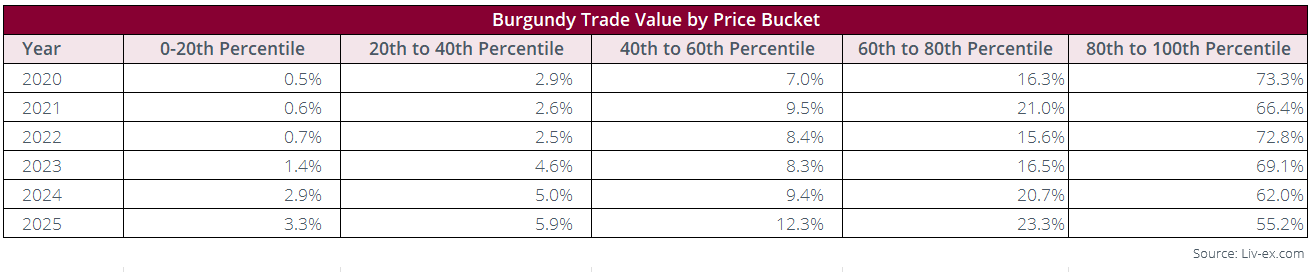

However, with the lower end still accounting for a tiny fraction of Burgundy’s total trade value, the question remains if this clear out of lower end stock will really make much of a difference?

Burgundy Trade Value Share by Price Bucket

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.