- Each of Liv-ex’s major indices fell in February

- Bordeaux 2021s recorded the greatest fall on average, but are seeing a marked increase in trade volumes

- Bordeaux Legends 40 and Sauternes 50 rise

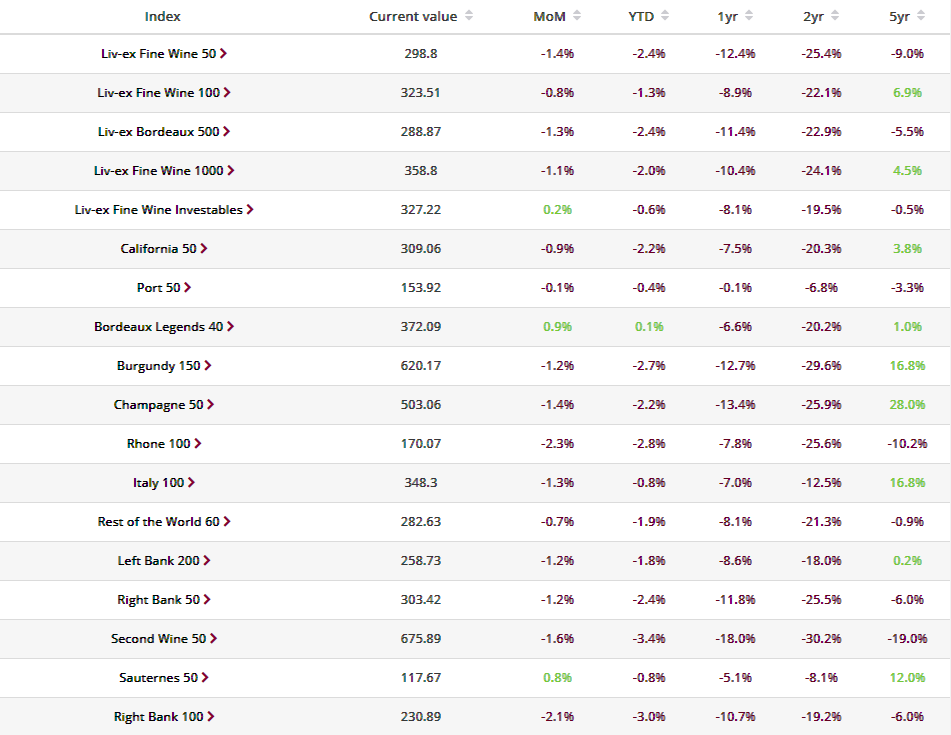

March saw each of the major Liv-ex indices record a decline. The Liv-ex Fine Wine 100, the industry leading benchmark, fell 0.8% to close at 323.51. The index now sits 2.2% above the 2018 peak, which acts as its next support level. In February, we revealed the results of our annual survey in which Liv-ex members predicted that the Fine Wine 100 would fall 1.9% across 2025, to close the at 320. This is just 1.1% below the current level.

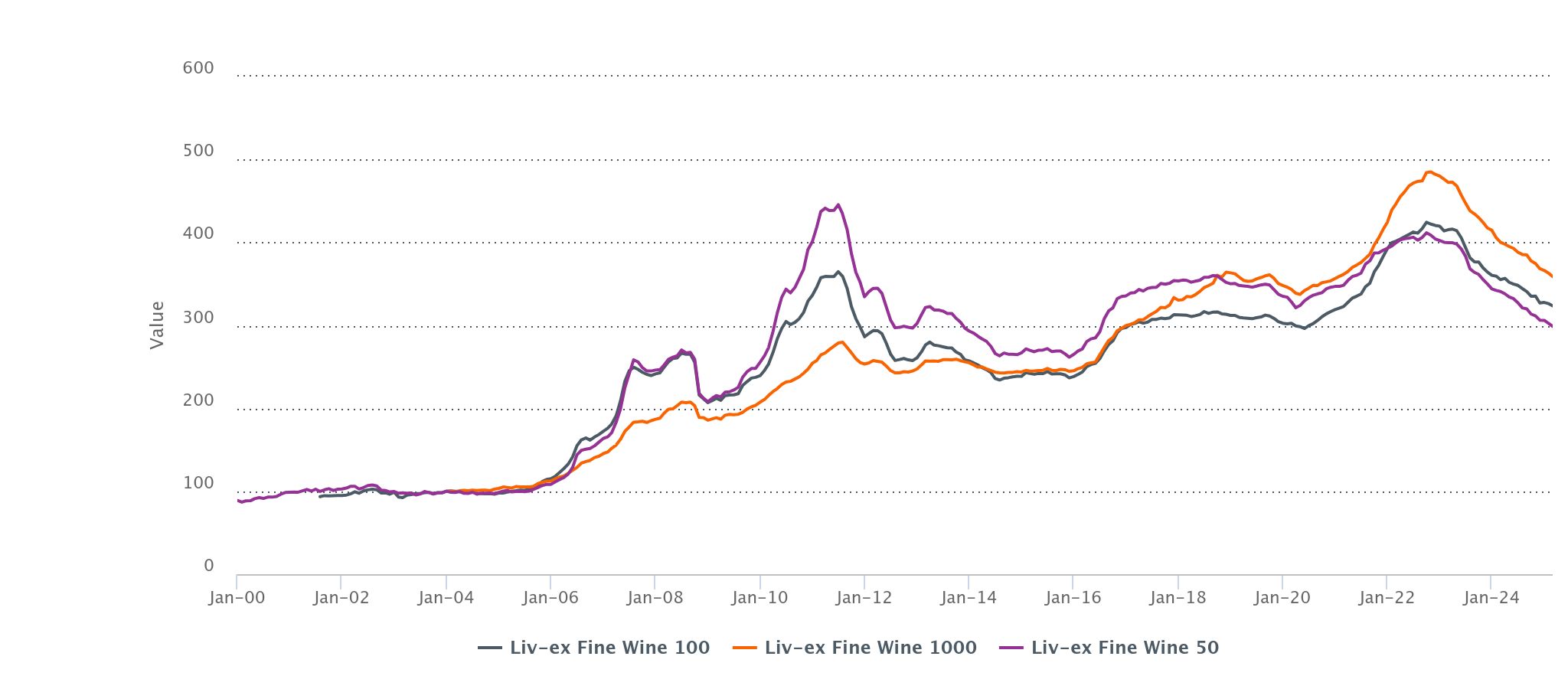

Liv-ex Major Indices Long-Term Performance

The Fine Wine 50 – prices fall and trade rises

The Fine Wine 50, which tracks the daily movements of the 10 most recent physical vintages of the Bordeaux First Growths, fell 1.4% to close at 298.8. It is now back at its 2012 low. While the index has continued to fall, February saw a notable uptick in trade. With bid:offer spreads of the Fine Wine 50 narrowing over the past month, the index recorded its highest trading volumes since July 2021. Month-on-month, trade volumes were up 67.7%. The 2021s are driving this surge, volumes up 56.8% compared to January to account for 39.2% of February Fine Wine 50 trade.

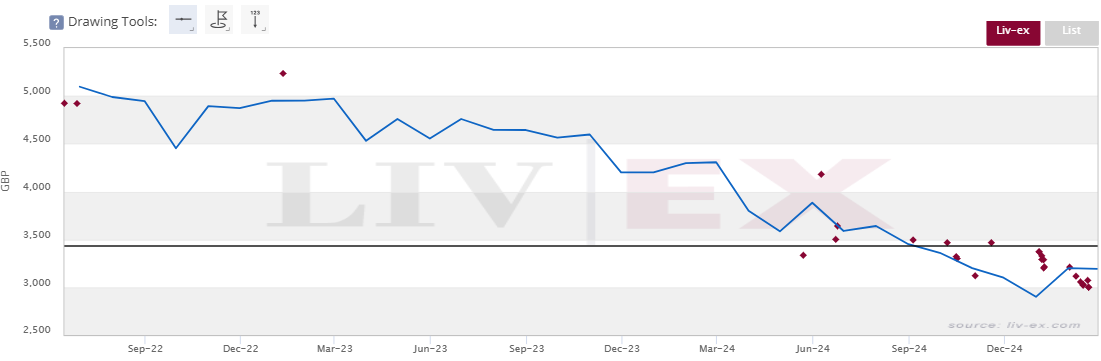

Margaux 2021 was the top-traded component of the Fine Wine 50 in February. It saw a flurry of trade at the start of the year after its price fell decisively below the ex-chateau level (€350/btl, today equivalent to c.£3,470 or $4,420) – indicated by the line on the chart below. However, this has not prevented it from further falls, with February seeing significant trade occur just above the £3,000 / $3,772 per case mark (equivalent to €302/btl).

Liv-ex Trades of Margaux 2021

The Fine Wine 1000 and sub-indices

Looking at the wider market, the Liv-ex Fine Wine 1000 fell 1.1% to close at 358.8. The Bordeaux Legends 40, which tracks the performance of blue chip back vintage Bordeaux, was the only sub-index to record a rise (+0.9%). Its performance was in stark contrast to the broader Bordeaux 500 which tracks more recent vintages (down 1.3%). The 44 Bordeaux 500 components from the 2021 vintage fell 4.1% on average. The ex-chateau release price now tends to be the level to watch for the 2021s, with the majority of trade occurring close to that level.

Italy 100 falls 1.3%

Having recorded a modest rise of 0.8% in January, the Italy 100 fell this month. The longer-term divergence between the Tuscan and Piedmontese components continues. In February, the Tuscan components fell 1.1%, while their Piedmontese counterparts fell 1.6%.

Italy 100 performance – Tuscan vs Piedmontese components

Any silver linings?

Similarly to the Fine Wine 50, the wider market continues to see a surge in activity so far this year. Compared to February 2024, last month saw a 12.4% increase in trade count and 23.2% increase in trade volume. The difference is even more pronounced when compared to the 2024 average, with February trade count and volume up 24.1% and 39.5% respectively compared to last year’s average. For certain vintages and regions, it appears that prices are now reaching levels to invigorate demand.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.