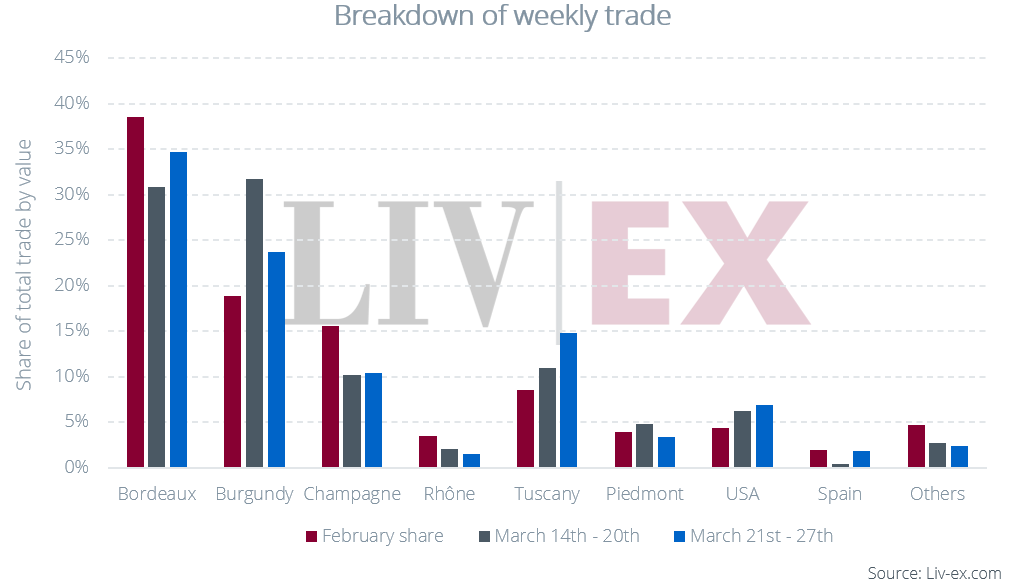

- Bordeaux leads trade, with 2021 the region’s top-traded vintage

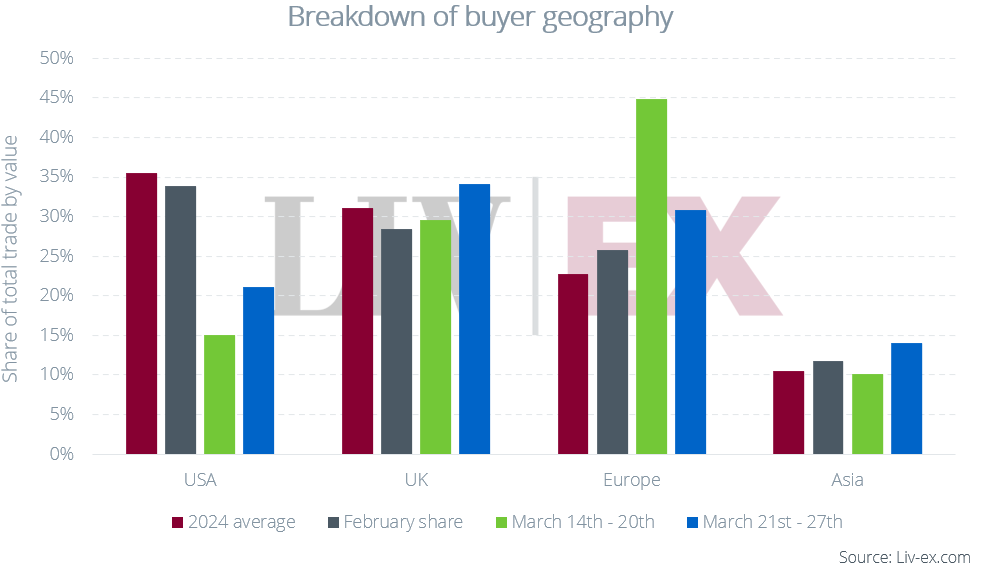

- US purchases rose on last week, but continue to sit well below their 2024 average

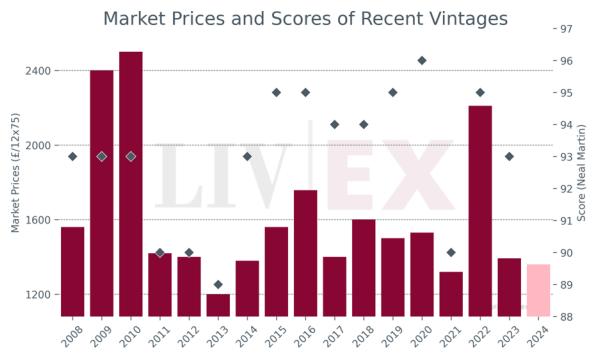

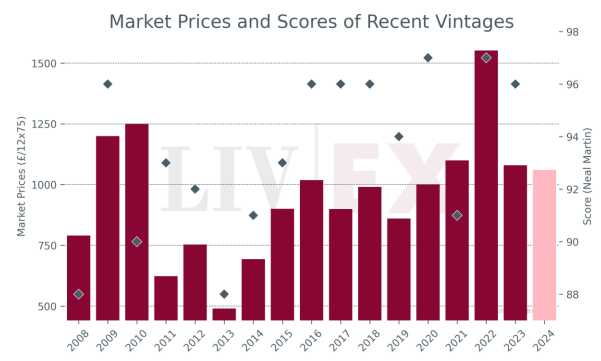

- This week, Liv-ex members were sent analysis of where the value is in recent Bordeaux First Growth vintages

Having slipped behind Burgundy last week, Bordeaux retook the lead, accounting for 34.7% of trade value. Petrus was the region’s top-traded producer, boosted by large format trades of the 2005 and 2016. Overall, 2021 was Bordeaux’s top-traded vintage. Notably the 2021 vintage made up 34.0% of Asian Bordeaux purchase value, compared to 24.6% for European Bordeaux purchases, and just 1.1% and 1.0% for the UK and US respectively. It appears that for Asian buyers, typically more brand focussed than in other regions, the lower quality 2021s have now fallen to price points that inspire demand.

Burgundy took a 23.8% share of trade value. Domaine de la Romanée-Conti accounted for 40.5% of total Burgundy trade value, with assortment cases of the 2017 and 2013 vintages leading the way.

This week’s Champagne and Tuscan trade were notable. As we saw last week, the threat of US tariffs has had a clear impact on Champagne trade. In the past week, the average daily US purchase value of Champagne was just 29.9% of what it was in February, contributing to another weak close for the region. Conversely, over the past week the US average daily purchase value of Tuscan wine was 132.9% of the February daily average. With EU buyers also stepping up, Tuscany rose to a 14.8% share of trade value.

Breakdown of buyer geography: US buyers up on last week

US purchase value rose 82.2% this week and accounted for 21.1% of total trade value, compared to 14.1% last week. Nevertheless, this is still well below the February share (33.9%). UK and Asian buyers stepped up, both concentrating purchases on Bordeaux.

In our April market report we will be conducting a deeper analysis of recent US purchase behaviour and what the impact of tariffs might be on the market as a whole.

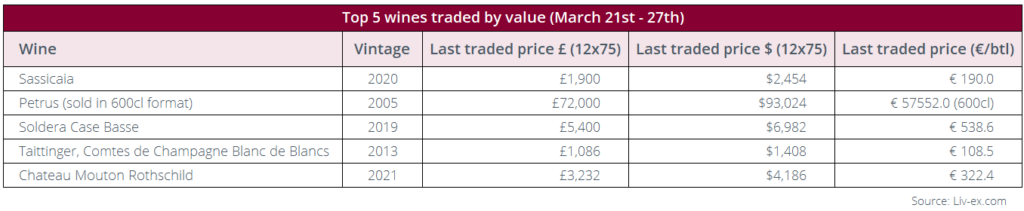

What were the week’s top-traded wines?

High volume trades at £1,880 / $2,428 / €190.0 per bottle resulted in Sassicaia 2020 being this week’s top-traded wine by value. So far in March, trade prices have been inconsistent, with a 26.1% spread between the low and high trade price. This week’s trade occurred in the middle of the range, 21.7% below the original ex-London release price of £2,400 / c.$2,882 per 12×75 or c.€224 per bottle.

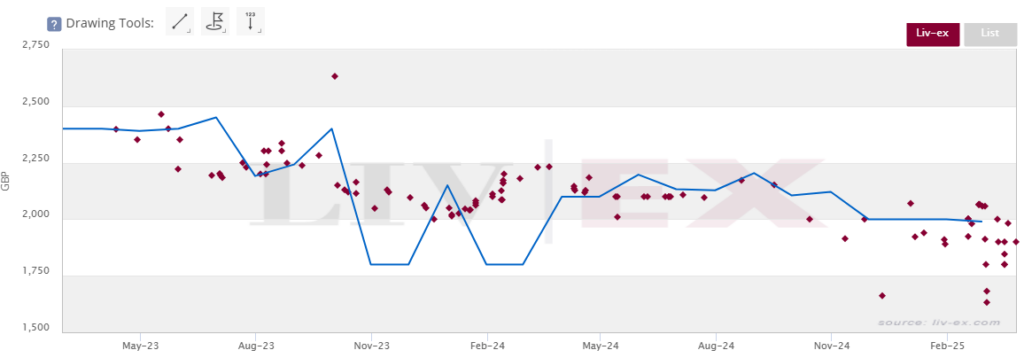

Liv-ex Trades of Sassicaia 2020

Petrus 2005 trade highlights large bottle premiums. This week saw a 600cl bottle trade at £48,000 / €62,016 / €57,552.0, equivalent to a 12×75 price of £72,000 / $93,024 or €7,194 per 1×75. This is double the current 12×75 Market Price, and 2.1x the value at which it last traded in 75cl bottles.

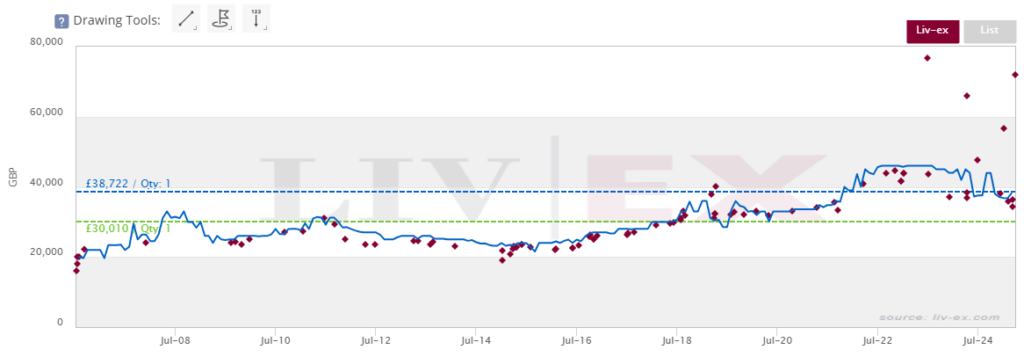

Liv-ex Trades of Petrus 2005

Top-traded wines by volume

Produttori del Barbaresco, Barbaresco is so far this year’s top-traded brand by volume, with both the 2020 and 2021 seeing considerable demand. This has predominantly been driven by US buyers who have accounted for 77.8% of the brand’s trade value. However, since Trump announced the threat of 200% tariffs a fortnight ago, US demand has completely dried up. This week 82.6% of the 2020’s trade value came from Asian buyers, with European buyers making up the remainder.

Weekly insights recap

This week, Liv-ex members were sent analysis of where the value is in recent Bordeaux First Growth vintages – the Lafite premium and Haut-Brion discount

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £140m of bids and offers across 20,000 wines.