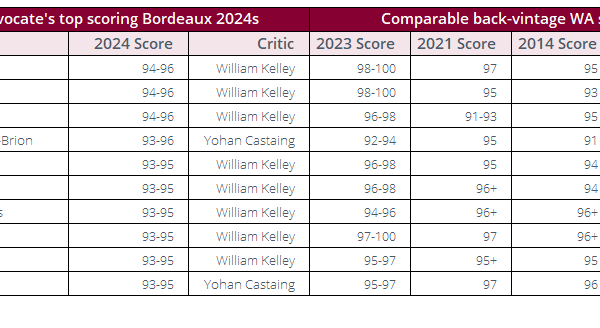

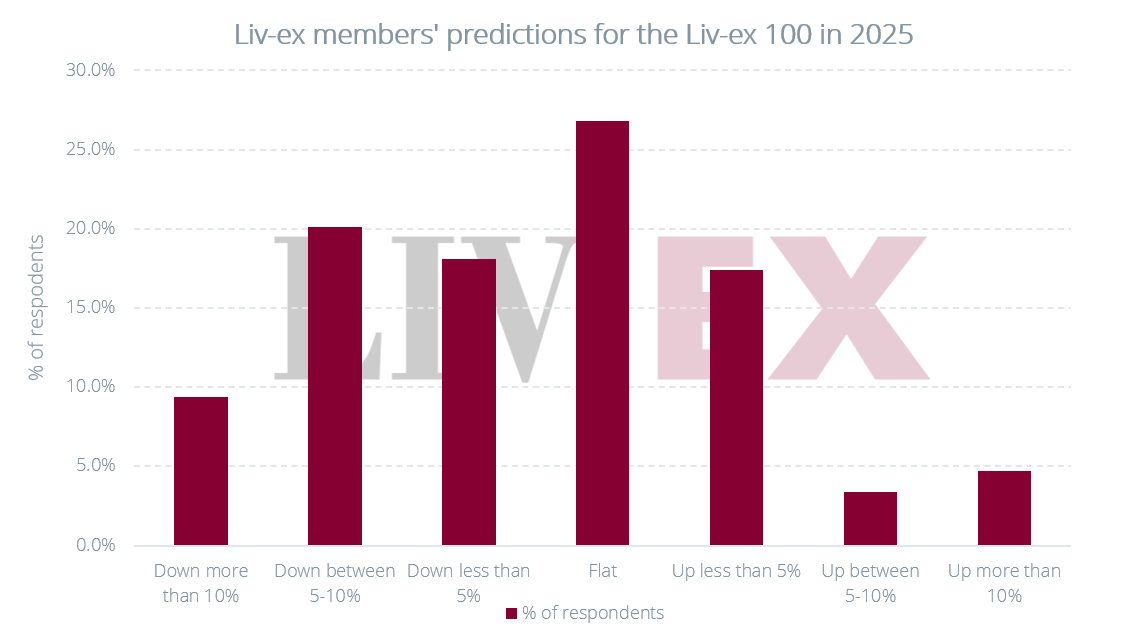

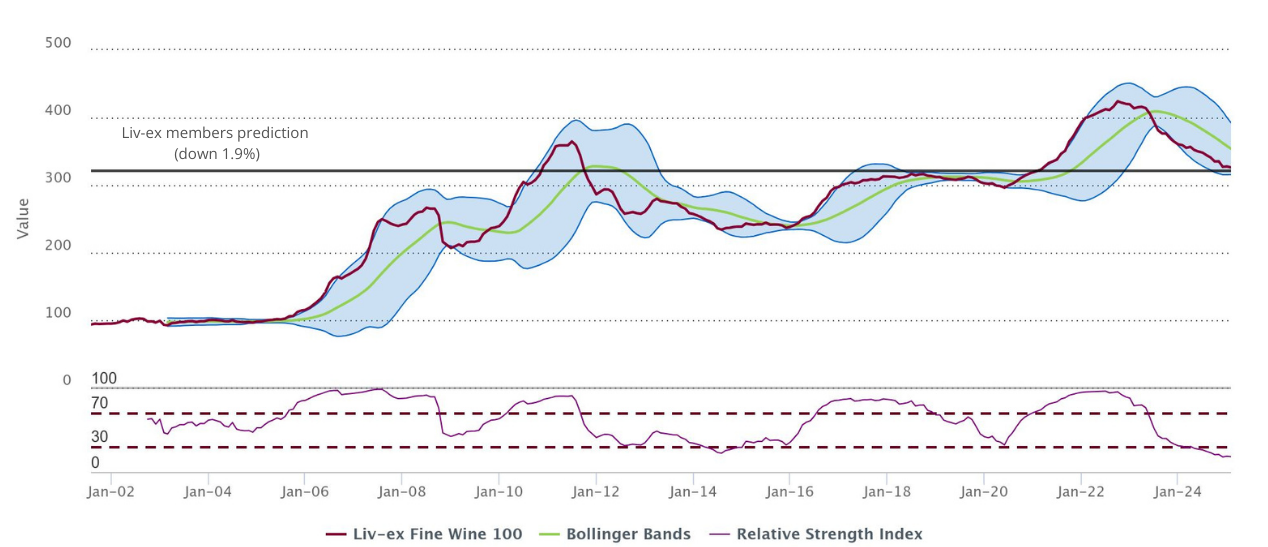

Earlier this month, we asked Liv-ex members whether the Fine Wine 100, the industry leading benchmark for fine wine prices, will be down, flat or up on its current index level (326.1) by the end of 2025. On average, respondents predicted that the index would fall by 1.9%, to close at 320 in December. This compares to a fall of 9.1% in 2024. The average prediction, as shown in the chart below, coincides closely with the index’s 2018 peak at 316.

Technical analysis of the Liv-ex Fine Wine 100

26.8% of respondents believe that the index will remain flat, making this the most popular choice. Several members reported that, while they don’t see prices falling much further – believing the post COVID correction to be over — the market, ‘having no impetus to rise’, will likely be slow to recover while sentiment gradually improves.

This is reflective of a general theme amongst respondents – most market participants feel that prices are close to bottoming out. According to one UK member, buyers are increasingly perceiving ‘incredible value’ at current prices. Another commented that ‘stocks of unsold wines are being eradicated’ as the market reaches end of 2021 levels.

Nevertheless, some members see room for further downward movement as the result of the wider macroeconomic and geopolitical landscape. Many respondents voiced concerns over looming US tariffs, high interest rates, inflationary pressures and general economic uncertainty.

Less than 10% of respondents believe the index will close in December over 5% above its current level. While the worst may have already passed, the market remains far from bullish. As we recently reported, steadiness, rather than immediate price increases, might be the remedy required to reset the market.

Which regions were the most optimistic?

While making up a smaller portion of the voting pool (4.7%), Asian respondents were the most optimistic. On average, they predicted a 1.4% decline over 2025.

US and UK respondents were next most optimistic, each predicting, on average, 1.7% decline.

EU merchants were the least optimistic, with 50% of respondents predicting that the Liv-ex Fine Wine 100 will fall over the course of the year, bringing the average to a 2.2% decline.

Which types of businesses were most optimistic?

Wine investment businesses were the most optimistic of any segment, estimating an average 1.2% increase. On the other hand, merchants who primarily buy directly from producers were the least optimistic, estimating a 3.9% decline.

This may be reflective of the speed at which prices begin to align with market conditions at each stage of the supply chain. Trade prices tend to fall first, followed by the most competitive merchants and then the wider market. Producers have been slow to correct their pricing. Of the merchants who predicted more serious declines, many cited fears of another year of poor release pricing, and concerns over the supply-demand imbalance.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £140m of bids and offers across 20,000 wines.