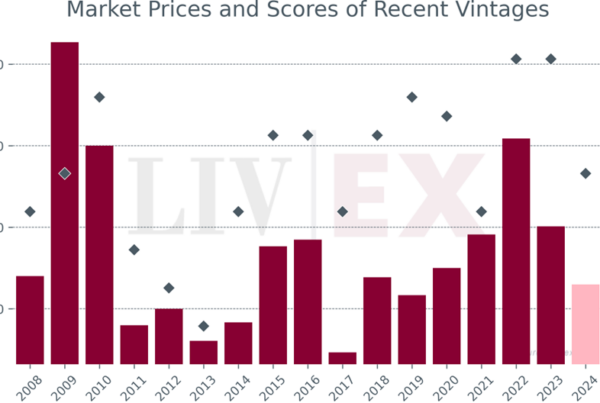

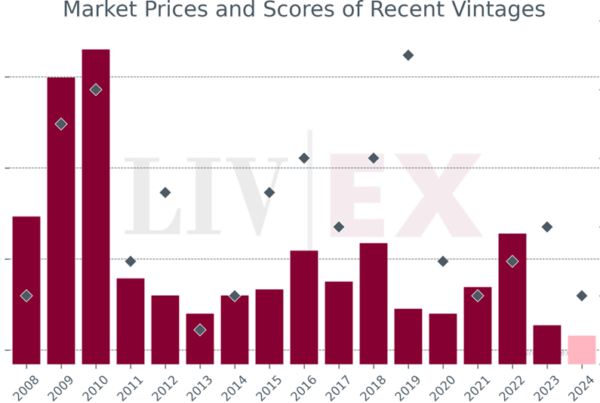

What’s happening in the market?

Burgundy and Bordeaux are neck-and-neck as the top traded regions by value this week. Domaine de la Romanée-Conti is in lead as the top-traded producer by value, with Château Lafite Rothschild in second place.

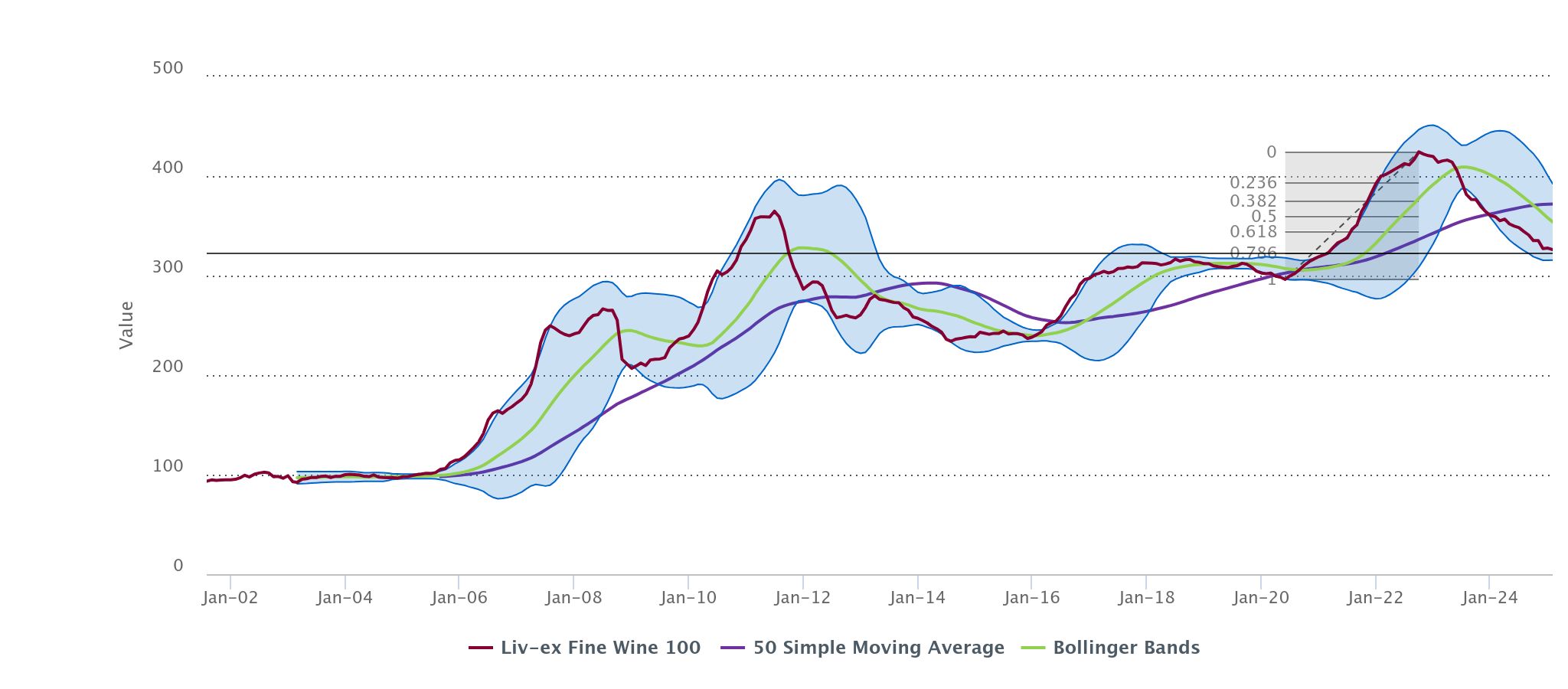

Today’s deep dive: potential price floors of the Liv-ex 1000’s sub-indices

Earlier this week, we published the results of a survey sent to Liv-ex members, where we asked for their predictions on the price performance of the Liv-ex Fine Wine 100 in 2025. On average, they predicted that the index would close in December 2025 1.9% down on its current level (326.1). This level happens to coincide with an attractive support zone for the Liv-ex 100 – the convergence of the Lower Bollinger Band, 78.6% Fibonacci retracement level, and 2018 peak, all around the 316-320 level.

Technical analysis of the Liv-ex 100

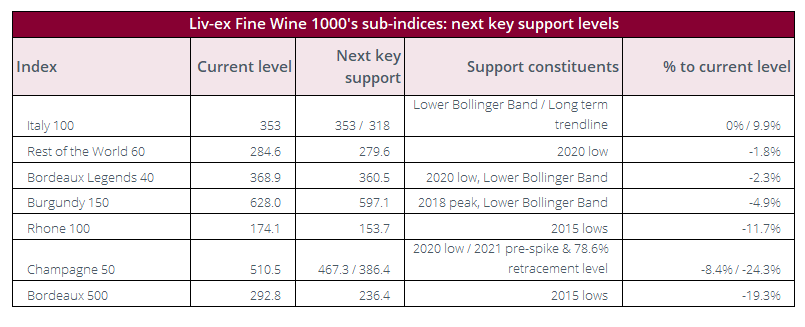

Many members believe that prices will find their floor this year, but the end is closer in sight for some regions than others. Expanding the pool of wines, where does technical analysis indicate support levels might lie for the Liv-ex 1000‘s sub-indices?

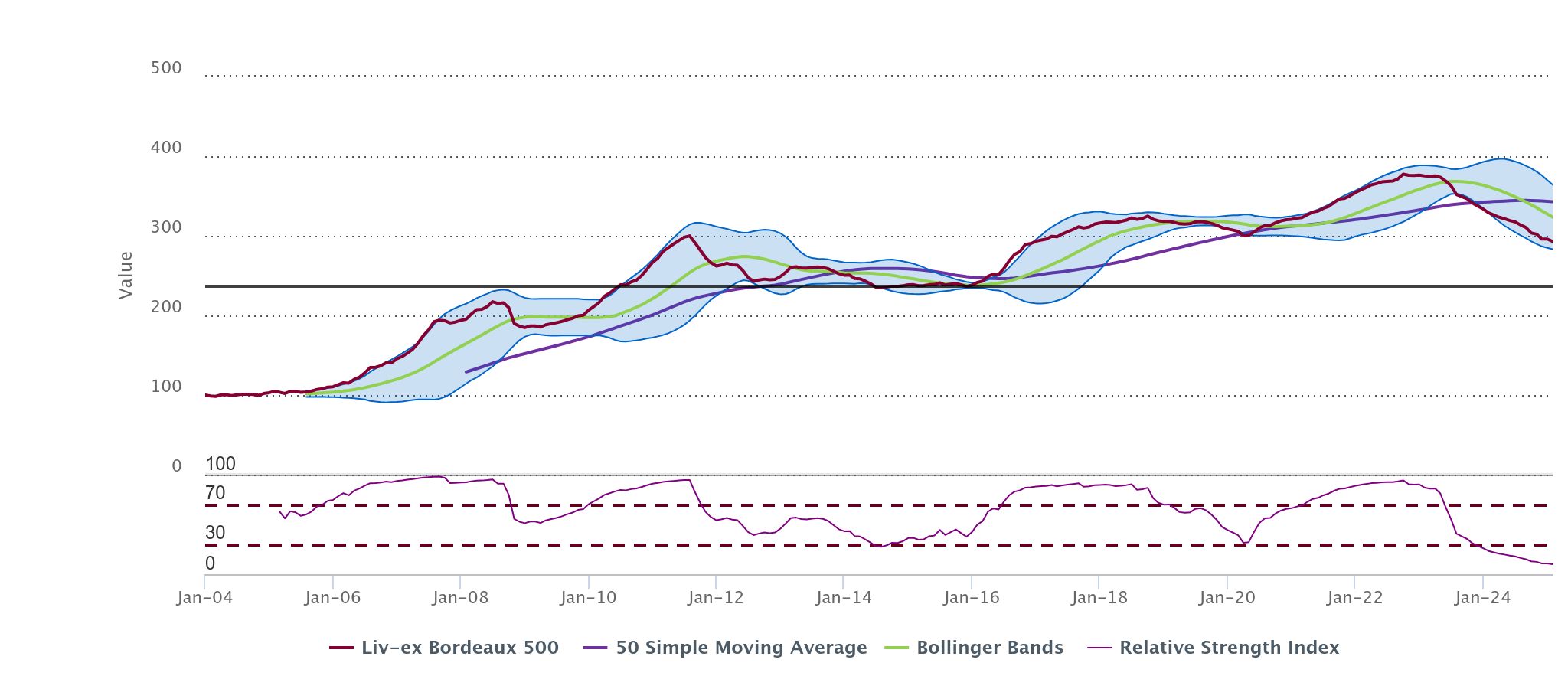

The Bordeaux 500’s next critical support level appears especially low. The index has already crossed below its 2020 lows and long-term trendlines, and bearish sentiment does not appear to be letting up. While the Bollinger Bands are narrowing slightly, indicating reduced volatility, the lower band continues to widen. Invisible supports in the form of release prices may hold in some cases, but technical analysis does not, at this stage, indicate the likelihood of swift recovery.

Technical analysis of the Bordeaux 500

By contrast, the Bordeaux Legends 40 sits much closer to its next support (just 2.3% below). High release pricing of recent vintages may make the difference here; having had more time to circulate through the market, more mature vintages are more closely tracking broader (international) indices, while sellers are reluctant to drop prices of recent vintages below cost.

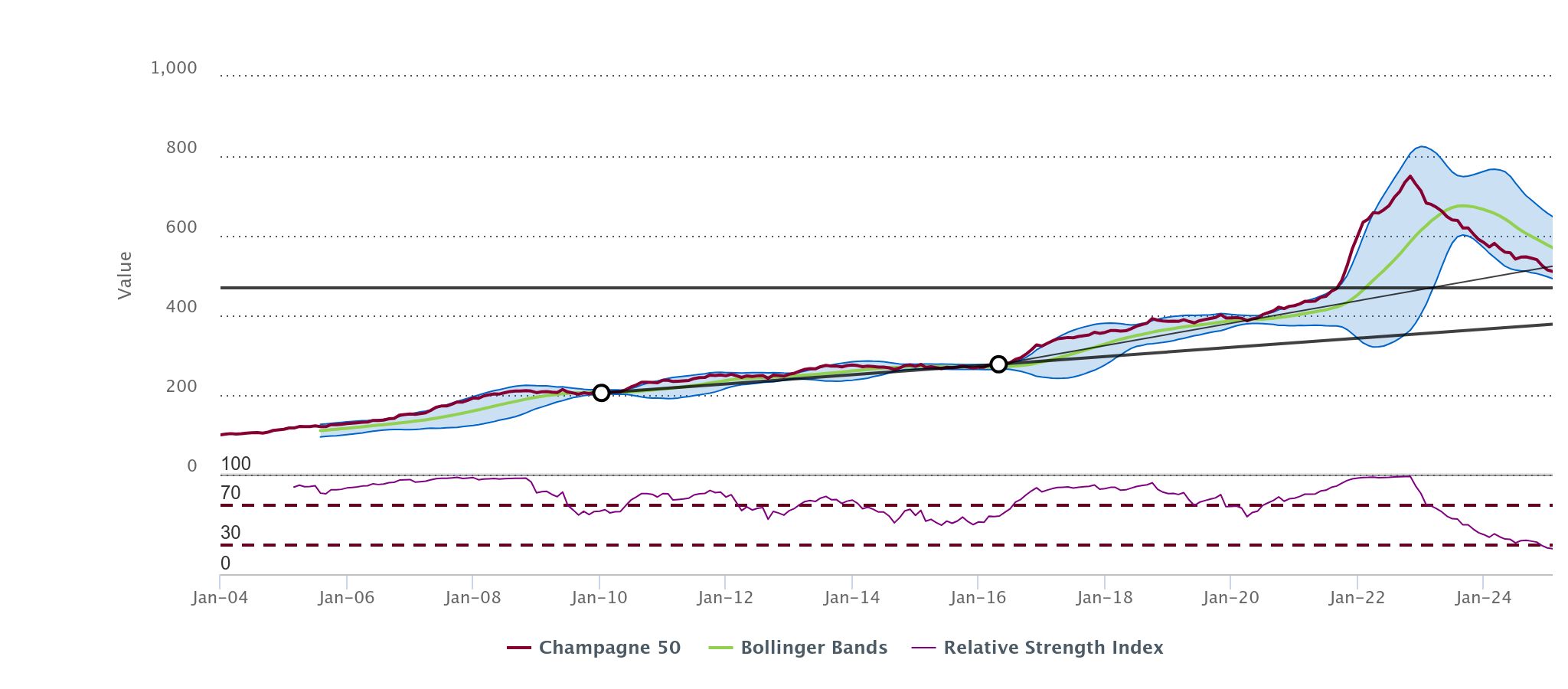

The Champagne 50 presents an interesting case. The index rose very quickly during the 2021-22 bull run and is undergoing a severe correction. While some individual components are nearing key support levels (i.e. Cristal, as detailed here), there is little support available for the overall index. Having crossed below its accelerated trendline, its longer-term trendline, coinciding with its 2020 low, now presents as the next critical support. This support, however, sits 24.3% below its current level. Intuitively, it seems unlikely that prices of many individual components will fall quite so far. While the less frequently traded and higher-priced labels (such as Jacques Selosse) may still be a way off the mark, others (such as the 2008 vintage of the Grand Marques) are seeing price consolidation in high volumes. Given this, the index may find support at a less technically attractive level 8.4% below its current level – its 2021 low, prior to the spike in prices, which coincides with the 78.6% retracement level.

Technical analysis of the Champagne 50

The Italy 100, having risen more sustainably in 2021-2022, has performed well through the downturn of the market. In December, it bounced from its Lower Bollinger Band, its RSI rejecting oversold territory, and has been trending slightly upwards since. The outlook for the Italy 100 is largely positive, but very low volatility does create the risk of a price squeeze, which in turn could result in downward price movement. Should this be the case, support lies not too far below on its long term trendline.

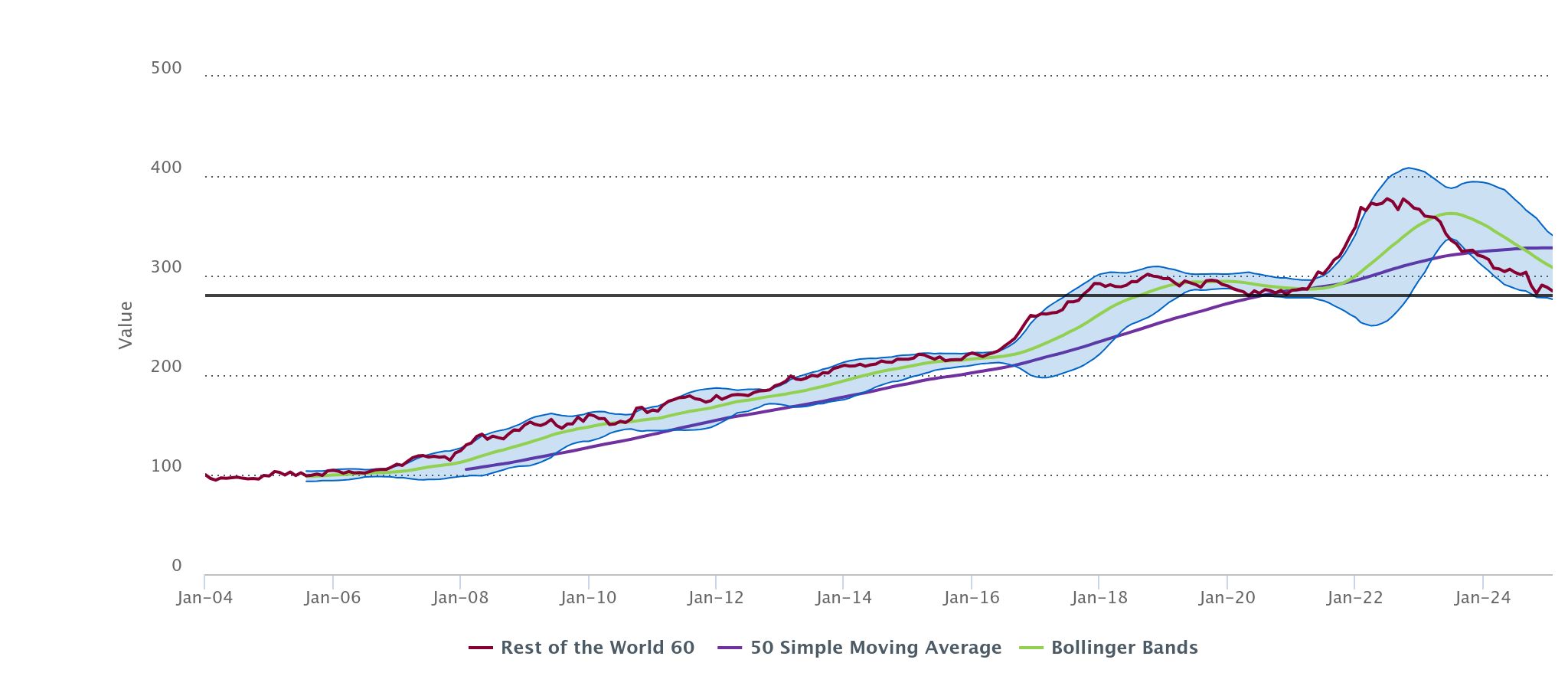

Promisingly, the Rest of the World 60 has already tested and found support at its 2020 low. If prices can once again find support here, this will form a double bottom – a promising sign that the index has found its floor.

Technical analysis of the Rest of the World 60

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.