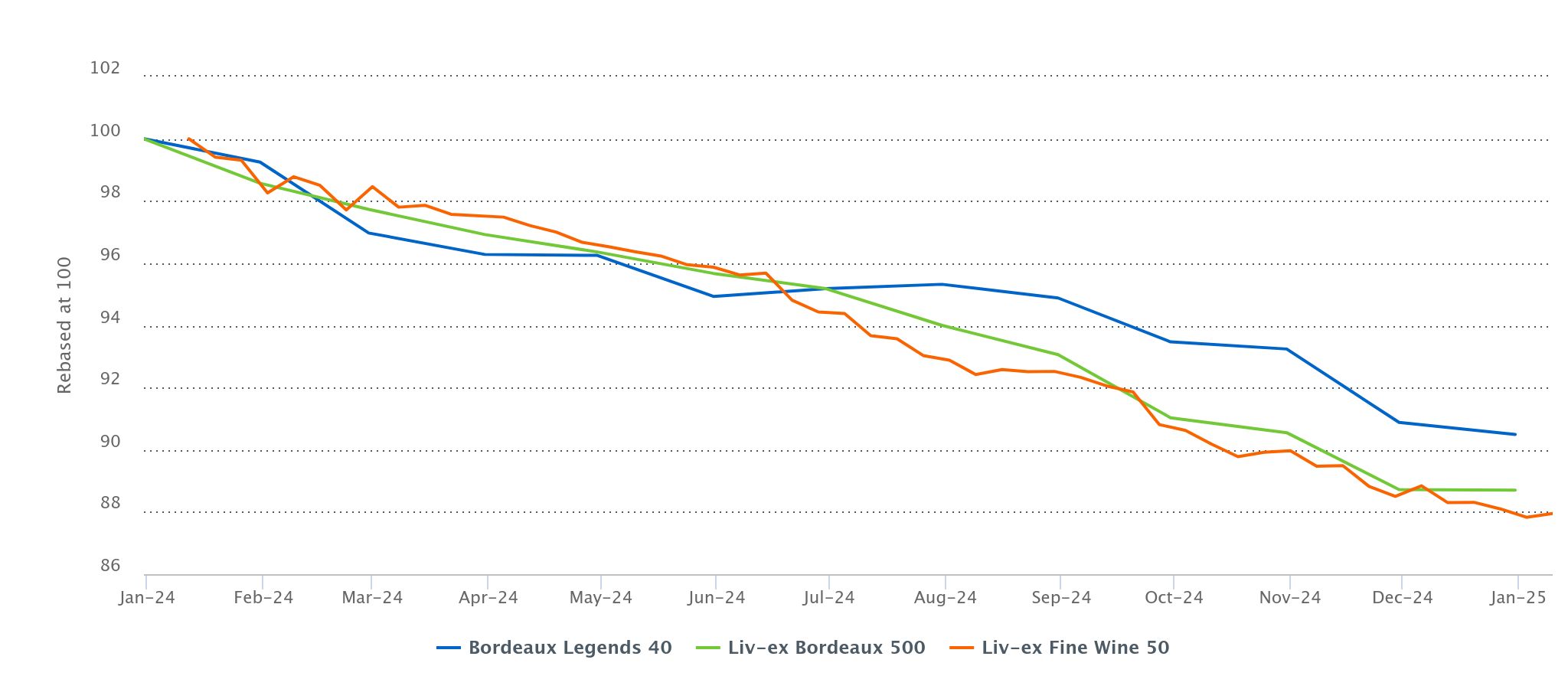

- Having fallen 2.5% in November, last month the Liv-ex Fine Wine 100 found a degree of stability, ticking up 0.2%. The wider market, represented by the Liv-ex Fine Wine 1000, fell 0.6%.

- In early 2024, the exchange’s overall bid:offer ratio dropped to new lows but recovered slightly towards the end of the year, possibly forming the beginnings of an upward trend. Still, it sits well below 0.5, a threshold we have previously identified as an indicator of price stability.

- Monetary policy and changes in exchange rates over the coming year may provide market participants with some respite, but merchants are more likely to look at producers to reduce release prices in a bid to awaken the market.

Introduction

Having fallen 2.5% in November, last month the Liv-ex Fine Wine 100 found a degree of stability, ticking up 0.2%. This mirrors what we saw in October, when the LX100 recorded a similarly modest rise (0.1%) after a sharp fall in September (-1.7%).

The wider market, represented by the Liv-ex Fine Wine 1000, fell 0.6%. The Champagne 50 closed 2.1% down, making it the worst performing sub-index of the LX1000. Burgundy, on which the eyes of the industry are trained during January and which, like Champagne, soared in value during the Covid bull run, experienced another tough month, with the Burgundy 150 falling 0.9%. The Rhone 100, which has to some degree been stuck in the doldrums with total trade share hovering resolutely around the 3.0% mark, was the only sub-index to record a rise (+0.2%).

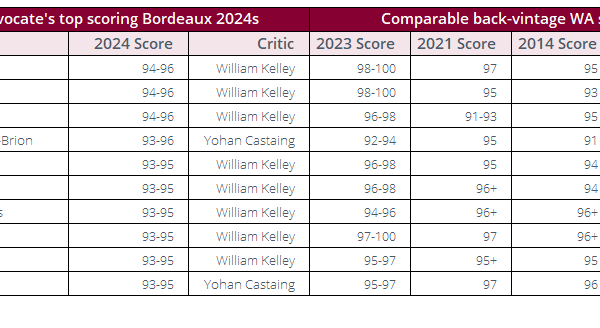

Turning attention to Bordeaux, the Fine Wine 50, which records the daily price movements of the First Growths, fell 0.1%. The wider Bordeaux market, represented by the Bordeaux 500 was flat on November. The Bordeaux Legends 40, which is comprised of back vintage blue-chip Bordeaux, fell 0.4% to close 2024 down 9.5%. While the demand-supply balance of the Legends 40 has tended to remain more stable than that of more recent vintages, it has not prevented the prices falling over the past 12 months.

Trade activity

While December saw much of the market close down for festivities, activity was significantly higher than December 2023. Trade count was up 22.3%, trade volume was up 14.3%, and trade value was up 4.1%.

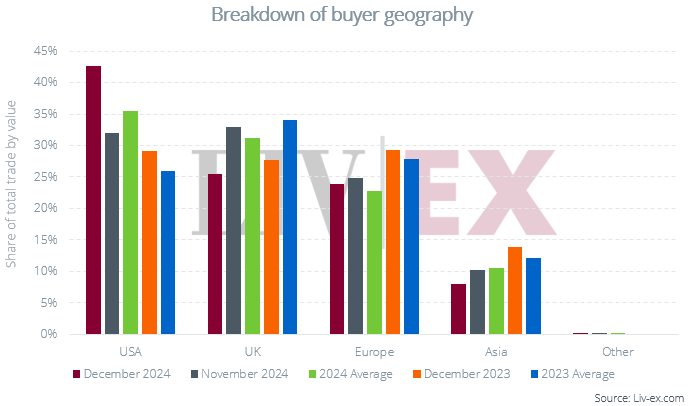

Buyer geography

Focusing on buyer geography, US merchants accounted for 42.6% of purchases in December 2024. This is a marked difference to December 2023, when the division of purchases was split much more evenly between US, European and UK buyers. While one month’s performance should not be taken in isolation, it is representative of a longer-term shift with US buyers coming increasingly to the fore. As we reported, 2024 was the first year that US buyers accounted for the lion’s share of purchases. Towards the end of this report, we cover some of the wider macroeconomic factors that may have contributed to this shift.

2025 market sentiment temperature check

Considering the exchange’s overall bid:offer ratio alongside the major Liv-ex indices, there exists a clear positive correlation. Drops in the bid:offer have historically predated bearish trend reversals, while increases occur in closer tandem with bullish reversals. In early 2024, the exchange’s overall ratio dropped to new lows but recovered slightly towards the end of the year, potentially forming the beginnings of an upward trend. Still, it sits well below 0.5, a threshold we have previously identified as an indicator of price stability.

Bid:offer ratio vs. Liv-ex indices since 2015

Since December, the bid:offer ratios of all major Liv-ex Indices – the Fine Wine 50, 100 and 1000 and Bordeaux 500 – have declined. The vast majority of sub-indices also took hits. The resilient Italy 100‘s ratio rose 0.1 to close with a monthly average of 0.65 — its highest in the past year. The Burgundy 150’s ratio recorded a modest 0.01 increase, but remained one of the lowest at 0.18. All other indices now sit below 0.5.

N.B. If you are interested in receiving regular updates on the bid:offer ratios of Liv-ex’s major indices or tailored specifically to your list, speak to your account manager.

As we reported in August, Masseto has remained in the lead with the highest bid:offer ratio of the Italy 100’s component wines. The wine’s ratio has continued to rise (from 1.05 in August to 1.71 this month) and prices have responded in kind. Of the ten component vintages, seven have seen month-on-month price increases. Only 20 wines in the Italy 100 are up over a one-year period, and six of these are Masseto. Ornellaia’s bid:offer ratio rose from 0.45 in November to 0.83 in December and has sustained at 0.79 so far this year. Should demand continue to remain healthy, prices of Ornellaia may also be set to stabilise.

At 0.05, the Sauternes 50 currently has the lowest bid:offer ratio of any Liv-ex index. Given tastes generally moving away from sweet wines, this may not come as a surprise. Even Château d’Yquem, the most frequently traded and highest value Sauternes on the market, has a current ratio of 0.10. The Rest of the World 60 follows with a ratio of 0.16. Given that buyers are expanding the breadth of their purchasing, this may be counterintuitive. Within the Rest of the World 60, some wines are indeed seeing stable demand. The 10 most recent vintages of Vega Sicilia Unico and Opus One have ratios of 0.59 and 0.47 respectively. Screaming Eagle Oakville Cabernet Sauvignon, Sena and Dominus’ ratios sit vanishingly low at 0.04, 0.05 and 0.06 respectively. Penfolds Grange’s ratio is only marginally better at 0.10.

The Fine Wine 50, Second Wine 50 and Bordeaux Legends 40 have seen the harshest drops in their bid:offer ratios over a 12-month period – each by upwards of 0.43. The signal here is clear – even the best vintages of Bordeaux’s top châteaux are suffering from demand-supply imbalances. With over 20,000 cases of each wine produced every year and stockholders reluctant to sell lower than cost, offer prices have evidently not fallen low enough to invigorate demand.

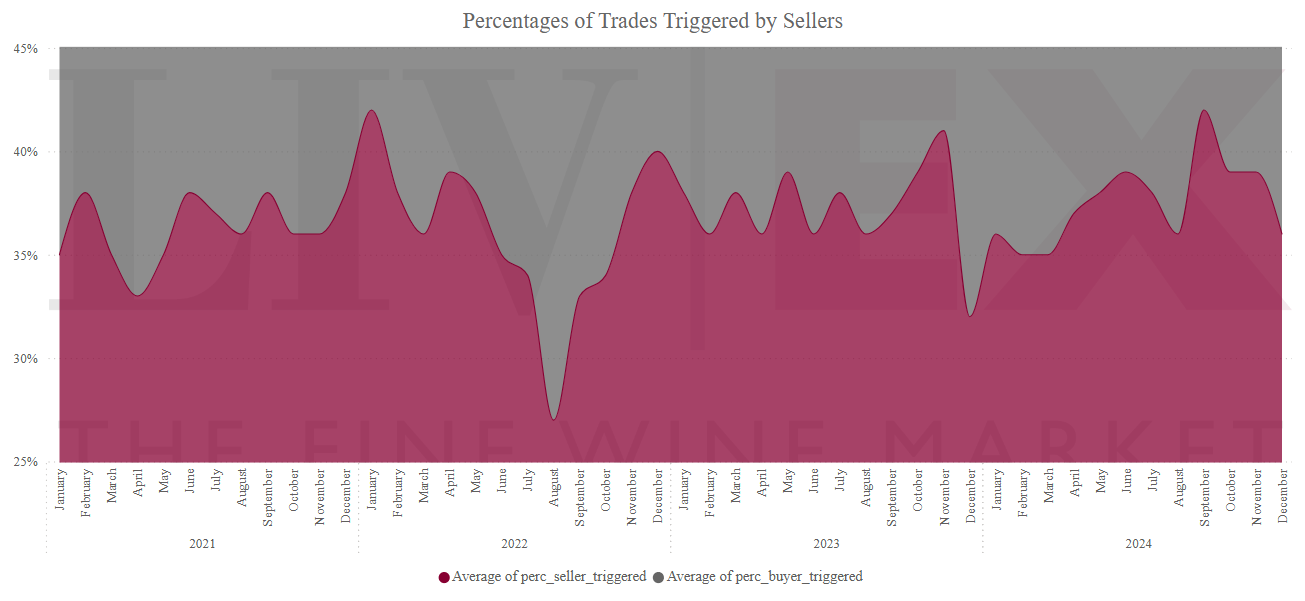

With supply outweighing demand for the majority of wines, buyers are endowed with a degree of power in the market – they are more likely to succeed in drawing sellers down to meet their bids than in more favorable market conditions. In December, 36% of trades were triggered by sellers (either moving down or directly meeting bids). Aside from brief troughs and peaks, the % of trades triggered by sellers appears to hold at this equilibrium level (its four-year average).

Can monetary easing end the slump?

- While there is no firm consensus on how interest rates will develop in 2025, monetary policy is generally expected to be more restrictive than previously anticipated

- While UK and US buyers would benefit from Sterling and Dollar strength, châteaux will be hoping for a weakening of the Euro to allow them to cut release prices less aggressively

- Though the wine trade does not exist outside of the global economy, it is unlikely that changes in monetary policy and foreign exchange rates alone will sufficiently reinvigorate the market. Rather than looking to central banks, merchants are more likely to look at producers to reduce release prices in a bid to shake up the system

The wine trade has seen an undeniably difficult two years. Older, traditional collectors have no need for wines that require an additional 15 years of ageing – their cellars are already full. The tastes of younger consumers are changing, and unrealistic release prices out of Bordeaux and Burgundy are in any case boxing them out. Moreover, châteaux, domaines and négociants can no longer rely on strong demand from an active Chinese market. In all, the trade is suffering from a serious demand-supply imbalance – one that is exacerbated by the broader economic climate. Market participants will no doubt need to adapt and make changes themselves, but not everything can be within their control. How have changes in monetary policy and foreign exchange rates impacted the fine wine market, and what should participants hope for over the coming year?

As a relatively expensive good, demand for fine wine is reliant on the availability of consumers’ disposable income. Interest rate cuts, decreasing the cost of borrowing, should, in theory, increase discretionary spending. Lower borrowing costs should also free up capital to hold more stock than strictly necessary. As such, lower interest rates should have a positive impact on the wine industry.

Still, these positive effects may be neutralised by rising inflation (reducing disposable income) and the increasing costs of running businesses. Lower interest rates are of little use to merchants if they don’t lead to increased demand for their wines. Moreover, unless merchants can draw in the next generation of potential buyers and consumers, disposable income is more likely to be spent elsewhere.

With inflation in the UK rising above the target 2% threshold and the October Budget causing concern over further inflationary pressure, it is unlikely that the UK will see cuts in Q1 2025. Nevertheless, the OECD predicts rates to fall to 3.5% by 2026, 125 basis points below the current rate.

As is the case in the UK, the US Federal Reserve is expected to cut rates at a slower pace than previously anticipated. The Fed announced three consecutive cuts in late 2024, down from a high of 5.33% in August to 4.48% in December but now forecast only two cuts in 2025.

As Trump’s tariffs pose a looming threat to European exports and thus growth, it had been expected that the ECB would continue to gradually cut interest rates in 2025. With inflation exceeding expected levels in some key countries, however, these cuts too, may be in jeopardy. Still, the outlook for ECB rates is somewhat rosier than Fed and BofE rates. While holding interest rates higher for longer doesn’t suggest good news, should the ECB continue to cut rates faster than the Fed and Bank of England, Sterling and Dollar buyers may benefit from an improvement in exchange rates, meaning greater purchasing power of European wines. At scale, slight improvements in these exchange rates are not negligible.

Recent En Primeur campaigns have been largely unsuccessful, with prices dropping below ex-négociant, and, in some cases, ex-château levels. For example, we are seeing transactions for 2021 Bordeaux go through the market at discounts to the ex-chateau release of up to 15% – that is 40% below international release prices. Twenty-five years ago, in the first year of Liv-ex, the 1997 vintage was cleared at similar discounts.

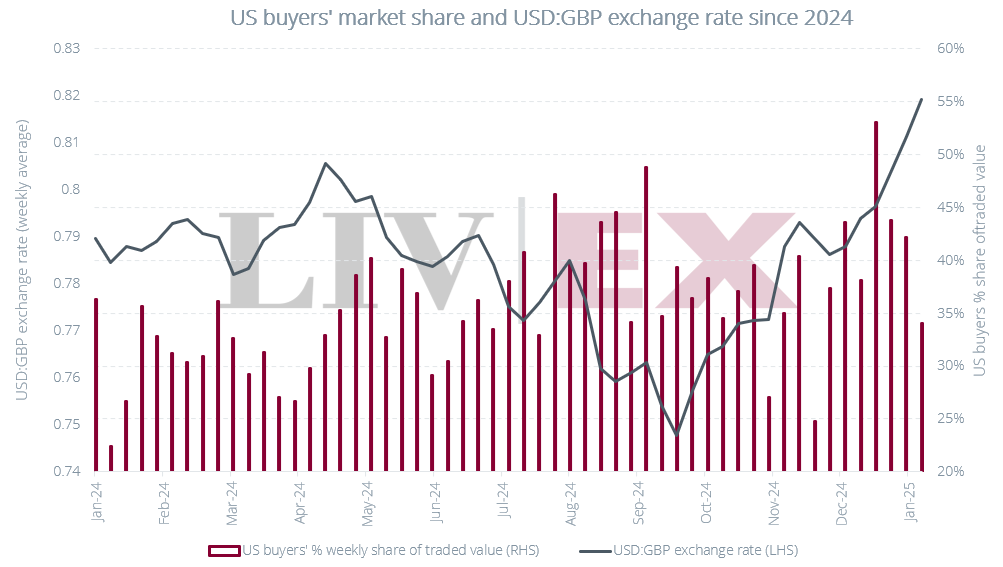

Exchange rates behave unpredictably – there is no consensus as to how Sterling and the Dollar will move against each other in the coming year. While the US Dollar has strengthened since the start of the year, HSBC argues that a ‘stronger Dollar [in 2025] isn’t guaranteed’ and UBS takes a harder line that ‘there is still scope to fall’, recommending investors use current strength to reduce exposure in US markets. The coming months may pose risks to US wine businesses, but for the time being, they remain the steadiest buyers in the market. With US buyers accounting for 35.5% of purchasing in 2024, a restrictive tariff policy and/or Dollar weakness would be considered unhelpful additional challenges to the market in 2025.

But regardless of these macro-economic uncertainties something much more fundamental is perhaps required to lift the market out of its current slump. In the absence of renewed and significant demand from Asia (read China), bold and meaningful cuts in release prices of the 2024 Bordeaux vintage will be fundamental to “bring the magic back”.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.