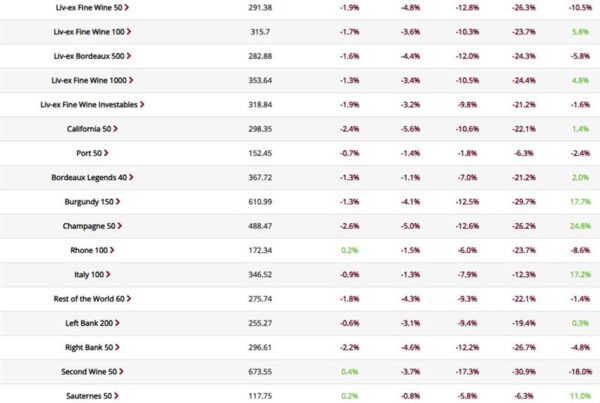

What’s happening in the market?

Burgundy and Bordeaux are neck-and-neck in the market, vying for this week’s top-traded region by value. Chrisophe Roumier’s Vosne-Romanee Beaumonts 1985 and Petrus 2010 are the regions’ top-traded wines respectively.

The US has had a strong week so far, taking 8.6% of traded value. UK buyers have accounted for 46.3% of US wine buying, and US buyers, 28.6%. Harlan Estate 2018 sits in the top spot by value overall.

Today’s deep dive: how high is too high? Pricing vs scarcity in Champagne

In theory, scarcity should protect the supply-demand balance of a given wine. And yet, we continue to see wines produced in tiny quantities and mature vintages see some of the lowest bid:offer ratios in the market. If priced correctly, these are the wines that should draw the most demand relative to their supply. At the peak of the market, it was indeed these wines that saw the highest bid:offer ratios. Prices, however, soared to a point that scarcity could no longer uphold, prices at which supply far outweighs demand, and trade begins to slow.

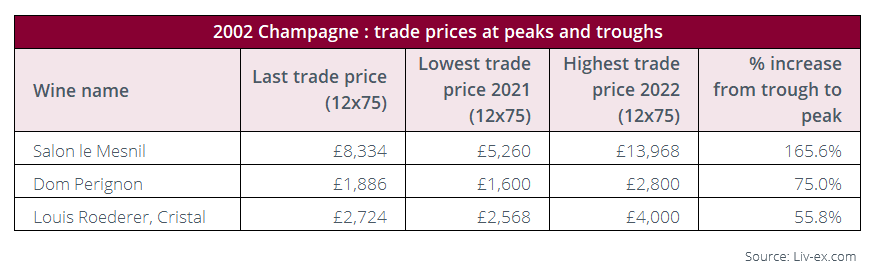

The correct price:scarcity balance is unique to each region, producer and wine. It rests not just on production numbers, but a wine’s quality, heritage and brand power. Today, we consider representatives of high and low production Champagne – Salon, Dom Pérignon and Louis Roederer’s Cristal, assessing the differences in the market’s response to price increases and decreases.

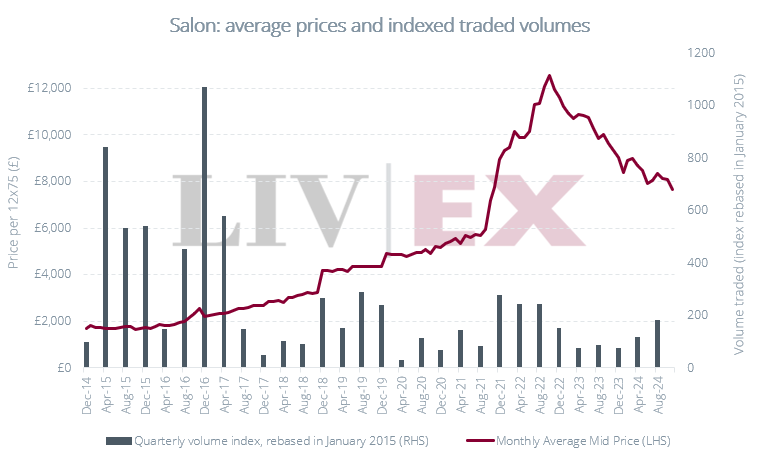

Salon produces significantly less of its flagship vintage than Dom Pérignon or Louis Roederer – an estimated 5,000 vs 50,000 12×75 cases. During the bull run starting in early 2021, trade prices of Cristal 2002 rose by 55.8%, Dom Pérignon 2002 by 75.0% and Salon 2002 by 165.6% (considering the lowest and highest 75cl SIB trade prices). Perhaps at play here is the idea that while prices are rising, nominal margins are higher when purchasing higher value wines. Salon’s price, already substantially higher than its peer group, might have been further driven up by the idea that those who purchased at the right time would see large returns, and that only a select few would be able to obtain bottles.

While prices of Salon rose considerably in 2021, they already sat much higher than those of Dom Pérignon, Cristal and most other major Champagne houses. Average prices had more than doubled between 2015 and 2020. With this price increase, traded volumes trailed off. While the start of the bull run invigorated demand, this was short-lived – buyers were either unable or unwilling to keep up with soaring prices. Salon’s price levels were not proportionate to its scarcity. Only 8,000 bottles (only magnums) of the 2008 vintage of Salon were produced. Released at more than double the price (ml for ml) of any other vintage, it has only traded twice in the past five years. In recent months, with prices of Salon dipping below the £8,000 per 12×75 mark (averaged across the 2006, 2007, 2012 and 2013 vintages), we are once again seeing demand increase.

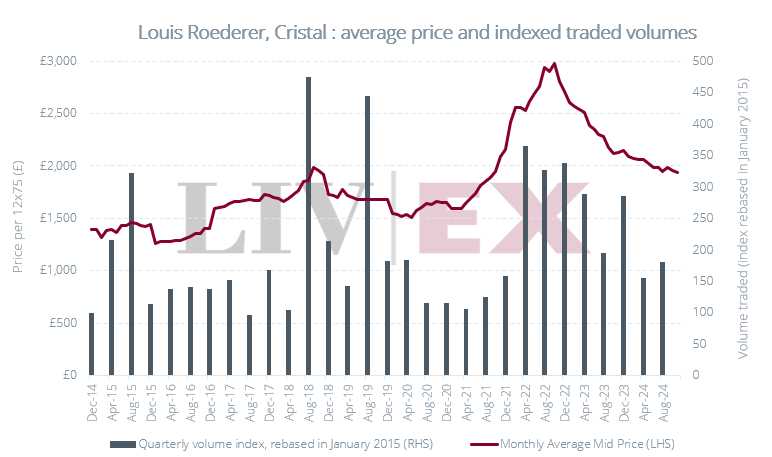

N.B. The average prices of this and the following graphs were determined using an average of the Mid Prices of vintages that were included at each period in the Champagne 50. For Salon, four vintages; Dom Pérignon, five; for Cristal, six. In general, these are the most recent vintages that are actively trading (on a rolling basis). Traded volumes were summed quarterly and indexed, rebasing at 100 for the January-April 2015 period.

By contrast, Dom Pérignon, whose prices remained relatively flat in the five years prior to 2021, saw large increases in trade volumes. Though these volumes increased with the rise of the market, they show their sharpest increases at times when prices have fallen. Buyers may be looking to capitalise on rising prices during up markets, but to a greater degree, they are turning to the likes of Dom Pérignon for value relative to quality. Averaged across component vintages, Dom Pérignon is the 4th cheapest wine of the 16 included in the Champagne 50, with an 95.3-point score average from Antonio Galloni (Vinous). Paired with the commercial power of the brand and the frequency with which it is bought and drunk by consumers, it presents a reliable opportunity for merchants. Buyers appear to have some faith in price stability – falling prices are not met with buyers backing away, but rather taking discounts when they can.

Volumes traded of Cristal behave more similarly to Dom Pérignon than Salon. They show the sharpest increases fairly consistently when prices reach the £2,000 per 12×75 mark. It is possible that this represents the point where buyers see the wine as inexpensive enough to provide relative value, and expensive enough that it does not appear inferior to its peer group.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £140m of bids and offers across 20,000 wines.