What’s happening in the market?

Burgundy and Bordeaux have dominated the market this week so far, taking a 41.0% and 31.8% share of traded value respectively.

Pomerol is in the spotlight — Petrus 2005, Le Pin 2009 and 2015 all changed hands in OWC, and are amongst the week’s top five traded wines by value.

Château Latour 2009 is in as the second top-traded wine of the week. Having been re-released at £11,000 per 12×75 ex-London, its price has fallen considerably, trading this week at £7,950.

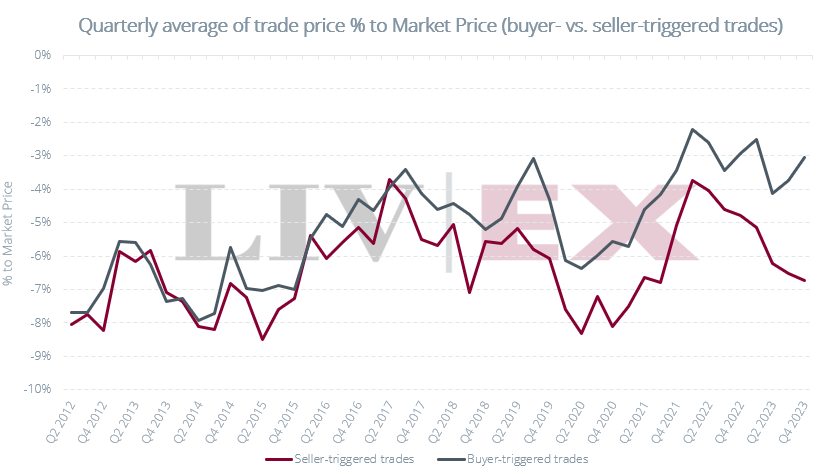

Today’s deep dive: trade prices vs. Market Prices in today’s market

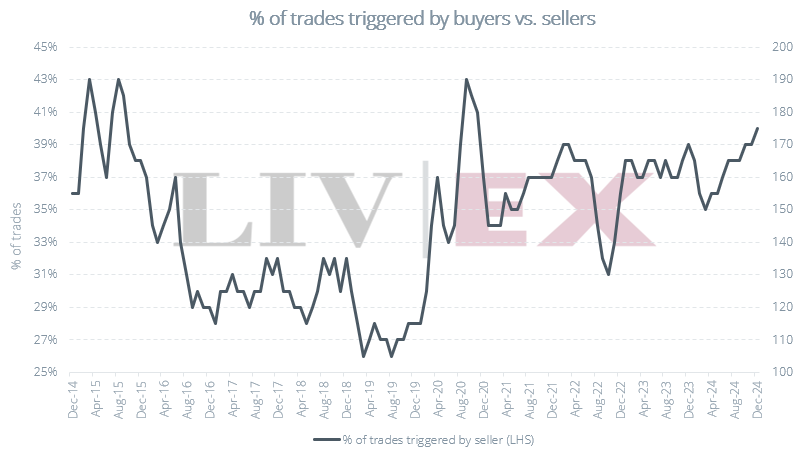

In recent months, we have seen an increasingly high percentage of sellers lowering their offers down to meet buyers where they are.

Since late 2022, there has been a notable divergence between the average % to Market Price of buyer- and seller-triggered trades. While seller-triggered trades are dropping well below Market Price, buyer-triggered trades have tracked Market Price fairly closely, generally taking place between 2% and 4% below. This figure has not fallen much since the turn of the market.

Rather than this indicating that buyers have been willing to pay the same prices as in an up market, this is likely down to Market Prices falling. For wines listed at the right prices, offers marginally below market may provide value to opportunistic buyers.

While the average % is volatile, there remains a long-term upward trend for buyers being more willing to step up to offers closer to Market Price. With increased competition in the industry, margins are narrowing. Under the pressure of current market conditions, this will come as no surprise to merchants.

Breakdown of % to Market Price by sub-index

Components of the Second Wine 50 have traded consistently well below their Market Prices this year, indicating a disconnect between buyers and sellers. As we reported in October, overinflation of the second-to-first wine price wine ratio and a subdued Chinese market have resulted in aggressive price corrections this year. While the market must come down, there is nevertheless hesitation to drop list prices below cost prices, thereby sacrificing profit.

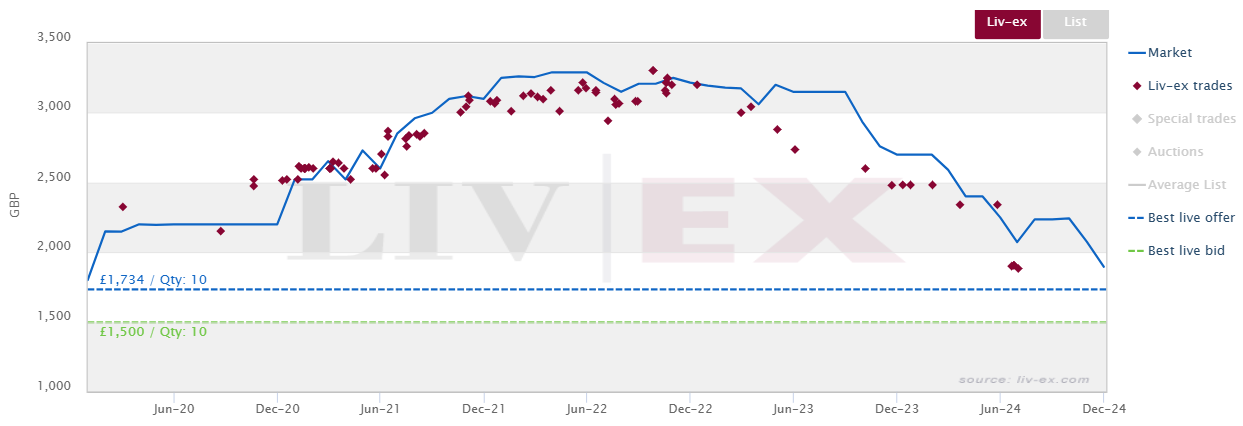

Trade activity of Carruades de Lafite 2018 illustrates this market interaction. Though its Market Price has fallen following months of inactivity to £1,833 per 12×75 (from £2,236 in July), the highest bid sits 18.2% below the new price, and the lowest offer, 5.4% below. There is still hope that prices can hold on the retail market, but a lack of activity at this price signals a lack of confidence that there is not yet further to fall.

Liv-ex trades of Carruades de Lafite 2018

In August, we reported on how far below Market Price trades were taking place for the Fine Wine 50’s components, suggesting that the gap may be closing slightly. This has remained the case – the average % has risen to -1.8% in Q4.

With the majority of component wines recording Mid Price losses over the past few months, it must be falling Market Prices rather than increasing trade prices closing the gap. When trade prices stray too far below market, merchants will eventually begin to lower their list prices – if wine can be acquired at lower prices, merchants will either be able to make the same margins without holding their list prices as high or accept a slightly lower margin. It is possible that this effect is also seasonal. With merchants clearing stock before year end, they may be further incentivised to drop list prices.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.