Domaine Leflaive is the top-traded producer so far this week, pushing Burgundy to a lead of the market with a 33.3% share of traded value. Bordeaux and Champagne follow with 23.7% and 14.2% respectively.

The Rhone has seen more active trade than usual, with several vintages of Domaine Jean Louis Chave’s Hermitage Rouge and Château Rayas Châteauneuf-du-Pape changing hands.

Today’s deep dive: the Power 100’s top 10 by traded value and volume

Earlier this week, Liv-ex published the 2024 Power 100, a ranking of fine wines brands by price performance; average price; number of individual vintages traded; and value and volume traded on Liv-ex this year. Today, we take a closer look at the top performers in the Power 100 in terms of traded value and volume, and explore the reasons why market dominance, for some, has resulted in a high overall ranking, but for others, has not.

Top 10 by Volume

N.B. Argiano ranked third by volume, but ranking at 187 overall, was not included in the Power 100 and thus has been omitted from this list.

Of the top ten brands listed above, prices of Tenuta San Guido’s wines have remained the most stable. While the producer’s second wine Guidalberto has also traded actively this year and seen remarkable stability (the 2021, 2018 and 2022 vintages serving as good examples), this has likely been driven by the great success of Sassicaia. Finding stability in a tough market has protected prices from rising artificially – the market has accepted release pricing as reasonable for the wine’s quality and heritage.

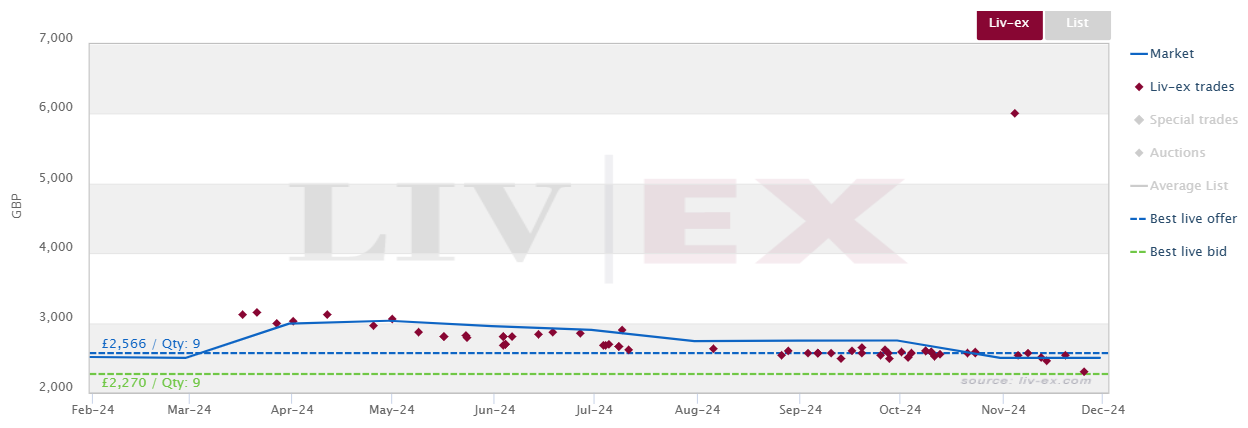

Liv-ex trades of Sassicaia 2021

Notably, three Grand Marques are amongst the top 10 brands by volume, with Bollinger just behind in 11th place. Louis Roederer and Dom Perignon were also featured amongst the top 10 by traded value. As we have previously noted, the commercial success of the Grand Marques has likely bolstered their trading activity. These more popular Champagne brands, held back by producers until ready to drink and opened in quantity at celebrations, are regularly bought and uncorked – more so than one would expect for similarly priced still wines. As such, wines purchased on the exchange can be sold onward with relative ease, presenting lower risk than more niche wines, despite downward price movements.

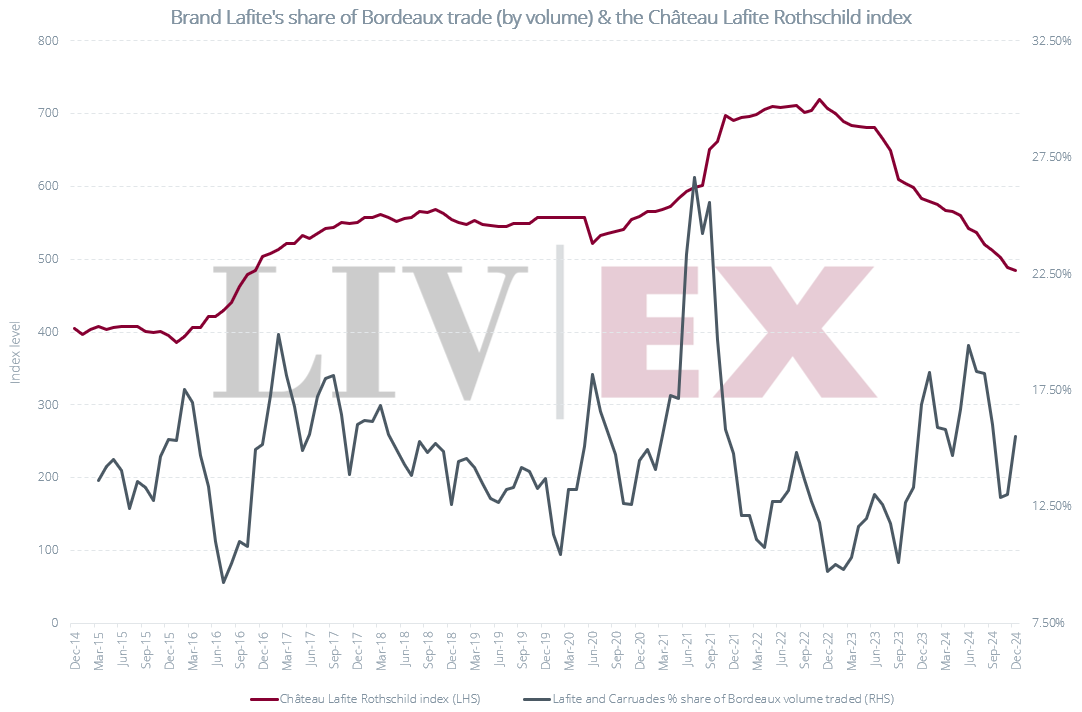

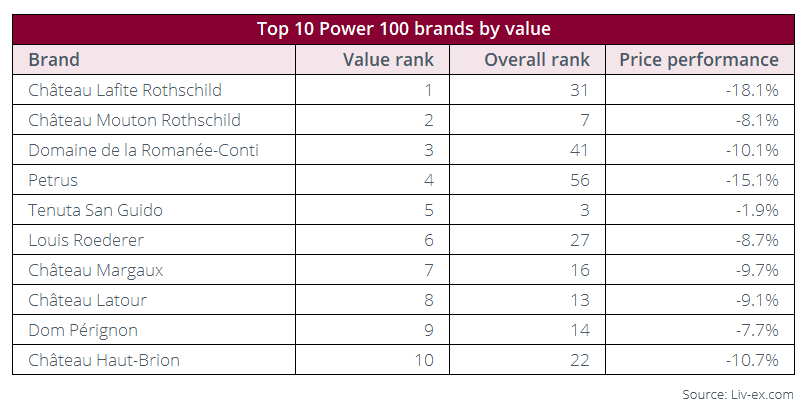

Château Lafite Rothschild, having only two labels, has traded more actively than any other brand this year. It stands head and shoulders above any other brand in terms of both volume and value traded – 22.1% more volume traded than Château Pontet-Canet and 89.3% more value than Château Mouton Rothschild. And yet, its Market Price has dropped by an average of 18.1% (across all vintages traded this year). Intuitively, healthy demand should somewhat protect prices – if volumes traded increase and prices stabilise, the market may have found an equilibrium price level. An increase in trading volumes as prices continue to drop, however, may instead indicate a growing need to offload stock. For every buyer, there is also a seller – if these sellers are increasingly willing to lower their prices, there may be cause for concern.

The spike in Lafite’s share of Bordeaux’s traded value in June 2021 may represent buyers’ confidence that prices would continue to rise. The recent spikes, however, may be more indicative of sellers’ concern prices might fall further than buyers’ confidence that prices have reached a floor.

Top 10 by value

Given the high prices of Petrus and Domaine de la Romanée-Conti wines, it will not come as a surprise that they feature amongst the list of top-traded by value but not by volume. We have recently published technical analyses of both the Petrus and DRC indices. Both are currently undergoing price corrections. Moreover, they have both seen fewer individual trades this year than last year. Not only were both victim to overinflation of prices, but their high price points may also be boxing them out in today’s market. With capital expensive and the industry at large feeling the pressure of downward momentum, buyers may be seeking lower risk wines, resulting in the lower-than-expected overall rankings.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.