- November saw each of the major Liv-ex indices record sharp falls. The Liv-ex 100 recorded its biggest fall of the year

- As Wine Spectator publishes its annual ‘Wines of the Year’ we look at how these awards impact trade

- Château Latour’s decision to withdraw from En Primeur has allowed it to watch as prices for recent vintages of its First Growth peers fall. Using technical analysis and the bid:offer ratio we analyse future price movements of Latour and how it might fare releasing new vintages into the market

- The US has played an increasingly important role in the fine wine market over recent years. We consider the role of the US in the market and the potential impact of Trump 2.0 and tariffs

Introduction

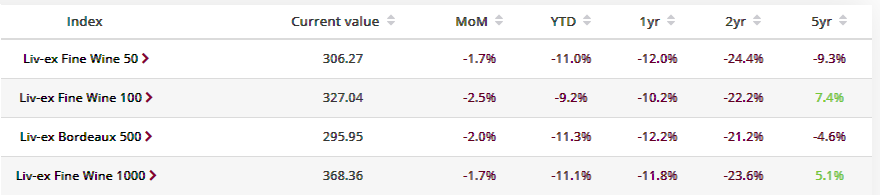

After some respite in October, November saw all of Liv-ex’s major indices record sharp falls. The Liv-ex 100 (the industry benchmark) fell 2.5%, its biggest fall of the year.

The Fine Wine 50 (which tracks the performance of the First Growths) and the Liv-ex 1000 (the broadest measure of the market) both fell 1.7%.

Having recorded the biggest falls of any Liv-ex 1000 sub-index in October, the California 50 and Rest of the World 60 regained some ground, rising 2.8% and 3.0% respectively.

While the Italy 100 still remains a beacon of relative stability amidst the wider market’s more severe downturn, this month it fell 2.3%. For the first time since the index’s inception, it has fallen into oversold territory (indicated by a Relative Strength Index level of below 30).

Despite the downward price movements, market participants have remained active. November saw the second highest trade volume of the year. Notably, the percentage of trades triggered by sellers has risen over recent months. It appears merchants are lowering their offers to meet bids in an effort to clear stock before the end of the year. For those with capital to spare, now may be the time to place bids.

Wines of the year – how do trade and prices respond?

As the year draws to a close, Wine Spectator has published its annual ‘Wines of the Year’ list. In some past cases, the release of this list has triggered a flurry of trade and subsequent price increases. Taking a few examples from recent years, we examine which wines are primed to see trade increases and which are not. Moreover, if the award results in price increases, for how long do these higher prices last?

This year, the publication named Viña Don Melchor Cabernet Sauvignon Puente Alto 2021 as its winner. Aaron Romano praised the wine for channelling ‘the finesse of the vintage with rich, muscular edges’. He awarded a score of 96 points. According to Spectator, around 18,300 cases were produced, with 5,000 imported into the US.

Having previously only changed hands once, the award has certainly enlivened the market, with most trades taking place at or above its Market Price of £1,166. In today’s market, we would expect trades to take place below Market Price as buyers seek to protect their margins. In this case, however, US buyers have accounted for 79.2% of purchasing, and the US Regional Benchmark currently sits at £1,387. While the award has undoubtedly driven recent trade, the effect has been far milder than in previous years.

Which wines have been most responsive to Wine Spectator’s awards?

Liv-ex trades of Argiano 2018

Argiano 2018, Wine of the Year in 2023, showed a striking uptick in trading activity immediately after receiving the award. Wine Spectator, being an American publication, tends to have greater influence on US buyers than those based in Europe or the UK. With US buyers already accounting for over a third of Tuscan purchasing on the exchange, the award may have coincided well with pre-existing tastes. Moreover, Argiano stock is largely held by UK and European merchants, and sold at lower prices than in the US.

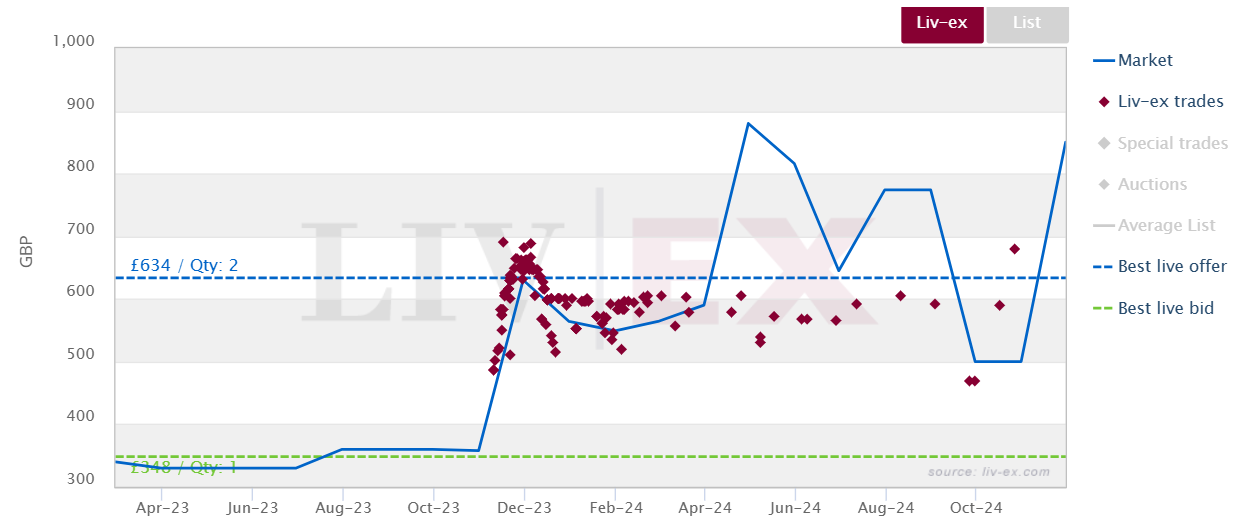

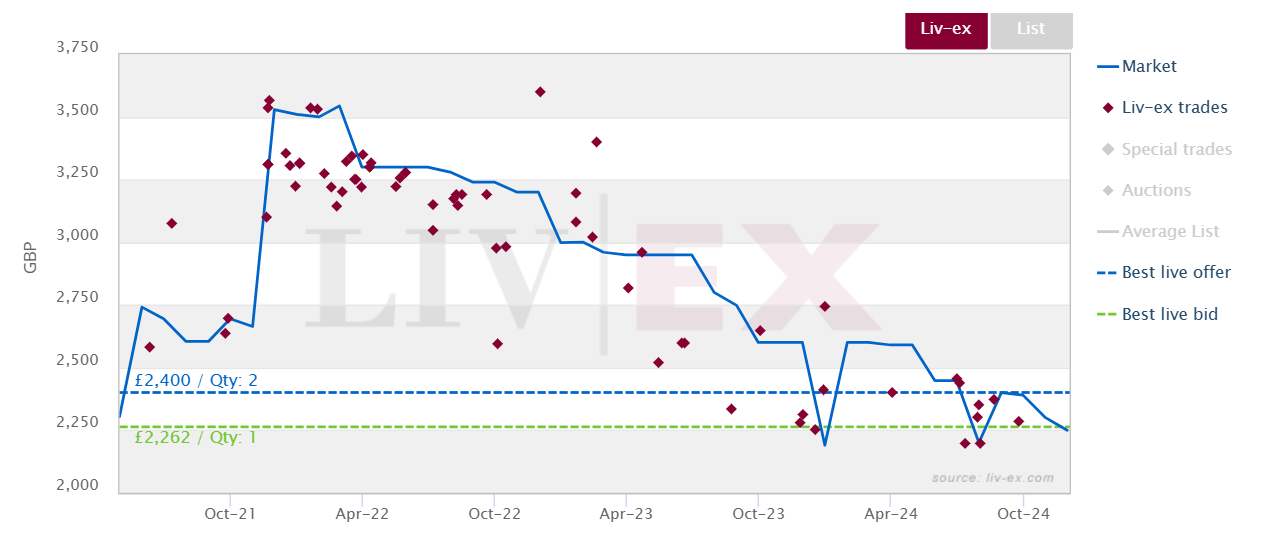

Léoville Barton 2016, Wine Spectator’s wine of the year in 2019, provides another clear example of the award’s effect on trade. On the 15th of November 2019, it traded 37 times, with prices varying between £700 and £1,166 – well above its Market Price at the time. In the days following the award announcement, US buyers accounted for 92.3% of trade, up from their average of 33.9% over the past 10 years.

Liv-ex trades of Léoville-Barton 2016

While the wine may have been cheaper to purchase on the exchange once the initial hype had died down in the early months of 2020, US buyers who purchased at the peak are still able to turn a profit. The US regional benchmark price currently sits at £1,894, twice the value of its current Market Price and 76.7% above its highest ever trade price. By contrast, the US Benchmark for the surrounding 2015 and 2017 vintages sit c.25% above market.

Which wines have been less responsive to Wine Spectator’s awards?

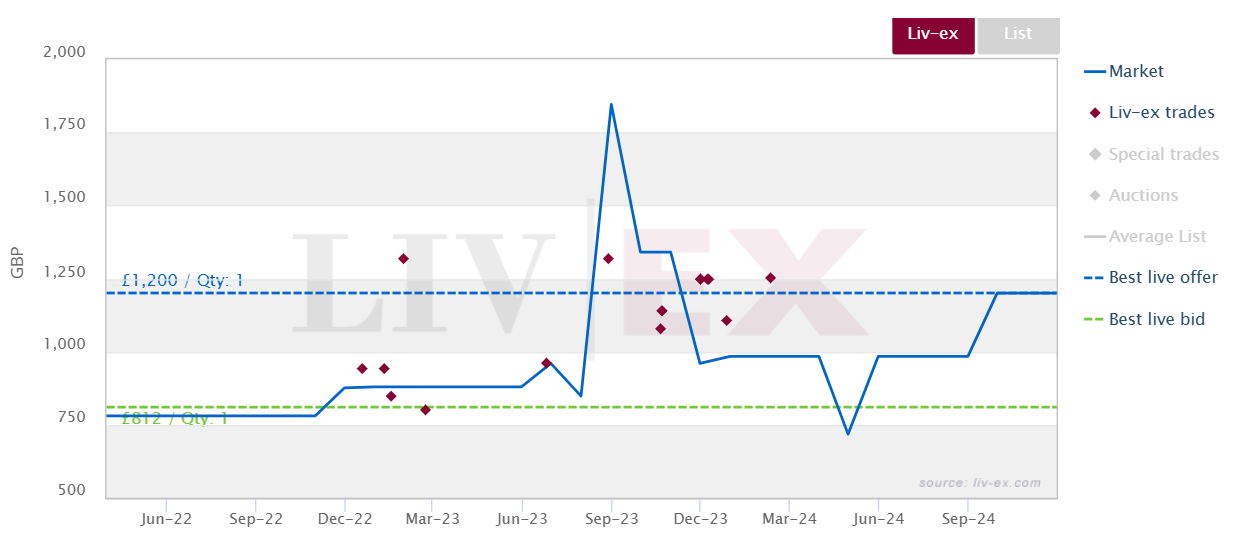

US buyers, more than any other regional segment, are likely to trade in response to a ‘Wine of the Year’ award. This is perhaps why US wines receiving the award have seen a less dramatic uptick in trade. It may be the case that US buyers are able to procure US wines more cheaply domestically, or even directly from the producer. Dominus 2018, the 2021 winner, for example, saw a brief spike in trade and Market Price, but has since returned to pre-announcement levels.

Liv-ex trades of Dominus 2018

The market for California Cabernet Sauvignons is not insignificant in Europe and the UK, but many stockholders will choose to stick with the flagship wines rather than expanding into single vineyard territories. This may explain why Schrader’s Double Diamond 2019, the 2022 winner, saw less trade than Dominus 2018 in the months following the award. Moreover, produced in lower volumes than the aforementioned wines, there is simply less available to trade.

Liv-ex trades of Schrader Double Diamond 2019

The Château Latour index

- The Latour index is navigating a corrective phase, having dropped 20% since its most recent peak in 2022

- The index has shown some early signs of stabilisation, hovering around its 2020 lows

- Restricting volumes on the market appears to currently result in a relatively healthy demand-supply balance

- While not part of En Primeur, one expects future releases of Latour will need to be pitched at the level of Market Prices of other Pauillac First Growths

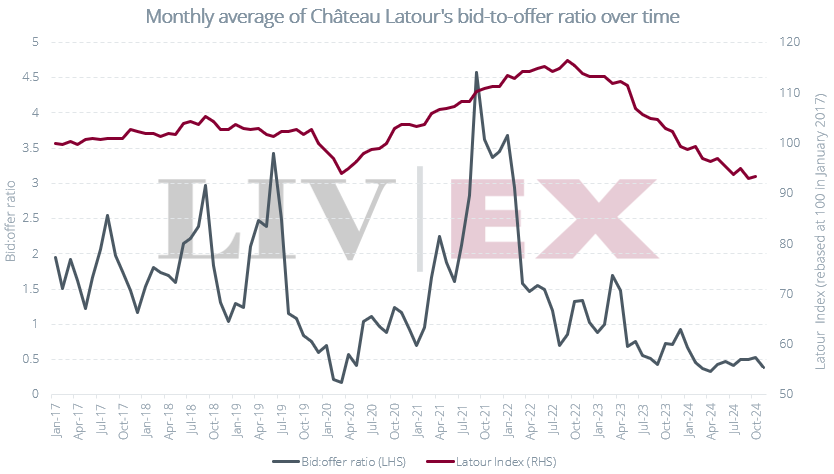

Beginning with the 2012 vintage, Château Latour withdrew from the Bordeaux En Primeur system, choosing instead to release its wines independently once bottled and ready to drink. Since its different release schedules prevent robust comparative analysis with its First Growth peers, we have often excluded it in our reports on the Fine Wine 50. Today, we turn our attention to the price performance of Latour and its bid-to-offer ratio over time.

*The index is comprised of the 10 most recently released vintages, currently including all vintages from 2007 to 2017 (not including the unreleased 2016).

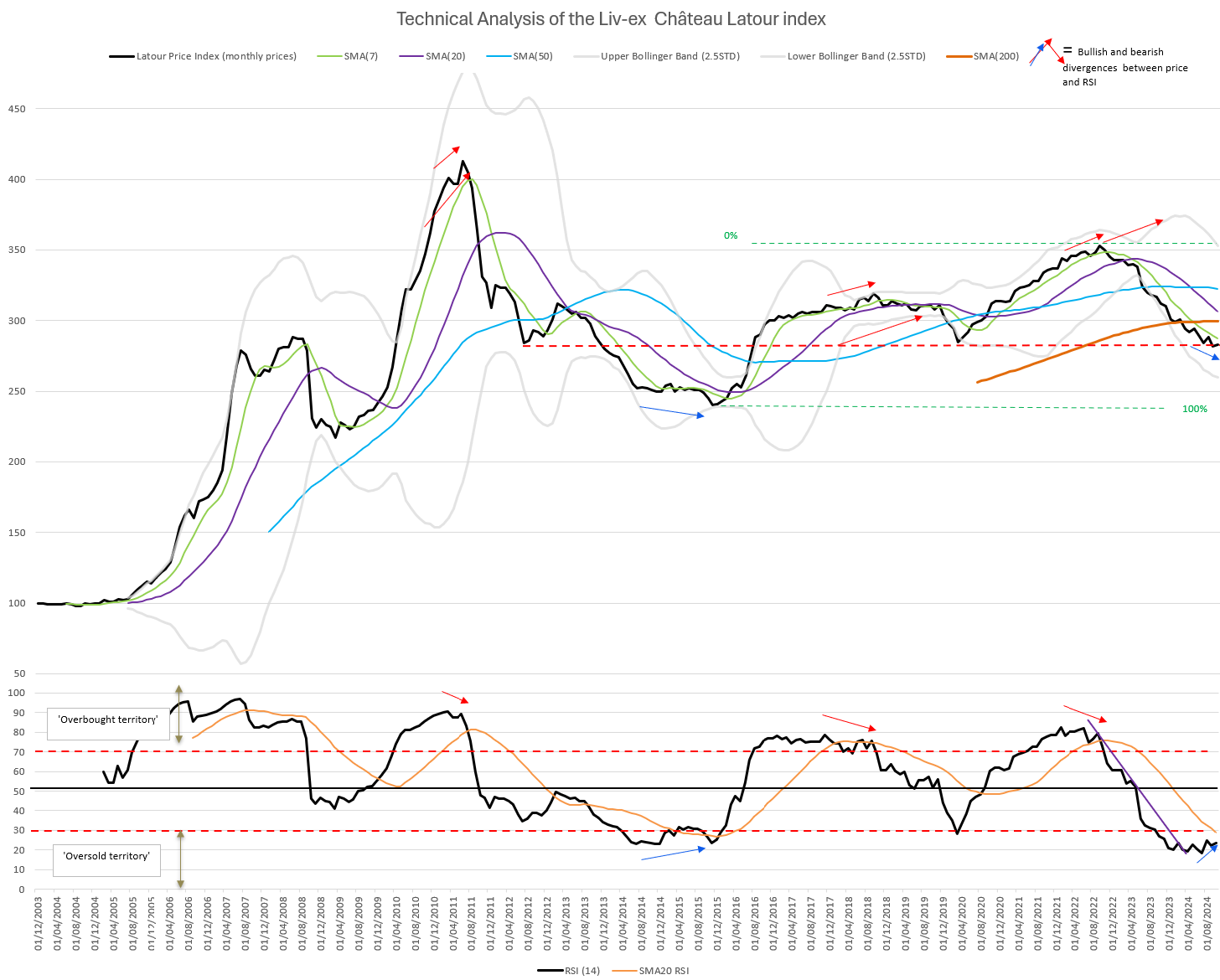

Recently, we published a technical analysis of the Château Lafite Rothschild index. The story here is less severe, though not dissimilar – the Château Latour index is navigating a corrective phase, having now dropped 20% since its most recent peak in 2022.

Like the Lafite index, the Latour index has now crossed below each of its key Simple Moving Averages (7-, 20-, 50- and 200-month). In recent months, however, the Latour index has shown some very early signs of stabilisation, hovering around its 2020 lows (horizontal support zone). By contrast, the Lafite index has decisively broken through this level, its next horizontal support now its 2015 lows.

Latour’s Relative Strength Index (RSI) dipped below 30 – the threshold at which a wine is considered oversold – in October last year, and fell to 18.5 in July. Having recovered to some degree since then, it now sits at 23.7. This improvement in the RSI could be interpreted as increased optimism in the market. Moreover, the RSI’s improvement coupled with downward price movements signals likely bullish divergence. While the index is falling, those downward movements are losing power. As denoted by the blue arrows on the chart, a similar pattern occurred in 2015, prior to the index’s trend reversal.

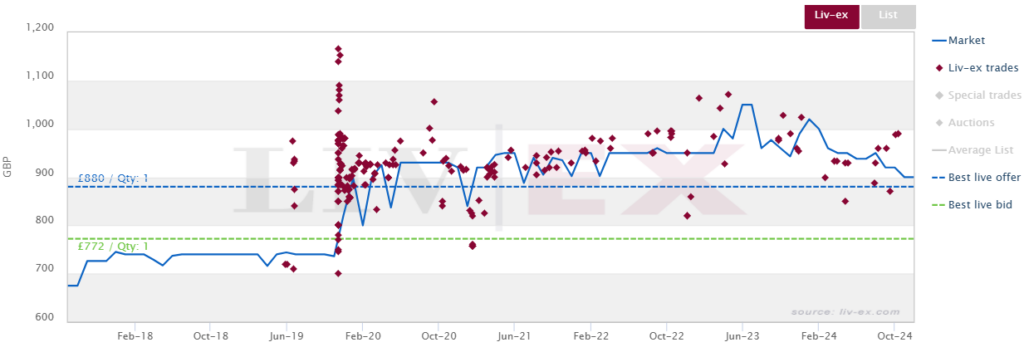

Château Latour’s bid-to-offer ratio

Latour’s bid-to-offer ratio, rising from 0.32 in April to 0.53 in October, provides some evidence of positive market sentiment. Still, the ratio has since fallen to an average of 0.39, indicating a level of uncertainty. Nevertheless, the ratio remains higher than its 2020 low of 0.17.

The relatively high ratio compared to previously is likely the result of Latour’s ability to restrict volumes, especially in a down market, which protects the demand-supply balance and thereby prices. While the Market Prices of the eight most recently released vintages sit below their ex-London release prices, no independently released vintages have fallen below their ex-négociant prices. By contrast, the Market Prices of four recent vintages each of Margaux and Lafite, three of Mouton and eight of Haut-Brion have fallen below this threshold.

Moreover, Latour can hold back its best vintages until market conditions are more favourable. While it may be true that the 2017s are readier to drink than the 2016s, they are also less critically acclaimed. Particularly in Latour’s case, where the 2016 vintage was awarded several 100-point scores, it makes more sense to take a hit on the lower-rated 2017.

That being said, reliance on this distribution method may create problems down the road for Latour. Holding stock is not inexpensive, particularly when production numbers are in excess of 15,000 cases a year. Eventually, the château will need to move stock, and the wine will not be exempt from the market conditions its peer group faces.

In September, Latour rereleased its 2009 vintage 16.0% above its Market Price. Needless to say, despite the wine’s critical acclaim, merchants were wary to take on stock. The most recent vintage released, the 2017, has been met with similar hesitance. Its Market Price already sits 14.6% below its ex-London release price of £4,800 per 12×75. Its price has fallen a similar distance to that of Mouton, but at a faster rate. By contrast, Lafite 2017’s Market Price has been considerably more stable, currently sitting just 3.5% its release price. In this year’s market, Latour’s lower release volumes have perhaps not had the desired effects.

What this demonstrates is that while Latour has been able to watch on from the sidelines as recent vintages of the other First Growths have fallen below their international, ex-négociant, and in some cases ex-château release prices, future releases of Latour need to be priced according to current Market Prices – not the release prices – of its peers. This, one might argue, largely defeats the point of delayed release.

Final thought – tariffs and the US market

Across the board, industry professionals believe that higher tariffs on imported wine will, overall, have a negative impact on the American wine industry. Rather than successfully encouraging consumption of US wine, tariffs will likely result in higher prices for all wine in the US, including that which is domestically produced. While the US wine industry prepares for this eventuality, there will likely be knock on effects felt in the UK and Europe in the months and years ahead.

For some US merchants, preparing for tariffs means getting stock onto US soil before they are imposed. A second set of merchants, with capital still expensive and the hope that lobbying may sway policymakers away from tariffs on wine, are instead choosing to sit tight. Even with Trump back in office come January, there may yet be a while to wait before any decisions are made. Other merchants – those less optimistic about the future of the US wine distribution industry – are scaling back, focusing on keeping balance sheets in good health as they prepare to take financial hits.

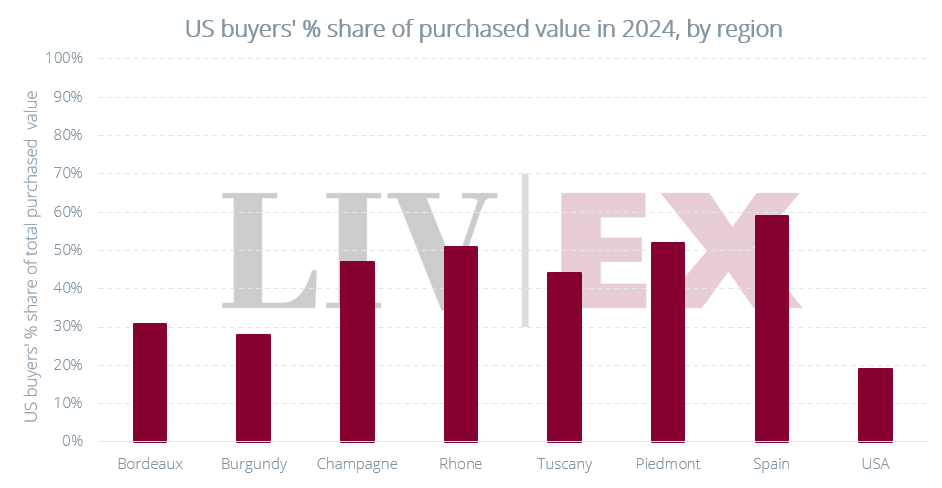

The role of US buyers on the secondary market

US buyers have accounted for 35.0% of all purchasing (by value) on the market this year. This means that for the first time the US is responsible for the greatest share of trade of any geography – impressive, given that they make up just 10% of market participants. US buying habits are not dissimilar to the broader market, mostly concentrated in Bordeaux, followed by Burgundy, Champagne and Tuscany. Nevertheless, they constitute a large percentage of buying of smaller, often overlooked regions – 51.6% of the Rhône, 53.1% of Piedmont and 58.5% of Spain. The presence of US buyers has allowed the secondary market for nicher labels to flourish.

Amongst US buyers, Dom Pérignon 2013 is the top-traded wine of the year by value, followed by Lafite 2010, Tignanello 2021 and Vega Sicilia Unico 2013. Vega Sicilia, which recently won the top spot in the Liv-ex Power 100, has found immense popularity amongst US buyers this year. Accounting for 64.5% of Vega Sicilia purchasing, US buyers have no doubt been instrumental in the producer’s success.

In general, wine prices are markedly higher in the US than in the UK and Europe, which allows more room for US buyers to make margins. As we have previously reported, in a down market, trade prices tend to occur at a higher discount to Market Price before list prices adjust to reality. On average, trades have taken place this year at a 5.7% discount to Market Price. However, the discount sits at 4.6% for purchases by US buyers. Not only do they account for a large proportion of buying, to an extent, they have aided in propping prices up.

How did the 2020 tariffs affect buying?

In 2019, French wine accounted for 76.5% of US buying. In 2020, after the imposition of a 25% tariff on French wine, this figure fell to 57.0%. While the nominal decrease in French wine imports was not insignificant, the opportunity cost was likely much higher. US buyers turned their attention instead to Italy, increasing their spending on Tuscan wines by over a third.

If, this time around, tariffs are imposed broadly, US buyers will not have the option of turning to other European regions. Possibly, as presumably hoped, this could encourage the buying of US wines. However, unlike the manufacturing of most consumer goods, premium European wine, tied above all to its sense of place, cannot be easily swapped out for a domestic alternative. While we can compare the best of Bordeaux with the best of California, they are undoubtedly different in character. With tastes changing in the US, there is concern that higher prices may push potential consumers towards spirits or other goods.

Still, there is some hope that broader conditions in the US economy could offset the potential losses of tariffs. Should the Dollar remain strong relative to the Euro and Pound Sterling, US merchants will still stand to turn a profit buying abroad. Though expected FED interest rates cut will likely mitigate Dollar strength, it will also free up US capital to expand stockholdings. With the American public recovering from a period of high inflation, it is unlikely Trump will make the unpopular decision to impose tariffs high enough to kick start another inflationary episode. Though we should not underestimate the importance of US buyers in the secondary market, all is not lost.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.