The 2024 Liv-ex Power 100 – How low can we go?

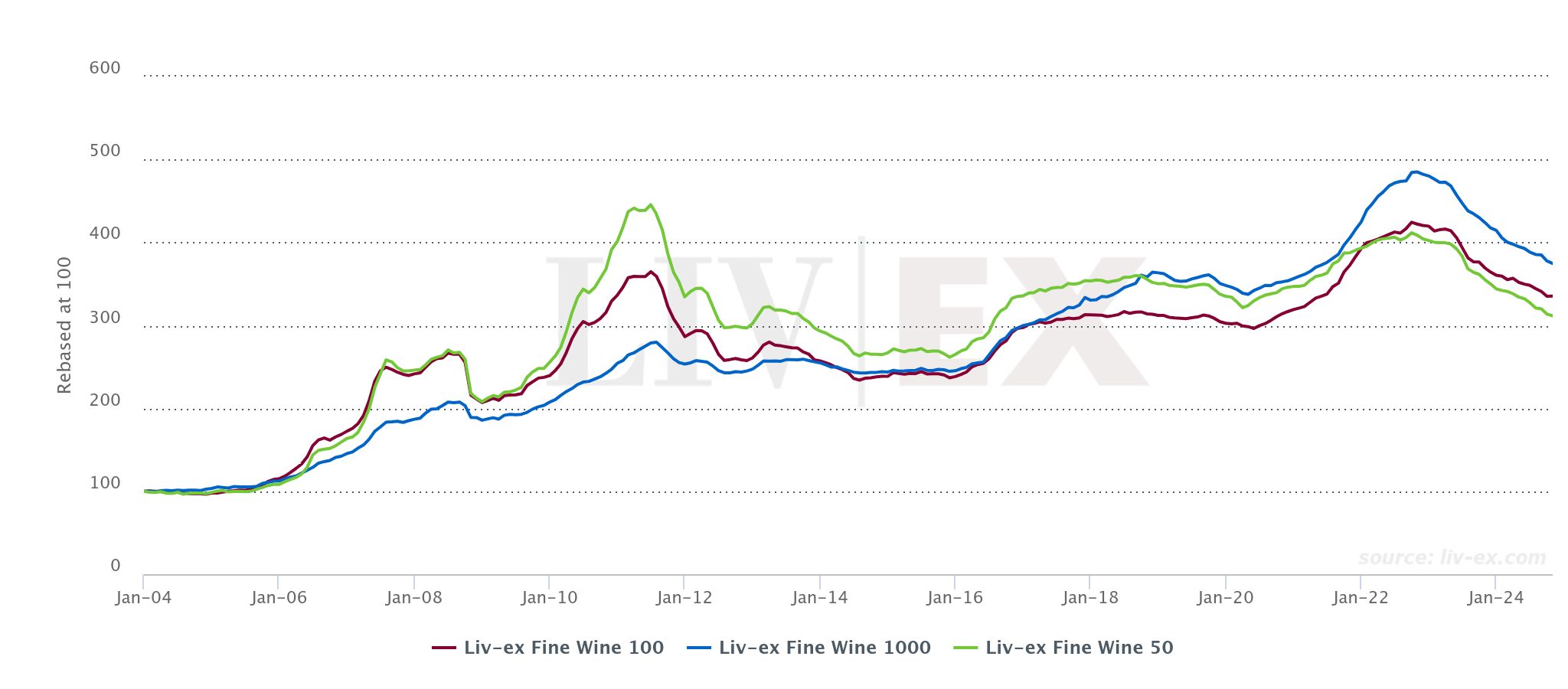

- The 2024 Power 100 is set against the continued market downturn, with all major Liv-ex indices down at least 9.0% year-on-year

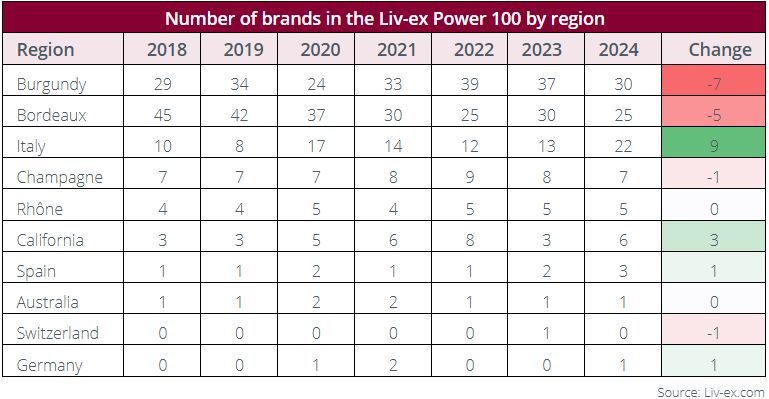

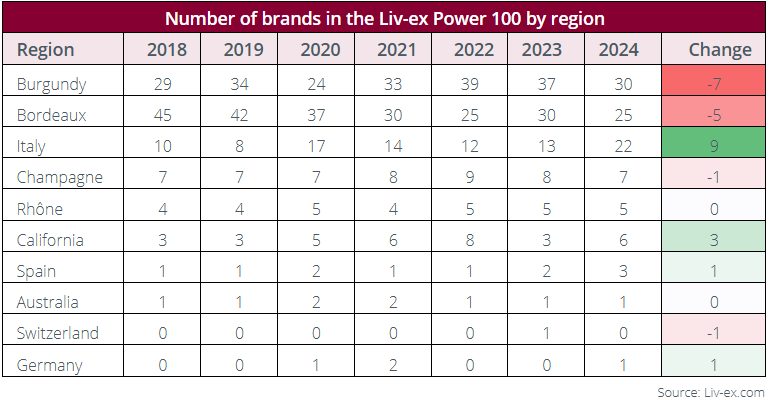

- Italy gains ground as risk aversion continues to hold firm in the market

- 2024 sees the Power 100 topped by a Spanish brand for the first time

- Household Bordeaux brands fall out of the Power 100, with prices for recent vintages crashing below their release prices

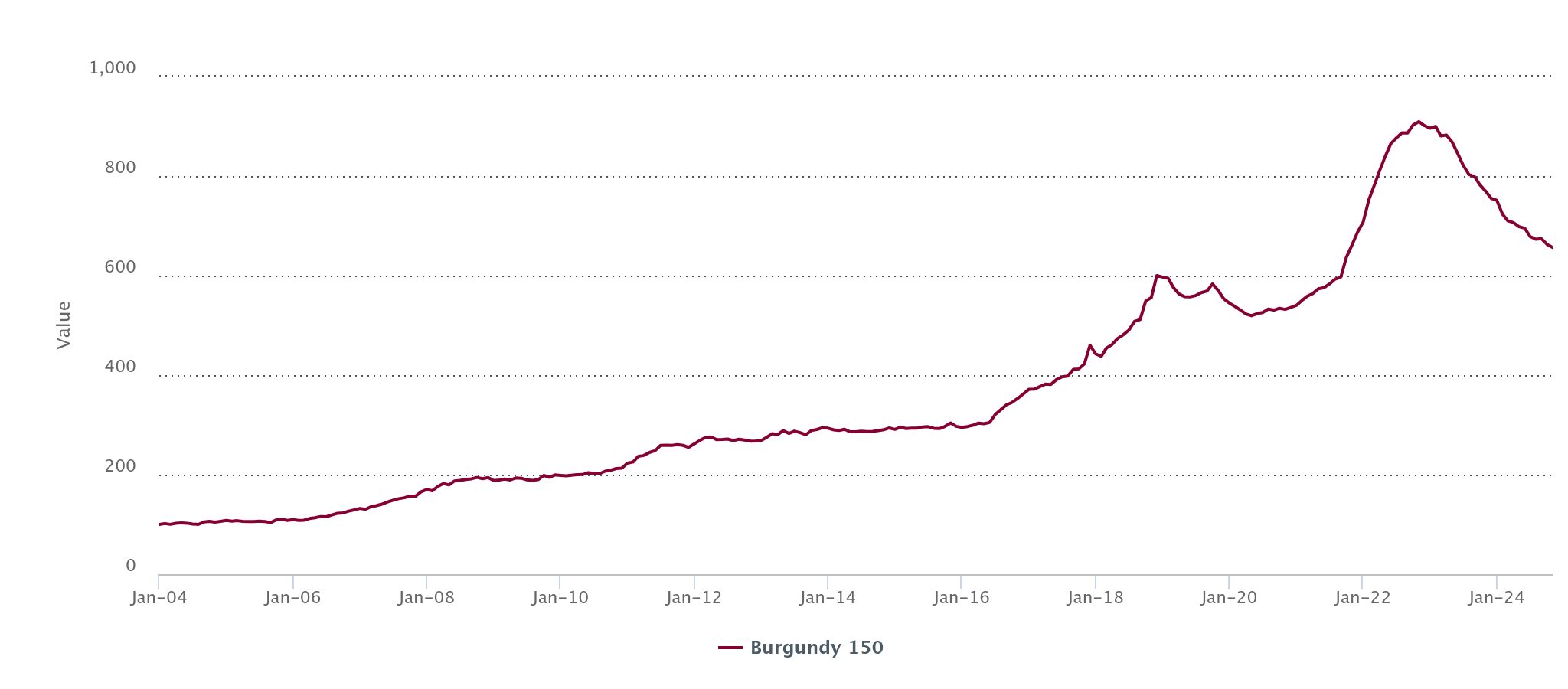

- With the Burgundy 150 falling 14.7% over the past year, many of the region’s blue-chip brands slip down the rankings

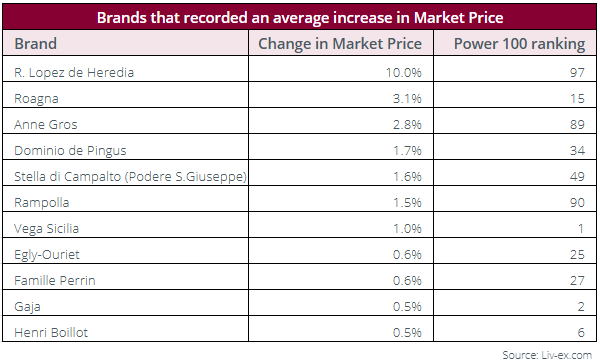

- Only 11 brands in the Power 100 recorded a positive price performance in the past 12 months

Introduction

The Power 100 is a ranking of fine wine brands that reflects trade on the global marketplace over 12 months. It takes into account a range of criteria such as price performance, average price and value and volume traded on Liv-ex.

In a gruelling year for the fine wine market, it is tempting to consider the Power 100 an attempt to hide a pack of wolves in sheep’s clothing. This would be a mistake. Yes, the might of many estates has been eroded since the downturn began two years ago, but as a list of the most reliable, consistent brands under current market conditions, an entry on the Power 100 is arguably more valuable than ever.

Before diving into the list, some market context. All major Liv-ex indices are down at least 9% year-on-year. The industry standard Liv-ex 100 is down 9.2%, the Liv-ex 1000 (the broadest measure of the market) is down 9.6%, and the Liv-ex Fine Wine 50, which tracks the performance of the 10 most recent physical vintages of the Left Bank First Growths (ie. the historical powerhouses) is down 12.5%. Of the Liv-ex 1000 sub-indices, the Italy 100 has weathered the storm better than the rest (down 4.1%).

In short, the market correction has continued, pretty much unabated. The two questions on everyone’s lips have been ‘Are we reaching the bottom?’ and ‘How much further can the market fall?’ The answers, broadly speaking, have been ‘No’ and ‘Until prices reach a point to clear out an excess of stock’. September saw the downturn accelerate. Perhaps enough stockholders were beginning to feel sufficient pressure to drop their prices in meaningful ways, rather than the steady death by a thousand cuts that had characterised the preceding months.

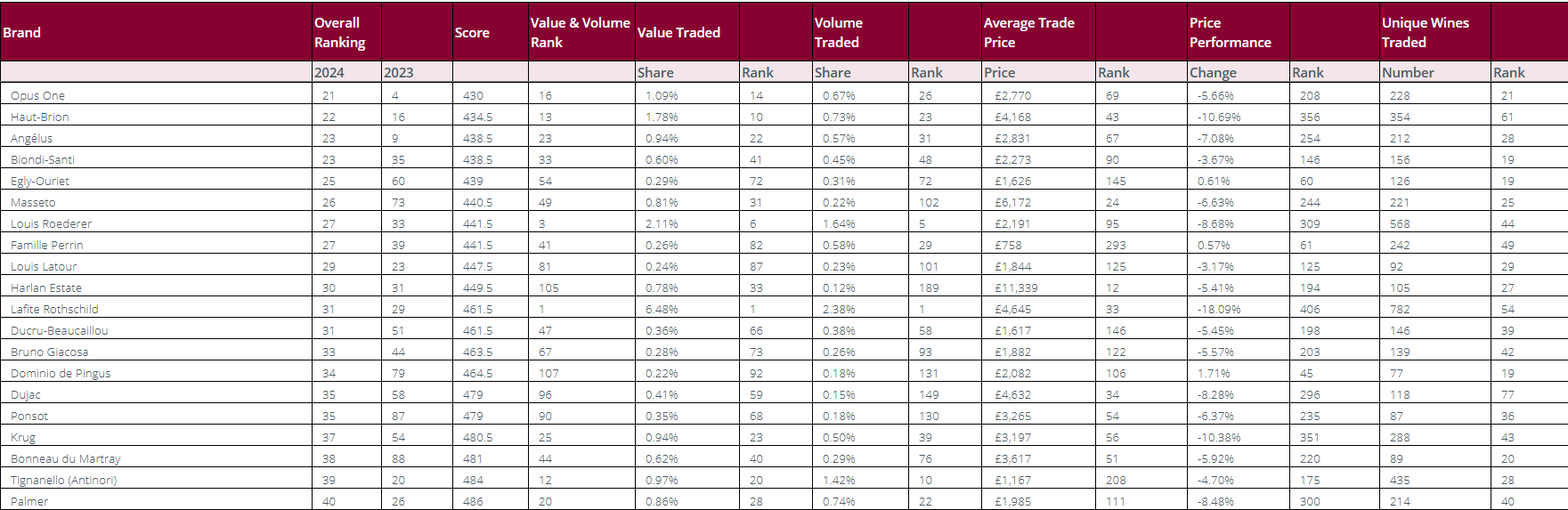

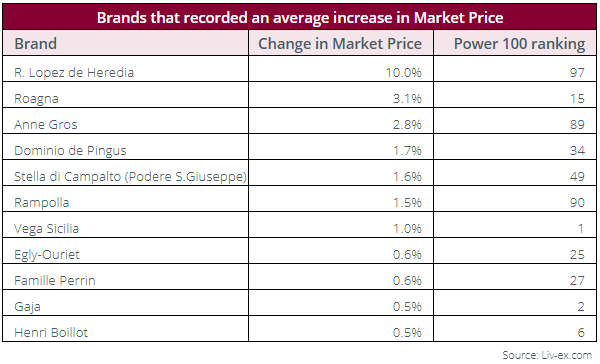

In that context, positive price performance – or even just an ability to limit one’s losses – has been hard to come by. In 2022, just 27 of the 422 brands that qualified for consideration in the Power 100 registered a negative price performance. This rose in 2023 to 216 (52.3%) of the 413 brands that made the cut. This year 343 (83.7%) of the 410 brands that qualified fell in value. Of the final 2024 Power 100, only 11 brands recorded a rise in their Market Price over the past 12 months.

Beyond price pressure, the 2024 fine wine market has been characterised by two trends. First, activity has remained high – the number of wines traded has stayed consistent. We see this in the Power 100 – the count of trades for the 2024 list is 7.9% higher than for the 2023 list. Secondly, buyers have tended to be reluctant to take on stock that they can’t shift quickly, resulting in volumes traded falling 6.5%.

Therefore, it is not surprising that what we tend to see at the very top of the 2024 Power 100 list is an exaggerated view of last year, it being heavily skewed towards brands with higher volumes and, generally, a wide range of labels.

The dataset considered covers the year from 1st October 2023 to 30th September 2024. The rankings are then calculated based on several weighted criteria including price performance, the number of a brand’s wines traded and the cumulative value and volume of that trade over the selected period. You can read the full methodology at the end of the report.

Regional Breakdown

Italy closes the gap to Burgundy and Bordeaux

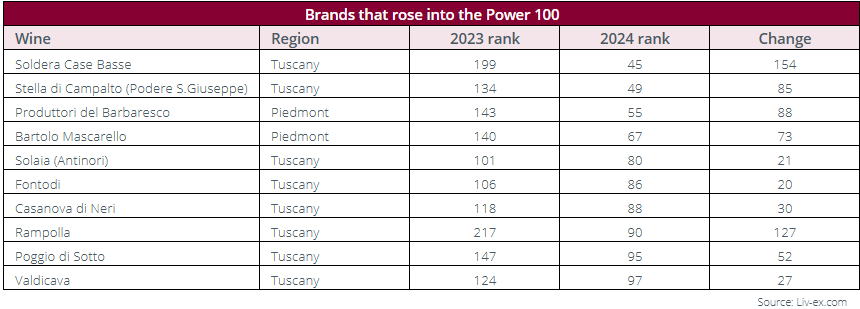

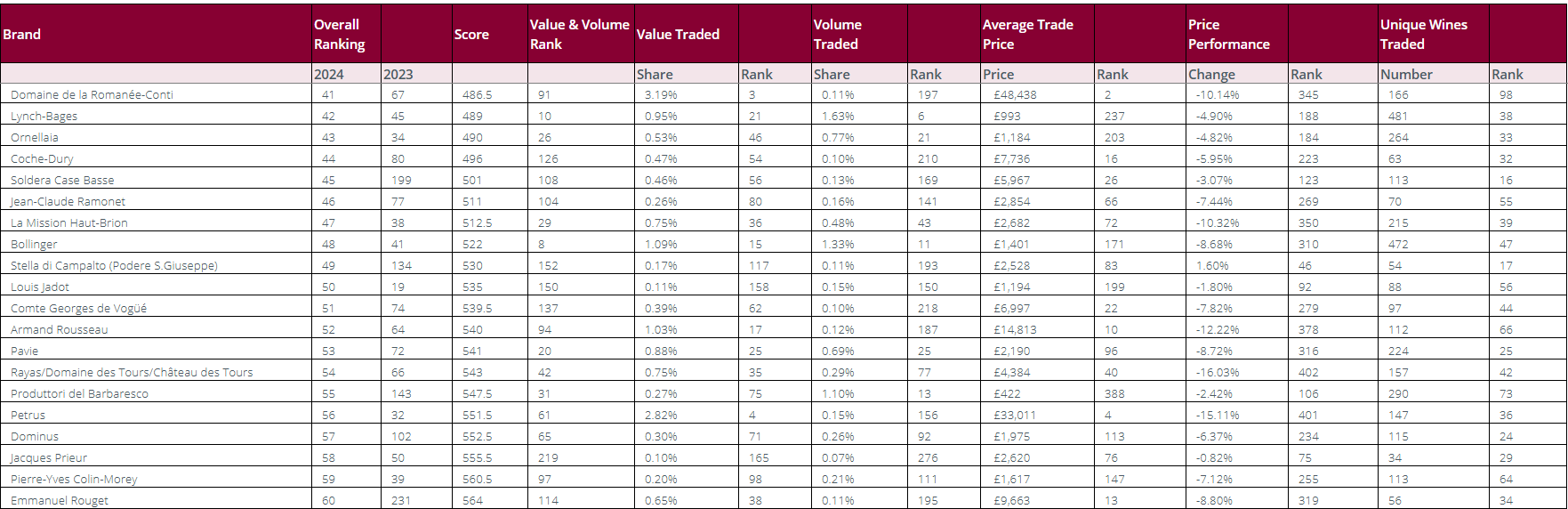

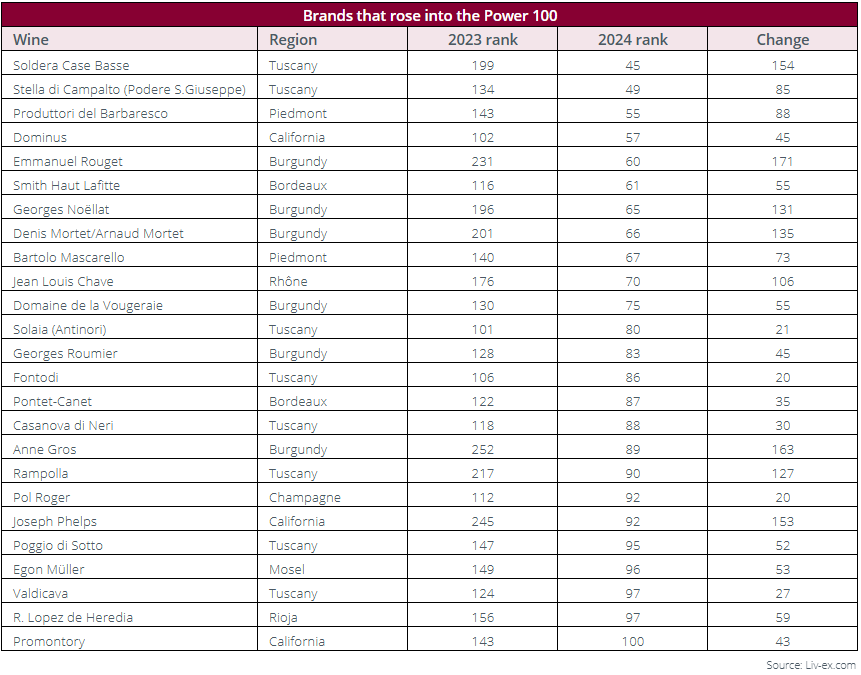

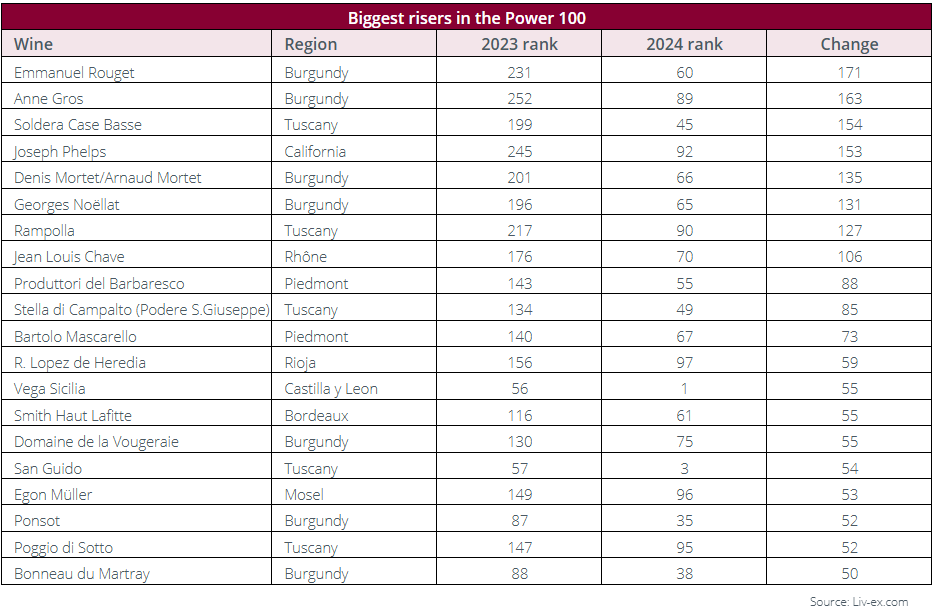

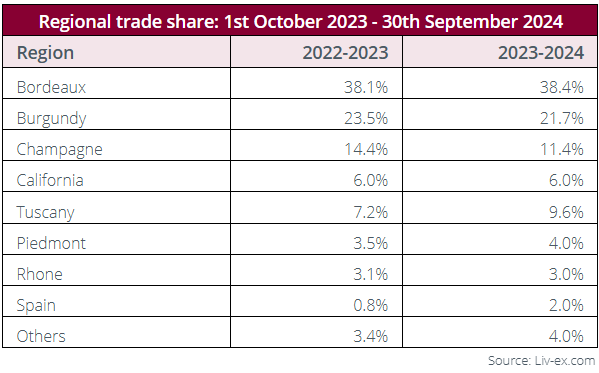

Italy stands tall as having made the strongest gains in the 2024 Power 100, filling 22 spots, nine more than last year, and is snapping at the heels of Burgundy and Bordeaux. While Tuscany, and in particular Brunello (or declassified Brunello in the case of Soldera Case Basse), has made the greatest gains, a deeper look reveals a far from homogenous set of Italian producers that have entered the list this year. On the one hand there are high value, relatively illiquid brands with the likes of Soldera Case Basse which has risen 154 spots on last year. On the other hand there is Produttori del Barbaresco, which is the 13th top-traded brand by volume in this year’s list, but whose average trade price is the 23rd cheapest.

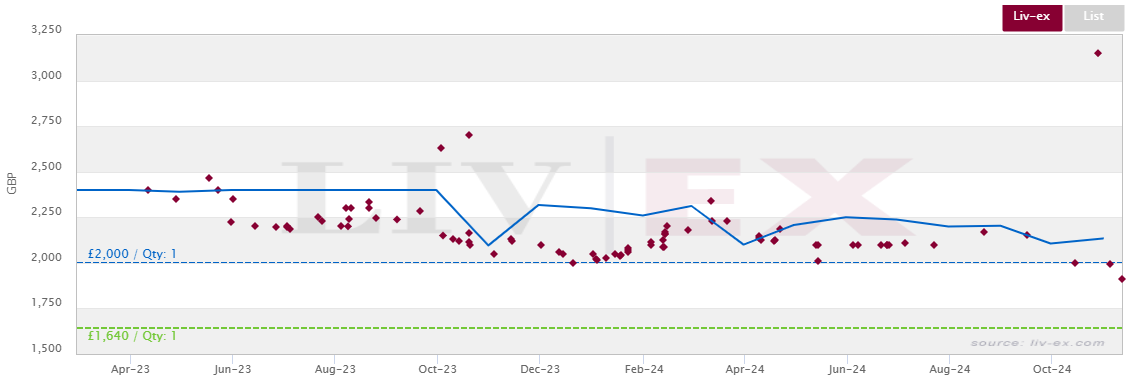

The top two Italian brands, Gaja and San Guido, exemplify this variety. San Guido has climbed 54 spots to reach third this year. Produced in decent volumes, with relatively consistent release prices, and, in the scheme of things, affordable trade prices, it represents a safe bet in a down market. It is a wine that can be bought in high volumes and, crucially, drunk without too much concern as to whether one should wait for tomorrow. Sassicaia 2020 was the third most-traded wine by value and eighth most traded by volume during the period considered for the Power 100.

Liv-ex trades of Sassicaia 2020

While the wider market has fallen over the past two years, Gaja has climbed the rankings. 38th in the 2022 list, seventh in 2023, and now second. The Gaja brand, carefully and consistently built up over decades, is well known and trusted. This is reflected in the breadth of Gaja wines that trade. 70 different vintages of 13 different brands have changed hands over the past 12 months. As an added bonus, it is one of the 11 brands in the Power 100 whose average price has not fallen over the past year.

Spain – no longer under the radar?

Vega-Sicilia tops the Power 100 list. This is the first time a Spanish wine has done so. While there are other wines in the stable, this is overwhelmingly a story about Unico (and to some degree Unico Especial). Spearheaded by US demand, Unico has been one of 2024’s few success stories. The facts speak for themselves. Compared to 2023, Vega-Sicilia Unico’s trade count is up 193%, its trade volumes are up 324%, and its trade value is up 310%. With considerable heritage – it was first produced in 1915 – and still representing good value, it is unlikely to be a flash in the pan.

There are just two other Spanish entrants in this year’s list – fellow Ribera del Duero (by way of Denmark) Dominio de Pingus and Rioja’s R. Lopez de Heredia. The latter is a new entrant. Beyond the top 100, there is one fewer Spanish brand in the long list than last year. What we can say, therefore, is that there are plenty of Spanish discoveries for the fine wine market to make. These may well come from Ribera del Duero and Rioja, but not necessarily. With producers on the up in regions such as Sierra de Gredos and Priorat, Spain is a country to be keeping a close eye on.

Bordeaux – survival of the fittest

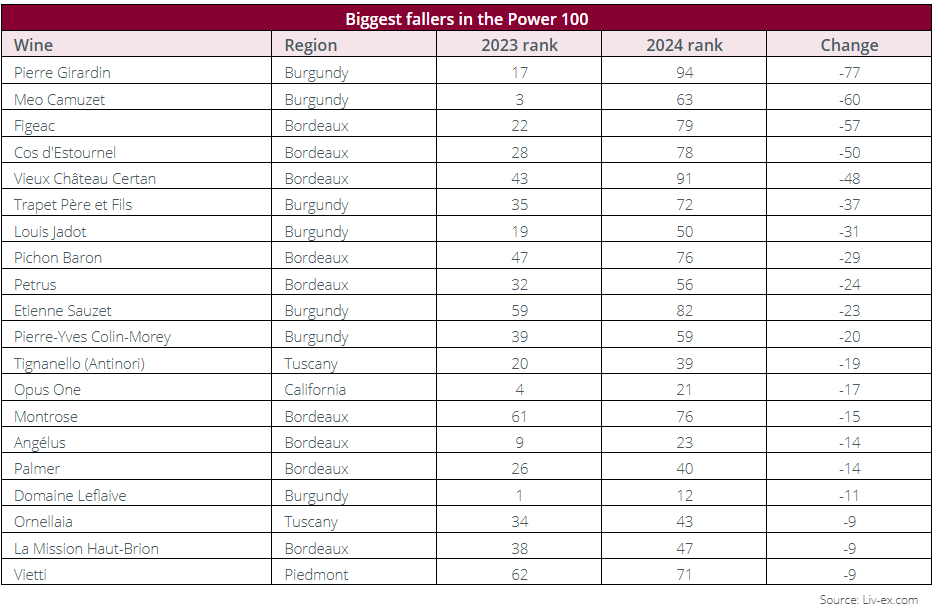

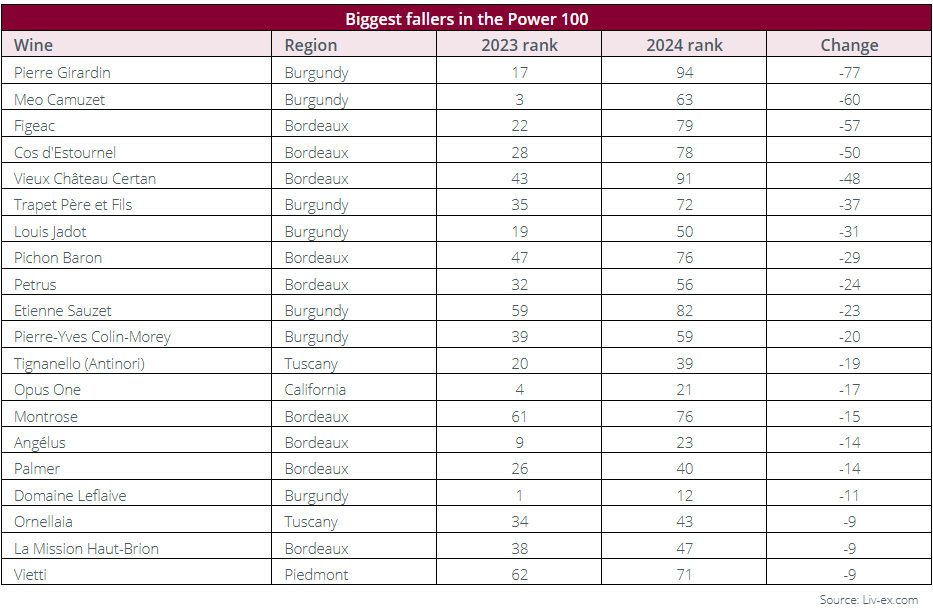

In last year’s Power 100, Bordeaux emerged as the beneficiary of Burgundy’s travails since the turn of the market in late 2022. As we wrote at the time: ‘[Bordeaux is] the least risky market, the best understood; collectors know what to expect from these wines, which is quality at a certain price, and relative liquidity’. 12 months later, not all the same can be said. It certainly remains the best, and most widely, understood – the mechanics are unchanged and liquidity is still its strength. However, in the current market, it is not necessarily the safest bet, in particular for recent vintages which have crashed through release prices pretty much across the board. Lafite is the prime example of Bordeaux’s dilemma. The number one brand in terms of traded value and volumes, its prices have, on average, fallen 18.1%.

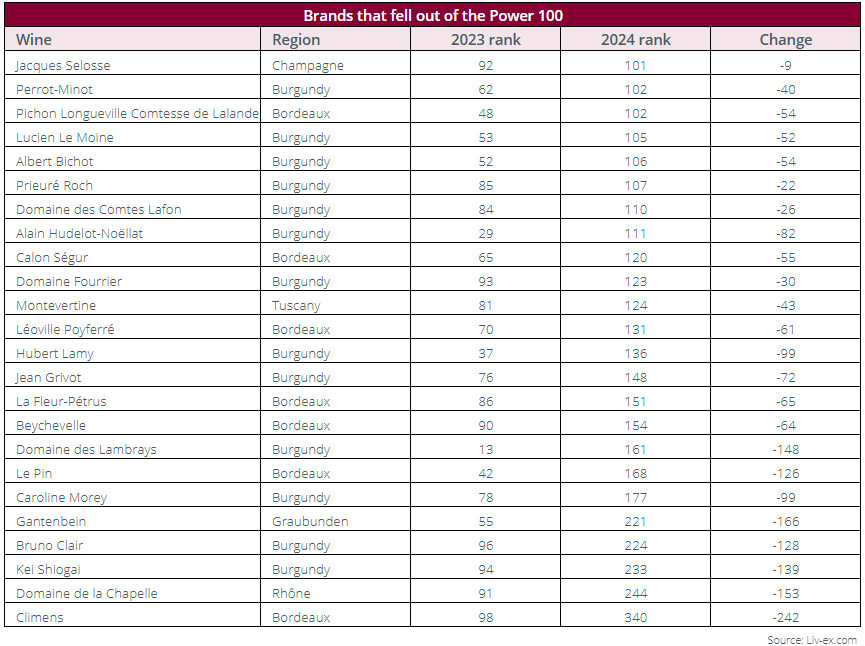

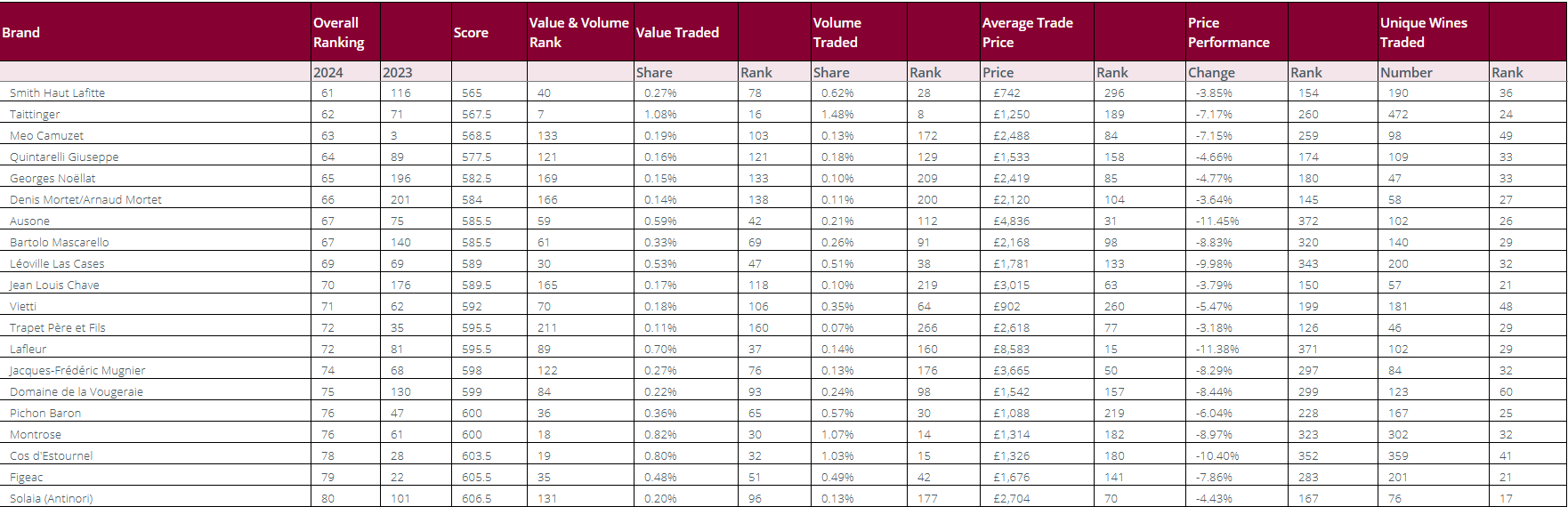

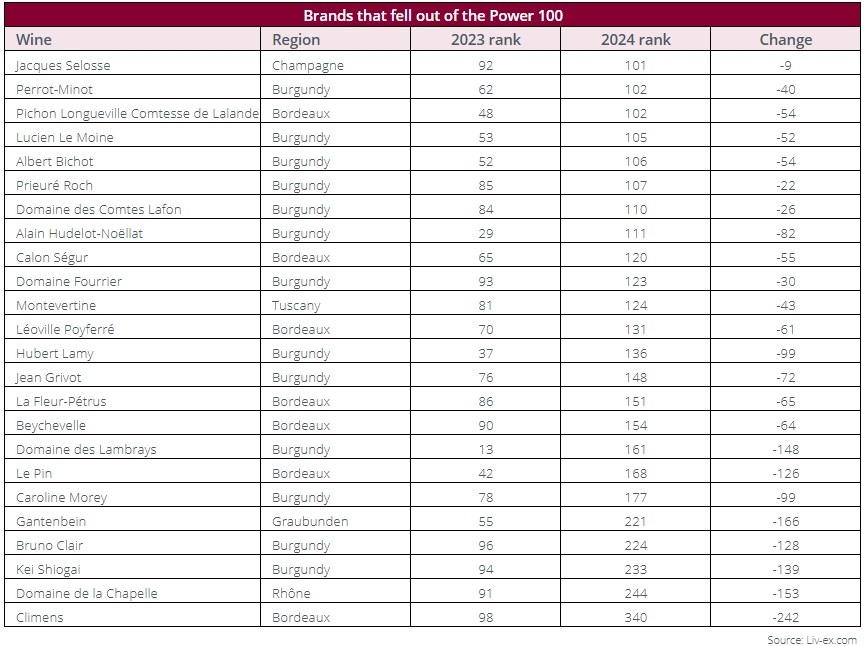

There are five fewer Bordeaux brands in the Power 100 compared to last year, with the likes of Le Pin, Pichon Longueville Comtesse de Lalande, and Léoville Poyferré dropping out.

Burgundy – victim of its own success

Given high volumes and accessible prices have characterised 2024’s biggest risers, it’s not surprising that Burgundy has fared badly this year. This is reflected in the Burgundy 150 index having fallen 14.7% over the past year, and 27.8% since the peak in October 2022. We also see the impact in this year’s Power 100, with seven fewer Burgundy brands in the list than last year. Nevertheless, Burgundy continues to be the best-represented region in the Power 100.

Variety of terroir is, for many collectors, the hook that inspired a passion for Burgundy. It is also the aspect of Burgundian wine that has prevented the region from faring any worse in this year’s Power 100. Burgundy brands take the top five spots in terms of number of unique wines traded. The Power 100’s methodology groups domaine, maison and négociant labels together. This of course increases the pool of wines and tips the scales in favour of the larger brands. It is thus no surprise that Drouhin, Bouchard Pere et Fils, and Louis Latour sit alongside and ahead of the very bluest of blue-chip producers near the top of the table.

Champagne

The Champagne 50 has fallen 10.6% over the past year. Its share of trade is also down from 14.4% last year to 11.4% this year.

Jacques Selosse has dropped out of the Power 100, with Egly-Ouriet remaining the only Grower Champagne in the list. This is not surprising. The Grandes Marques represent volumes, consistency (in both taste and trade), and accessible prices. Crucially, the Grandes Marques are regularly opened and drunk. They are, in short, reliable and liquid.

California

There are three more Californian brands in the Power 100 this year, courtesy of Dominus, Joseph Phelps and Promontory rising up the ranks. With just 12 vintages under its belt, but benefitting from the Harlan heritage, Promontory shows that there are new brands that can thrive under current market conditions. Its average trade price ranks 23rd in the Power 100.

Joseph Phelps is one of the biggest risers this year, up 153 spots. It is not hard to see why. It has enjoyed price stability (its average Market Price is flat over the past 12 months), increased trading volumes (+84.2%), and increased trade value (+151.2%).

Who were the underperformers?

Given the characteristics of this year’s top performers, it comes as no shock that Burgundy accounts for the greatest number of brands to have fallen down the rankings this year. Moreover, we note that many of the Burgundian brands that rose the fastest have now crashed the hardest. The likes of Kei Shiogai and Domaine des Comtes Lafon have dropped out of the Power 100 altogether.

What is notable is the struggle of many of Bordeaux’s household names. Figeac, Cos d’Estournel, Vieux Château Certain, Palmer…the list goes on. However, it is undeniable that Bordeaux has all the fundamentals to be struggling less. It has the volumes, it has an enviable number of established brands, it has the distribution, and it should have the prices to sustain it. That Sassicaia – Tuscany’s mirror image of the Bordeaux model – is thriving is further evidence that something is wrong. Beyond a subdued Chinese market, that something is unquestionably release pricing. This year’s En Primeur campaign was, to put it mildly, hard going. With cellars full of back vintage Bordeaux and lacklustre demand, there is a significant stock overhang. A stock clear out is currently underway. While collectors have not profited from buying En Primeur for a decade, we are now seeing merchant and négociant margins disappear as the market searches for the clearance price.

Conclusion

As confidence has dissipated from the market, participants have gravitated towards brands that represent the least risky bets. While last year it looked like that meant Bordeaux, this year it means brands which share many stereotypically Bordelais traits – but not its terroir – that have risen to the top. Volume, liquidity, heritage brand, and prices that invite the uncorking of bottles are their calling cards. With the market still looking for a turning point, it is unlikely participants will be changing tack just yet.

Power 100 methodology

To calculate the rankings, we took a list of all wines that traded on Liv-ex in the last year (from 1st October 2023 to 30th September 2024) and grouped these by brand. As is now standard, Burgundy labels with both maisons and domaines were combined as one.

We then identified brands that had traded at least three wines or vintages and had a total trade value of at least £10,000.

Brands were ranked using four criteria: year-on-year price performance (based on the Market Price for a case of wine on 1st October 2023 with its Market Price on 30th September 2024); trading performance on Liv-ex (by value and volume); number of wines and vintages traded; and average price of the wines in a brand. The individual rankings were combined with a weighting of 1 for each criterion, except trading performance, which had a weighting of 1.5 (because it combined two criteria).

All Tables and Charts

2024 Power 100 – 1 to 20

2024 Power 100 – 21 to 40

2024 Power 100 – 41 to 60

2024 Power 100 – 61to 80

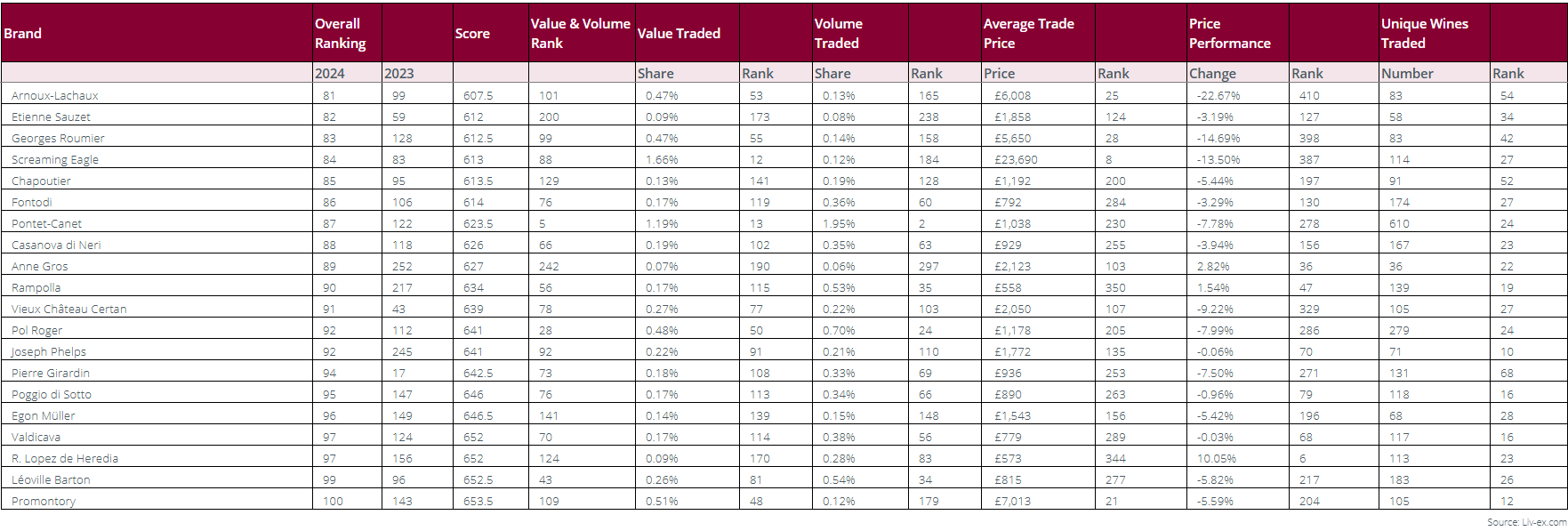

2024 Power 100 – 81to 100

Brands that recorded an average Market Price increase

Brands that fell out of the Power 100

Brands that rose into the Power 100

Biggest fallers in the Power 100

Biggest risers in the Power 100

Regional trade share

Breakdown of Power 100 by region