November Market Report

Introduction – Market Activity Increases

After a downward acceleration in September, October saw a degree of stability return to the major Liv-ex indices.

The Liv-ex Fine Wine 100, the industry benchmark, recorded a modest rise (0.1%). This is the first time since March that the Liv-Ex 100 hasn’t fallen. Year-to-date the index is down 7.0%.

The wider market, represented by the Liv-ex Fine Wine 1000, fell 0.8%. The California 50 and Rest of the World 60 were the worst performing sub-indices, falling 2.5% and 2.8% respectively.

The Liv-ex Fine Wine 50, which tracks the 10 most recent physical vintages of the Left Bank First Growths, fell 0.7%. Latour fared best, with five vintages rising, three falling, and two flat.

While prices on the whole remain under pressure, October saw a notable increase in market participation with the highest number of unique wines (LWIN11s) traded on the exchange in a single month since January 2022 – a 20.5% increase on September. Traded litre volume in October was up 31.0% on September, and traded value by 24.4%. Total exposure also reached record levels (£150m).

Finding Value in Chablis

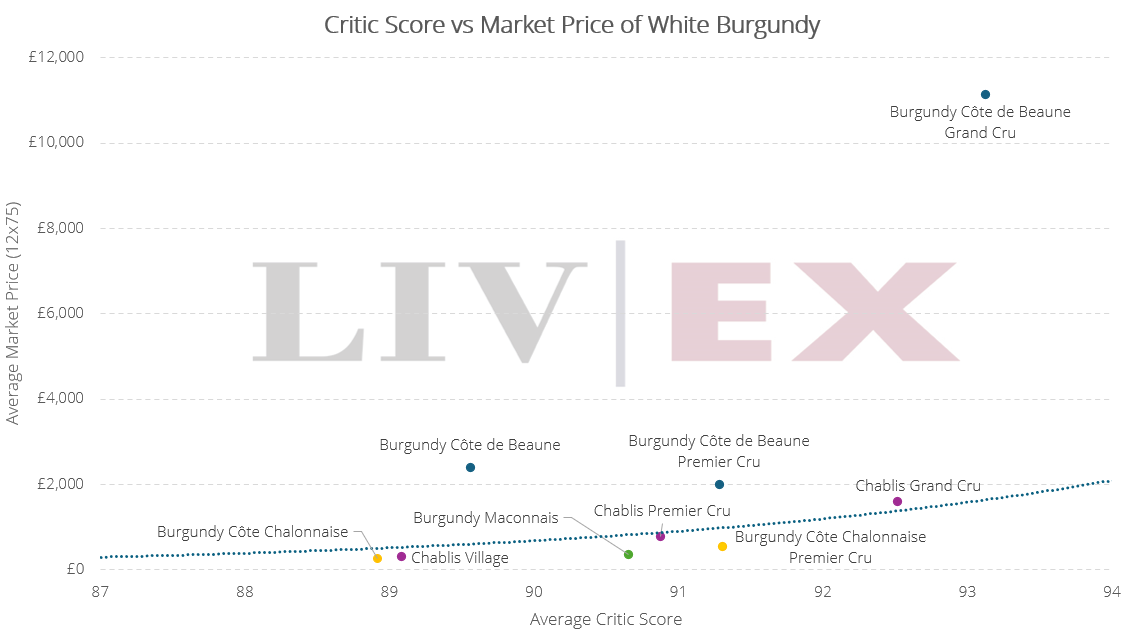

Chablis’ producers contend with a marginal climate to make some of Burgundy’s longest-lived white wines. Nevertheless, despite this longevity and widespread recognition of the Chablis brand among consumers, its prices tend to sit well below those of other Burgundy sub-regions.

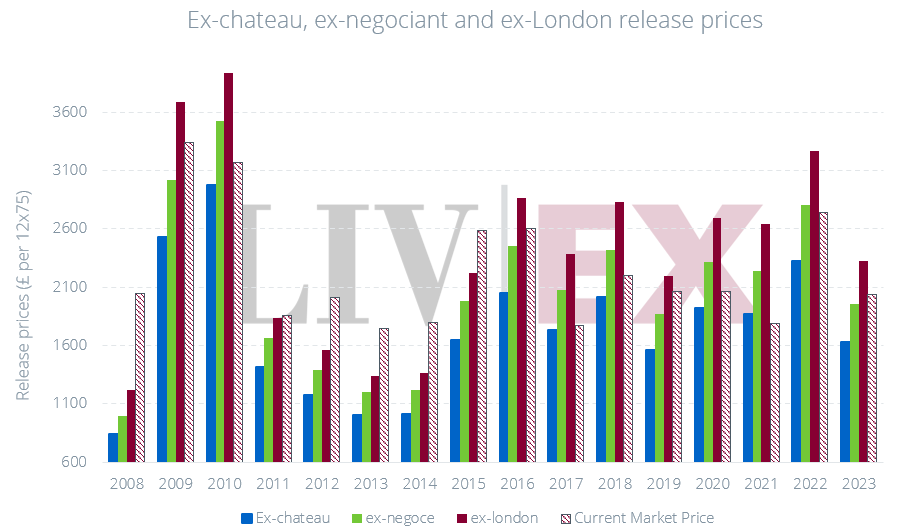

Across each tier, the price of Chablis is significantly below Côte de Beaune whites. Chablis Grand Cru might be the most interesting category for collectors. Its wines are, on average, rated higher than 66% of Burgundy white wines (92.5), yet cost less than half of them. Only the whites of the Côte de Beaune Grand Cru category outperform Chablis Grand Cru in terms of average score (93.1), their wines rating higher than 73% of Burgundy whites. However, this quality comes at a considerable premium: at an average price of £11,146 per 12×75, Côte de Beaune Grand Cru whites are, on average, seven times more expensive than Chablis Grand Cru.

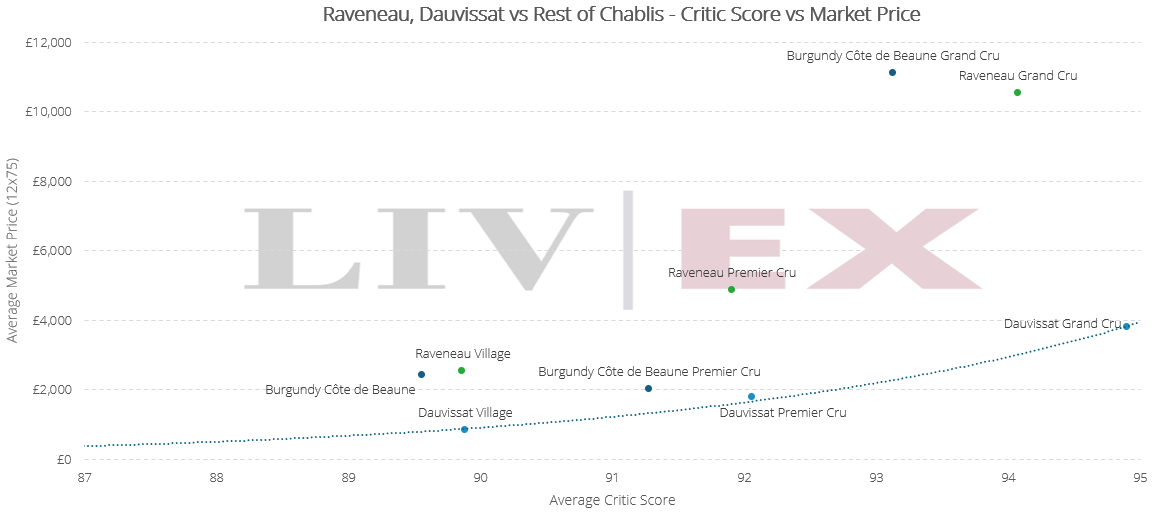

Raveneau and Dauvissat: In a Class of Their Own

While most Chablis wines are priced well below their Côte de Beaune counterparts, leading producers Raveneau and, to a lesser extent, Dauvissat command prices more in line with Côte de Beaune benchmarks than their Chablis neighbours. Nevertheless, their higher prices do accompany increased quality.

Dauvissat stands out, with each tier appearing an interesting proposition. It is perhaps Dauvissat Grands Crus that are the best opportunity of all Chablis wines. They are more highly rated than Raveneau Grands Crus (94.9 vs 94.1), yet are on average 64.0% cheaper.

As with other top-tier Burgundy white wines, however, liquidity is an issue with Chablis’ leading producers. Dauvissat and Raveneau tend to trade relatively infrequently. Given Chablis’ climate, the most marginal of all Burgundy’s sub-regions, this scarcity is only likely to increase as vintages grow more unpredictable under changing climate conditions.

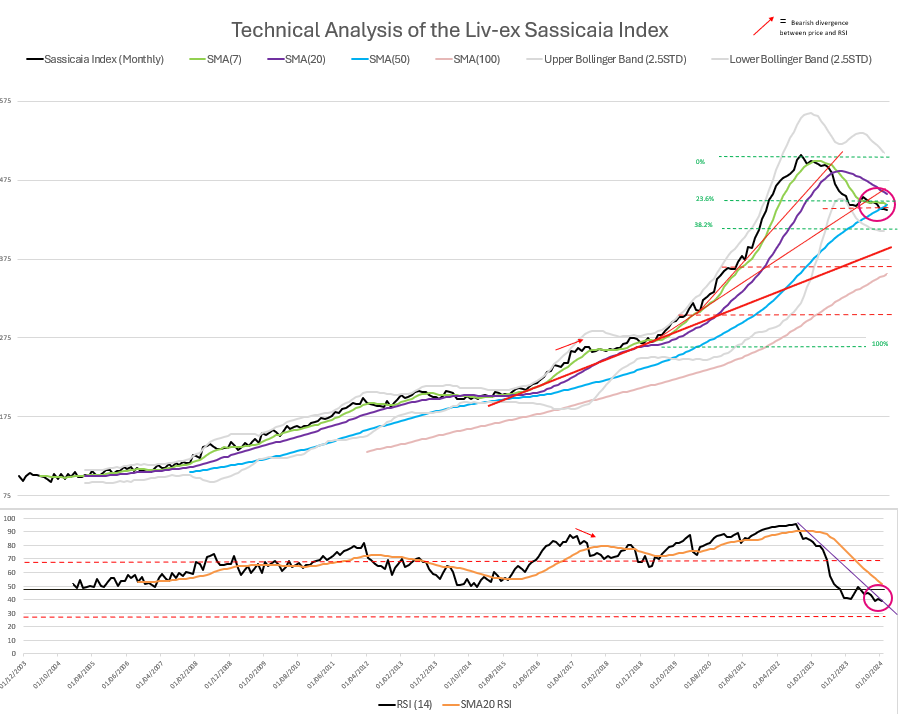

Chart of the Month – The Sassicaia Index

- While navigating a bearish phase, the Sassicaia index’s long-term bullish trend remains intact

- Technical analysis reveals no clear signal that the current downward trend will soon reverse

- The bid:offer ratio indicates increasingly positive market sentiment; ex-London release prices may act as support levels.

Counting all vintages, Tenuta San Guido’s Sassicaia is the second top-traded wine so far this year by volume, and fourth top-traded by value, up several places in both respects since 2023. While Sassicaia has strengthened its foothold on the market, prices have fallen since peaking in September 2022. Despite the 13.8% decline from its all-time high, the long-term bullish trend remains intact. Today, we employ technical analysis techniques to assess possible future price movements.

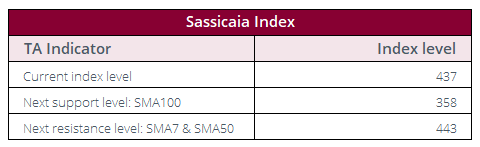

In August, the Sassicaia index crossed below its 50-month Simple Moving Average (SMA50), an indicator of the medium-term trend, for the first time since its inception. At 437, the index has just crossed below the SMA50 at 443, which is now acting as an immediate resistance. A short-term trend reversal – an end to the current bearish phase — would only be validated by a price break above the SMA7 and SMA50.

From 2003 until September 2023, the Relative Strength Index remained above 50 – the threshold above which momentum is considered upward. While it tested the 50 line in March this year, coinciding with a substantial increase in traded volumes after the 2021 vintage was released in February, the RSI has since remained below it. Still, at 38.9 Sassicaia is not yet in oversold territory. If the downward trendline continues to act as a resistance, we may see the RSI cross below 30 in the coming months.

As indicated by the wide Bollinger Bands, volatility remains high, leaving space for continued downward movement. Still, the slight flattening of the lower band may provide some protection from harsh price swings.

At this stage, technical analysis reveals no clear signal that current bearish momentum will reverse. Still, demand for Sassicaia remains promising. The bid:offer ratio (by value), across all vintages of Sassicaia, has increased from 0.48 in August, to 0.49 in September and to 0.58 in October. We have previously identified a sustained bid:offer ratio above 0.5 as a strong indicator of stability or upward price movement. Should this ratio hold or improve over the coming months, historical trends would suggest prices may hold.

In the months ahead, the key question is whether the Sassicaia Index can reclaim both the converging SMA7 and SMA50, signaling the potential end of the short-term downtrend. Should the price fail to hold this convergence zone, technical analysis would suggest that prices will fall to the horizontal support levels at 372 and 308 (15.3% and 29.8% below current levels).

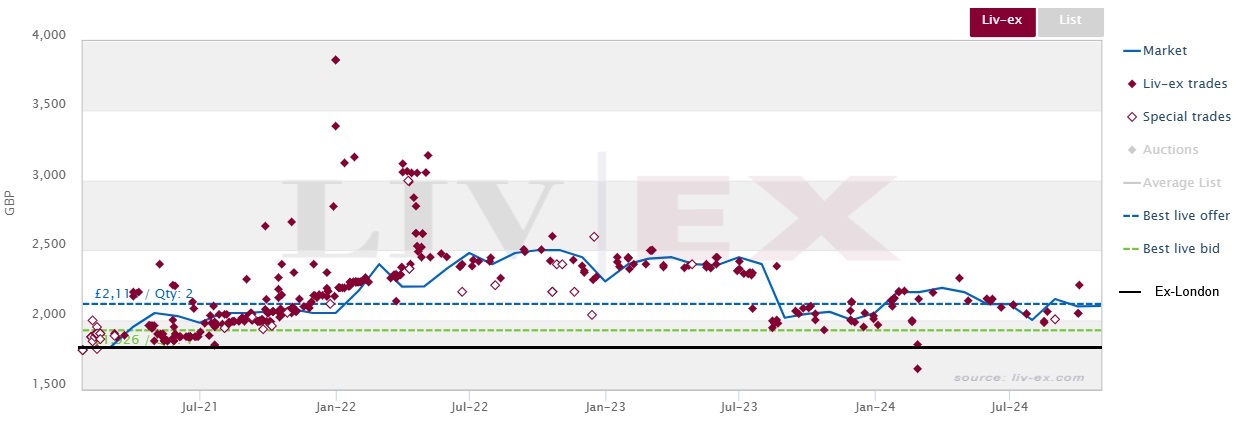

As further detailed in the next section of this report, we have recently seen prices of a number of Bordeaux wines cross below their ex-négoce and even ex-château prices. Release pricing of Sassicaia, however, has been more consistent than Bordeaux wines. Ranging from £2,000-£3,000 per 12×75 and generally receiving scores above 95 points, Sassicaia presents relative value. As has been the case for the 2018 vintage, released into the UK market at £1,800 and now trading frequently between £1,900 and £2,000, support may be found at ex-London release pricing.

Liv-ex trades of Sassicaia 2018

Bordeaux En Primeur – Who Wins?

Reports out of Bordeaux on the 2024 vintage have not been resoundingly cheerful. According to Jane Anson, ‘strong mildew pressure, poor flowering, and a relatively dry summer’ characterised the growing season. Funding for constant green harvesting and new cellar technologies may go some way towards protecting the quality of the wealthier châteaux’s wines, but yields are set to be notably low across the board.

While En Primeur is over six months away, châteaux, négociants and merchants will be beginning to plan their pricing and buying strategies. It is no secret that recent campaigns have not been hugely successful. Châteaux cut prices of the 2023s but, in most cases, not by enough to generate adequate demand from either merchants or consumers.

Tough growing seasons are expensive. Coupled with lower yields, châteaux will have to take a hit to their margins to release the 2024 at the right price – the price at which buying En Primeur is still profitable at each level of the supply chain.

Is En Primeur still working?

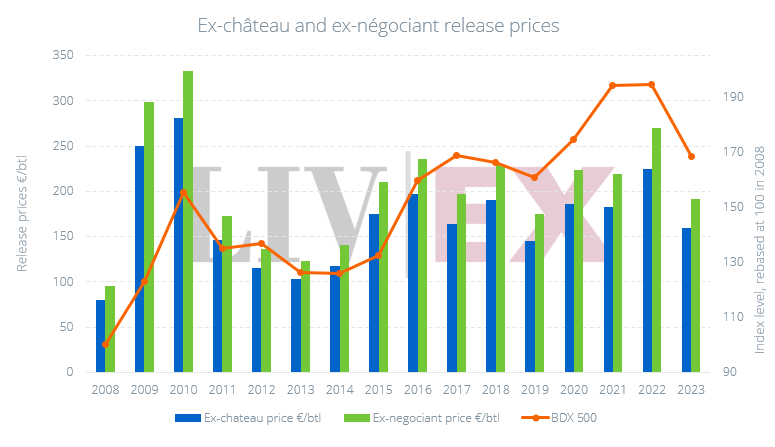

Currently, the Market Prices of all vintages after 2015 sit, on average, below ex-London release prices. End consumers, therefore, would have been better off buying now than at release. Except for the 2016, 2019 and not-yet-physical 2023 vintage, Market Prices for all post-2015 vintages sit lower than ex-négociant prices.

The 2019 vintage, released at the lowest price since 2014, presents as an anomaly. As we reported at the time, since the Covid-19 pandemic prevented En Primeur releases taking place at the châteaux as usual, most prices were offered before general critical opinions were received. Moreover, the 2019s were released during a period of high economic uncertainty, the effectiveness of bailouts not yet clear. As a result, Bordeaux producers played it safe and kept release prices low. Alongside vintages 2012-2015, it serves as an example of successful release pricing.

As the downturn of the market continues, we are beginning to see trade prices of some Bordeaux wines fall below their ex-château prices. At this stage, it becomes cheaper for négociants to purchase wine on the market rather than directly from châteaux, rendering En Primeur unprofitable, even for négociants. Will relationships along the supply chain hold together the En Primeur system, or will release prices need to meet the market for it to persist?

Ex-château and ex-négociant release pricing

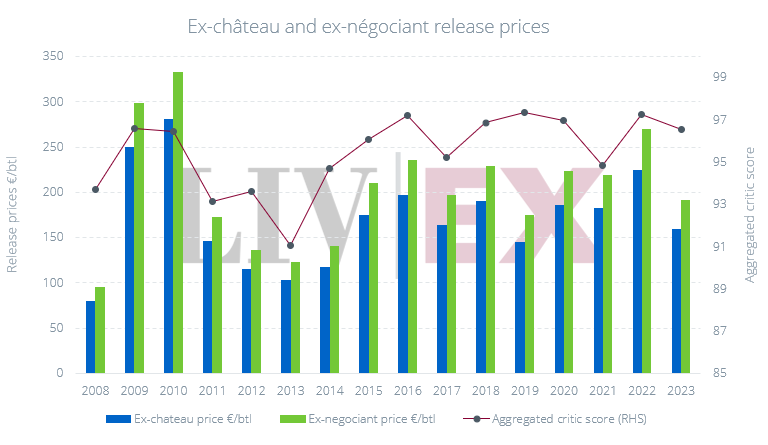

On the one hand, it appears that châteaux are responsive to both market conditions and the critical receptions of their wines. On the other hand, their responses to dips in the market have been more modest than their responses to peaks and critical acclaim.

The relationships between châteaux and négociants are long-standing and solid. It is unlikely that négociants will stray from the 16% margin châteaux recommend they take on En Primeur offerings – at least not publicly. While ‘Recommended Retail Prices’ have had some effect on ex-London release prices, it is UK merchants who are more likely to alter their margins to meet demand. For some previous vintages, a strengthening of Pound Sterling against the Euro has allowed UK merchants to lower prices without dropping their margins; in particular the 2014, when the euro-pound exchange rate dropped to c.0.71. Now, the exchange rate sits at 0.83. ECB interest rate cuts may lower the rate, but the Euro is likely to remain fairly strong.

Why are ex-château prices so high?

Over the past 10 years, many châteaux have poured funds into new wineries, technologies and marketing. Anecdotally, production costs have, in some cases, tripled. As recently reported by The Times, the popularity of Bordeaux in the 1990s led to significant overproduction. With consumer preferences moving away from Robert Parker claret and a subdued Chinese market, supply now far outweighs demand. Having spent lavishly during prosperous times, châteaux are now sitting on full warehouses and debt. Even though release prices are high, they may mark the lower limit of profitability.

Châteaux that can afford to lower prices but choose not to may be waiting on the market to turn, holding back the vast majority of their stock in hopes of re-releasing in more bullish years. With an increasing number of the Bordelais looking to sell their properties, it is also possible that some are keeping release prices high to drive up asset evaluations.

What happens if the En Primeur system fails?

That the end of the négociant distribution system — ‘cutting out the middleman’ — will necessarily benefit end consumers is a fallacy. Négociant networks are efficient and well-built; it will be a difficult and expensive endeavor for châteaux to build their own. In other words, if négociants are cut out, prices offered to UK merchants and consumers are unlikely to be lower. Moreover, not all châteaux will be able to construct their own networks. Already, the less wealthy châteaux are feeling financial pressure. There have been around 50 put up for sale this year alone.

What can we expect from the next En Primeur campaign?

The 2024 En Primeurs should be met with tempered expectations. On the one hand, with low scores and yields expected, châteaux may be more willing to slash prices – it makes more rational sense to take a lower margin on a small number of poorly rated wines (as was the case with the 2013 vintage). On the other hand, lower yields may put even more pressure on châteaux that are already struggling for cash.

*Data from this article was drawn from all 50 LWIN7s of the Bordeaux 500 for which an ex-château, ex-négociant and ex-London price were available from vintages 2008-2023. This totals 23 different wines (368 total vintages) across sub-indices.