What’s happening in the market?

After the region’s strong close last week, Burgundy has continued to increase its share of traded value. Armand Rousseau has overtaken Domaine de la Romanee-Conti as the top-traded Burgundian producer by value this week, with the 2016 and 2019 vintages of the Charmes-Chambertin Grand Cru changing hands.

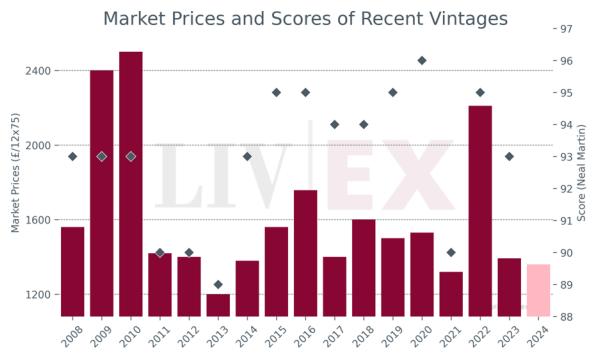

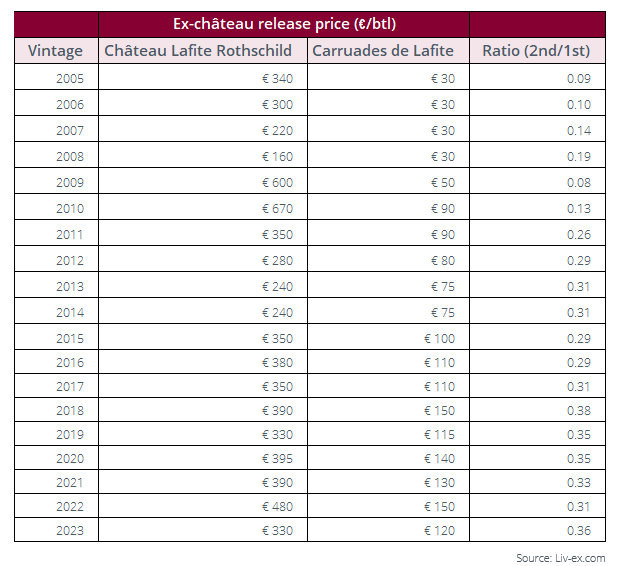

Fittingly, given the content of today’s deep dive, Carruades de Lafite 2020 is the top –traded Bordeaux wine of the week so far (by value). It is currently on offer at £1,728, just above its ex-négociant price of £1,705.

Today’s deep dive: has the ‘second wine’ bubble burst?

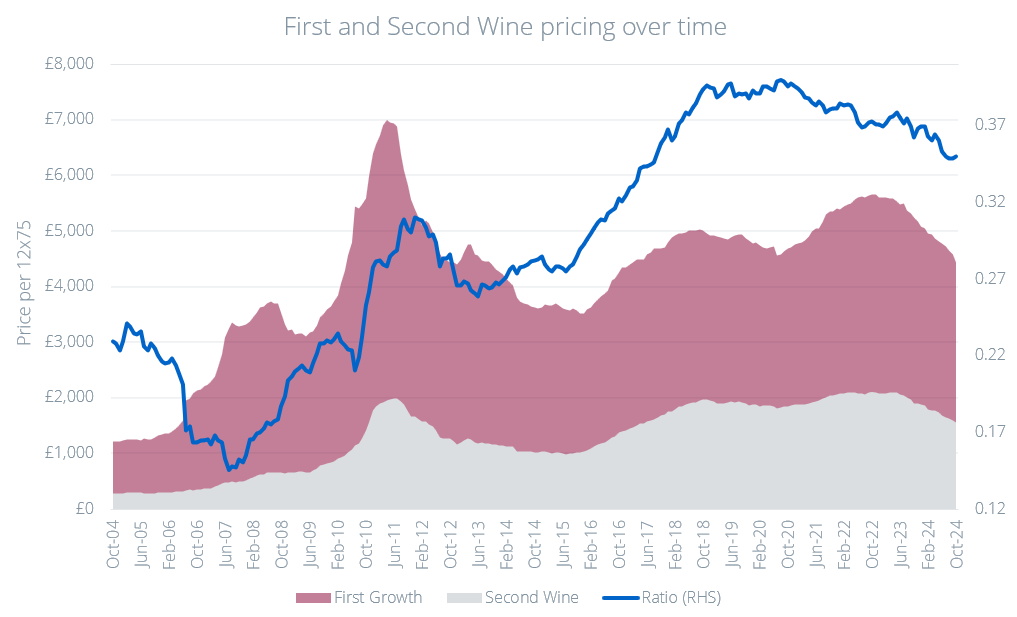

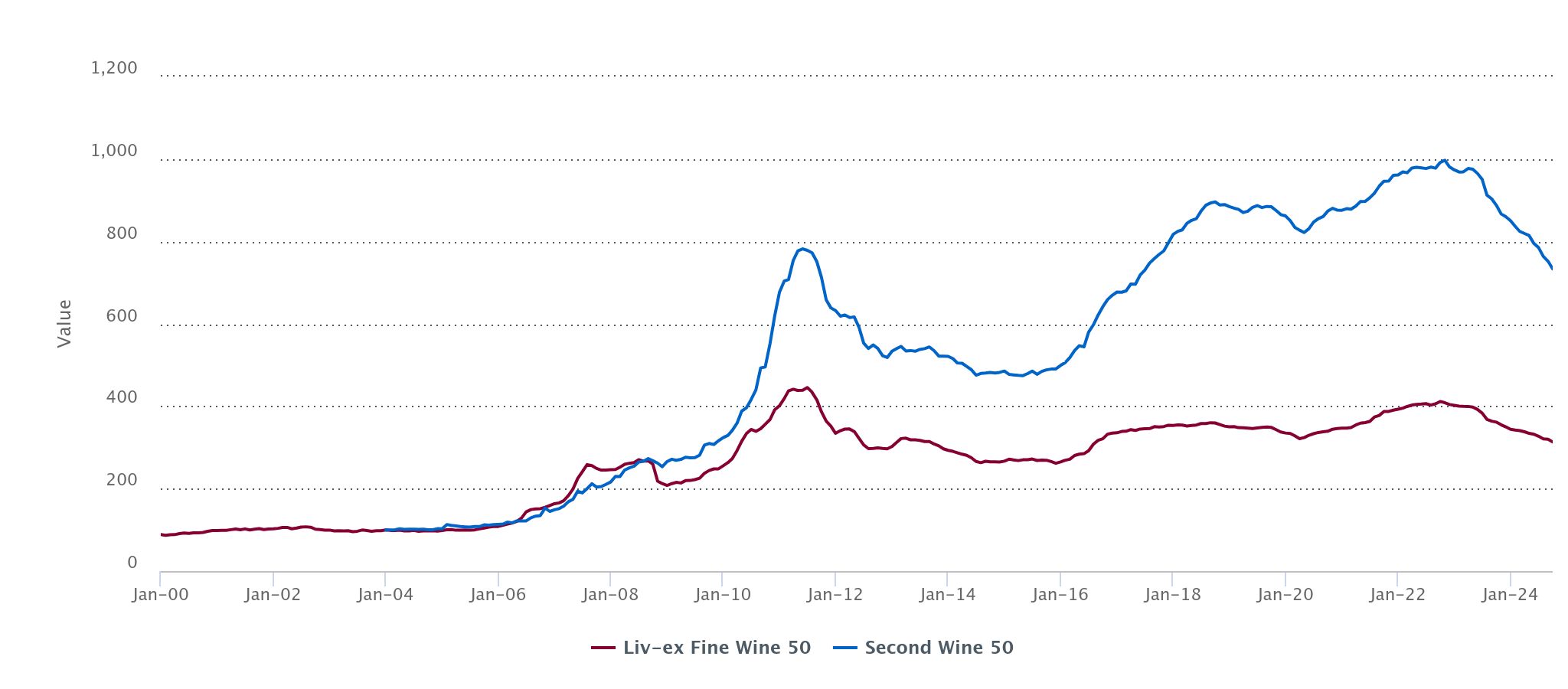

Over the past 20 years, second wines have become increasingly expensive relative to their first wines. In 2005, the First Growth second wines were, on average, around a fifth of the price of their first wines. The ratio peaked in 2018-2019 at which point Château Mouton Rothschild was only twice the price of Petit Mouton. Since then, however, the relative price of second wines to first wines has been falling. It would appear that, in this downward-moving market, buyers are turning to quality over brand.

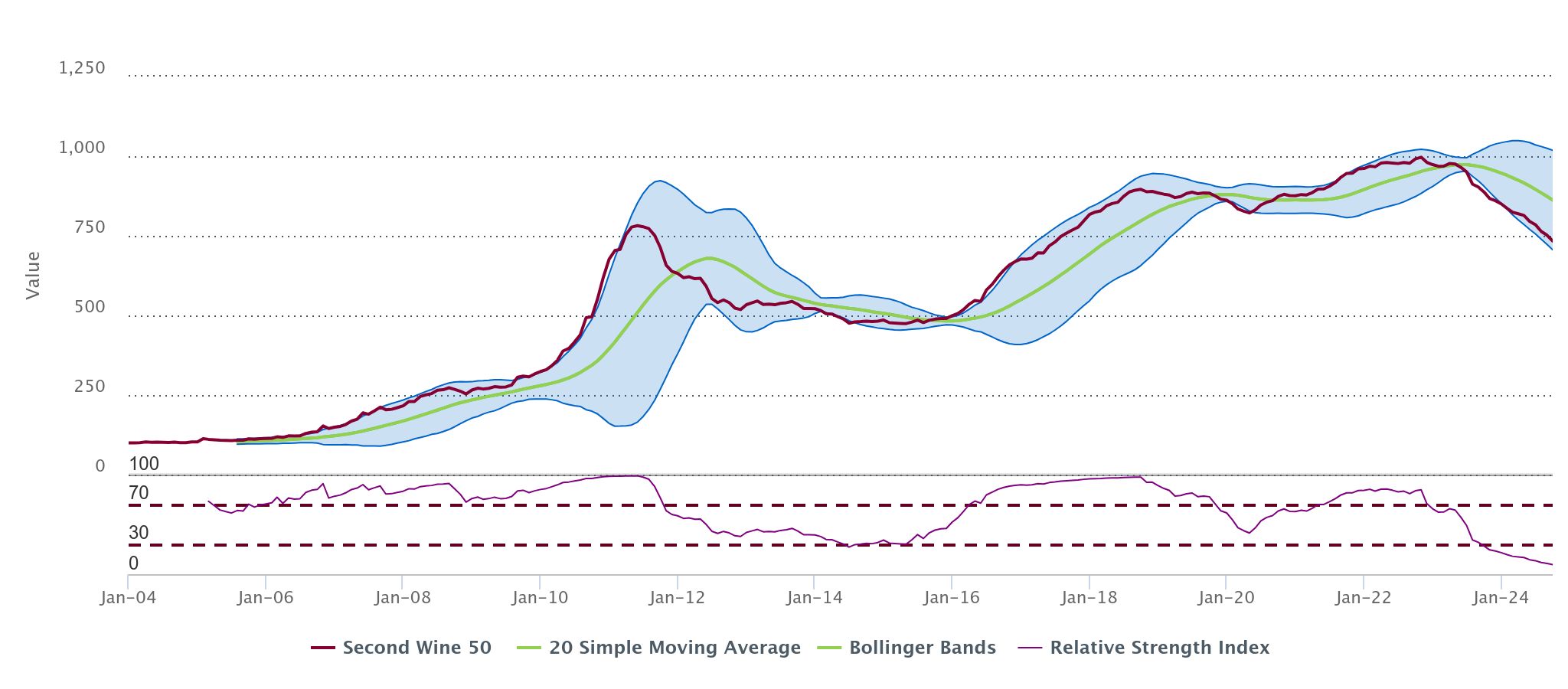

The chart below displays the monthly average Market Price of the First Growths and their second wines, overlayed with the ratio between them. Château Latour and Forts de Latour have been excluded, since their different release schedules and pricing model skew the data.

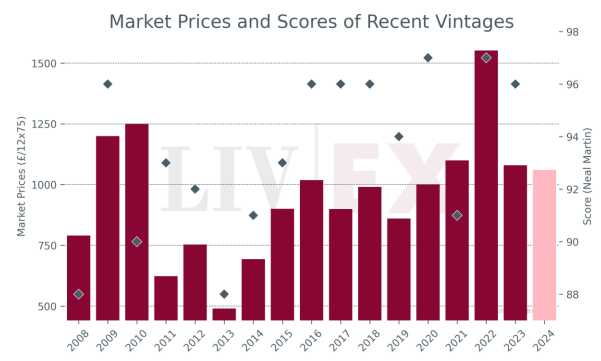

In the mid to late 2000s Bordeaux found immense popularity on the Chinese market. At the time, the fine wine market in China was highly brand focused, and none was more sought-after by buyers than Château Lafite Rothschild. Carruades de Lafite served for many new buyers as a proxy for the First Growth – simply by bearing the name ‘Lafite’, Carruades won prestige and thereby prices rose. The power the brand held in China sent prices of Carruades soaring disproportionately to its relative quality. To a lesser extent the same was true of Château Mouton Rothschild. The sudden increase in the second:first ratio for these two châteaux is apparent in the chart below.

While Chinese buyers remained active on the market, Carruades de Lafite and Petit Mouton were safe bets for resellers – consistently, allocations sold out and prices rose regardless of quality. Neither wine’s prices share any significant correlation with scores. Carruades 2014, for example, received a score of only 87 points from Neal Martin (Vinous) and is one of the most expensive recent vintages currently available on the market. In 2018, Carruades 2014 was available at three fifths of the price of Château Lafite Rothschild 2014.

In the past few years, however, China’s dominance of the Bordeaux market has weakened. The Chinese economy has been slow to recover after extended lockdowns and a massive correction in the property market decimating customer spending. Moreover, customs rules have tightened, and markets have become more strictly regulated. Many high-net-worth individuals are choosing to leave China and Hong Kong as a result of political and economic uncertainty, diminishing demand for fine wines overall. Despite this, châteaux have kept release pricing of their second wines high relative to their first wines. This year, Carruades de Lafite cost négociants over a third of the price of Château Lafite Rothschild (2023 vintage).

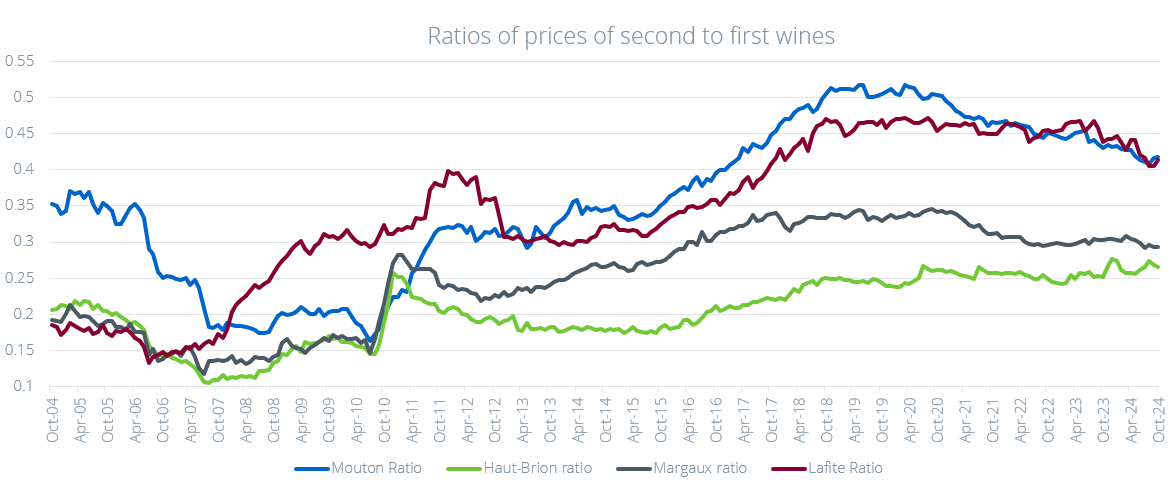

The Second Wine 50’s Relative Strength Index neared 100 in both 2011 and 2018 — well into overbought territory. Prices of the seconds have been falling faster than the First Growths since the turn of the market, and do not appear to be flattening in the near future. Prices had been artificially overinflated – propped up by a Chinese market that is no longer so dominant. Merchants and speculators had previously been able to rely on brand power to maintain the profitability of the trade, but now it would seem that quality is the metric that increasingly governs trading behaviour.

The price ratio of second to first wines will need to be corrected — it is likely that the prices of the seconds will continue to fall faster than the firsts. The question remains, will the ratio need to fall back to pre-2010 levels, or does there now exist a higher equilibrium?

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.