What’s happening in the market?

Bordeaux has dominated trade so far this week, taking 49.0% of traded value. Mouton Rothschild has been the top-traded producer, followed by Angélus and Le Pin.

Burgundy has taken 15.4% of traded value, with Leroy Vosne-Romanée, Les Beaux Monts 2011 trading. Jean-Luc & Eric Burguet, Gevrey-Chambertin, Mes Favorites Vieilles Vignes 2015 has also been trading in high volumes.

This week has also seen Latour release 12,000 bottles of the 2009 ex-château. It was offered at €910 per bottle from La Place de Bordeaux, with merchants offering it internationally at £11,000 per 12×75.

Today’s deep dive: An update on the DRC index

Key findings:

- DRC prices have fallen sharply over the summer – as hypothesised was more than likely by Technical Analysis in June

- For the first time, the DRC index’s Relative Strength Index (RSI) has dipped below 30, the threshold at which it is considered ‘oversold’

- Volatility remains high and, at present, technical indicators do not point to a trend reversal

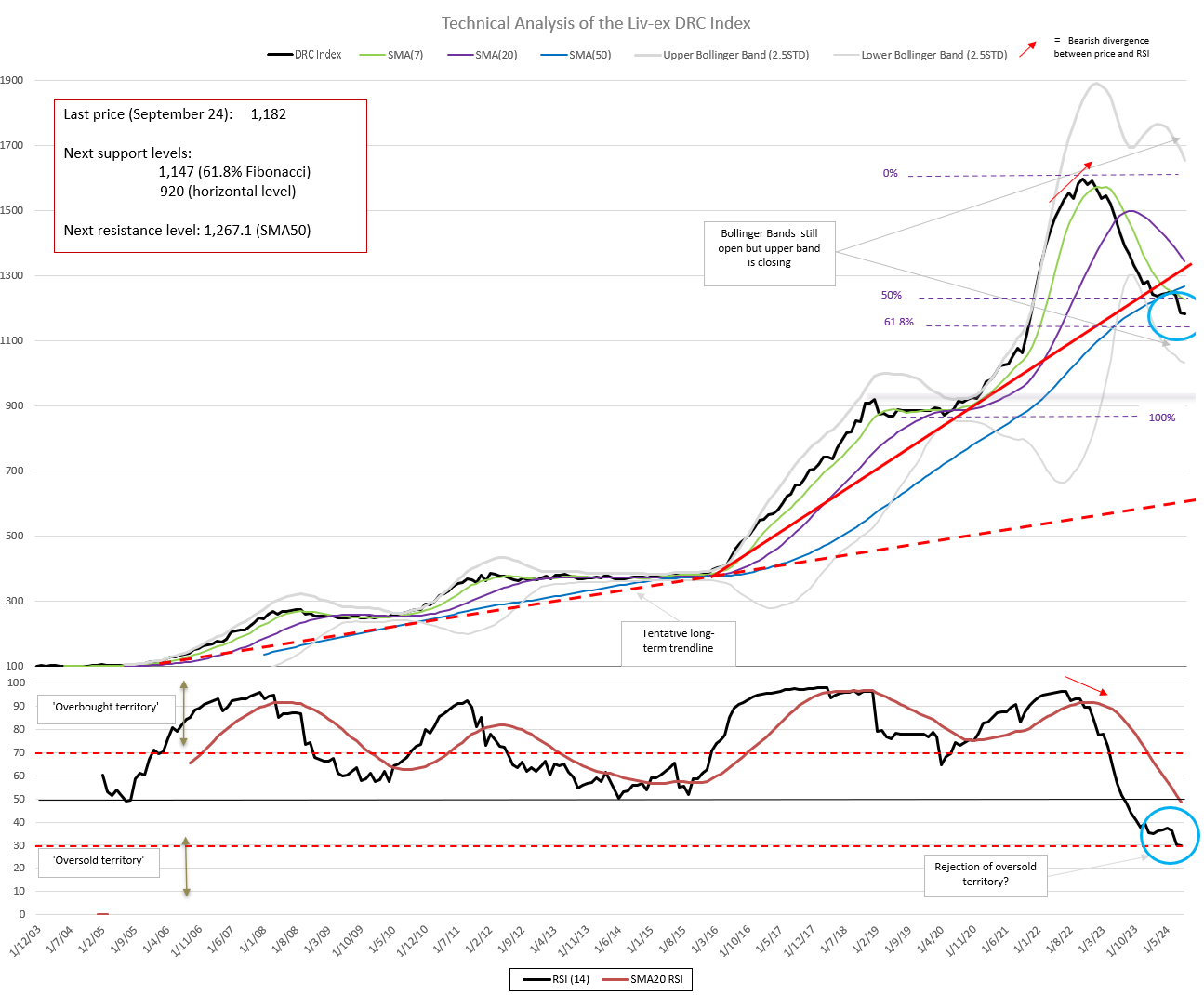

In June, Liv-ex published a technical analysis of the Domaine de la Romanée-Conti price index. At the time, prices had stabilised slightly but have since fallen sharply – an outcome the technical analysis hypothesised was more than likely. In August, we published a piece on how market participants can seek to make the most of this dip, by acquiring investment-grade cases at low prices. The remaining question, that we seek to answer using technical analysis techniques today is how much further prices might fall before we will see a recovery.

The Domaine de la Romanée-Conti index (which comprises the 10 most recent physical vintages of Romanée-Conti, La Tâche, Richebourg, Romanée-Saint-Vivant, Echezeaux, and Grands Echezeaux) has maintained a long-term bullish trend since its inception in 2003. While this trend, as represented by the Simple Moving Average (SMA)50, remains intact, the index has recently dipped below this long-term trendline. Both the SMA7 and SMA20 are downward sloping – in both the short and medium term, the market for Domaine de la Romanée-Conti is firmly bearish.

For the first time since the index’s inception, its Relative Strength Index (RSI) has dipped below 30, the threshold at which the index is considered ‘oversold’, and now sits at 29.9. In August, we saw only a minimal decline, which may indicate that the RSI has rejected ‘oversold territory’. Still, given that prior to mid 2023 the RSI had never crossed below 50, there is the possibility that we will see prices correct further.

The index’s volatility, as measured with Bollinger Bands, remains very high. While the upper band appears to be closing, the lower is continuing to widen, suggesting we are likely to continue to see downward price swings. Technical indicators do not, at this stage, point to an upcoming trend reversal.

In June, we suggested that if prices broke below the SMA50, they would continue to fall to the 61.8% Fibonacci retracement level (1,147). We will monitor the index closely to see whether or not this level provides adequate support. Should prices break below it, the 76.8% retracement level, followed by the 2021 lows (920), would be the next supports.

Prices are likely still falling, but this doesn’t mean buyers should hold off until they reach their floor. Since the start of the year, offers by litre volume have been falling while bids have been rising. Given DRC’s scarcity, obtaining cases is not always easy. Moreover, they largely retain their value after their drinking window. Should prices continue to fall, more potential sellers may choose to hold their stock or take their chances at auction.

There are currently 351 LIVE opportunities on Liv-ex for Domaine de la Romanée-Conti. Log into the exchange to view them here.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.