What’s happening in the market?

So far this week, Bordeaux has led the market with a 35.3% share of traded value. The region was buoyed by trades of Château Lafite Rothschild. While the 2008 and 2018 vintages were also active, the 2019, which came in as the top-traded wine in H1 2024, took the top spot by value. It traded this week at £4,700 per 12×75, marking the lowest recorded transaction price for the wine since its release.

Burgundy came in second, with Domaine de la Romanée-Conti accounting for 45.0% of the region’s trade. Mature DRC vintages, such as Echezeaux 2002 and and Romanée-Conti 1994, were more actively traded.

Today’s deep dive: how far below Market Price are trades taking place?

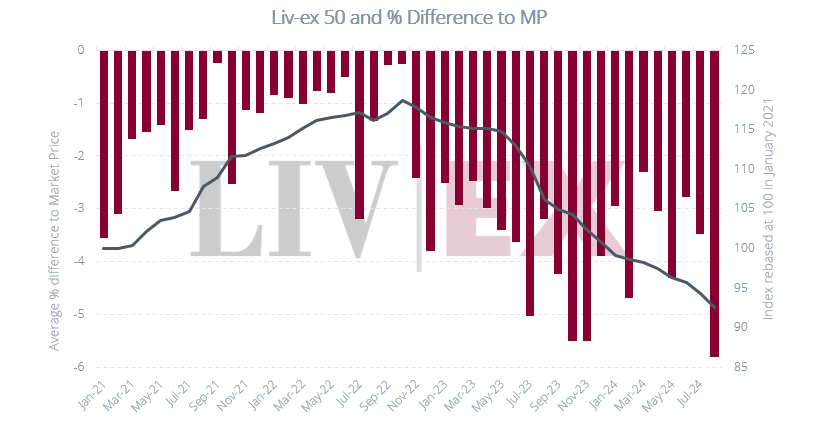

So far this year, across all wines, trades have occurred, on average, 4.7% below the Market Price. In 2023 and 2022, trades averaged 4.4% and 3.3% below Market Price respectively. As the market has moved down, the gap between lowest listed price and actual traded price has been widening. Though merchants are acquiring wines at lower prices on the secondary market, many are keeping their listed prices high. Today, we turn our attention to the average difference between trade prices and Market Prices for the Liv-ex Fine Wine 50 over time.

While the difference between average trade price and average Market Price more than doubled from 2022 to 2023 for the Liv-ex Fine Wine 50 (1.4% vs. 4.0%), the gap has closed slightly in 2024. So far this year, trades of component wines have occurred, on average, 3.5% below Market Price.

Between October 2022 and November 2023, the average gap between trade and Market Prices for the Liv-ex Fine Wine 50 grew considerably. During that period, the index, though faltering at its peak, held relatively flat until May 2023. Given that the indices are calculated using Mid Price, the midpoint between the lowest offer and highest bid, or any trades struck within, the index is a true and tested measure of actual transactions. Between October 2022 and May 2023 traded prices remained relatively flat. The widening difference between trade and Market Price, then, suggests the continued lifting of list prices, just as the market began to waver. Those who bought at the December 2022 peak, realising the bull run was over, attempted to sell their stock high online, but accepted no-loss bids on the secondary market.

Analysis of this price gap may be useful to us as a measure of market sentiment. Just as the widening of the gap predated the downturn of the market, a convergence of Market Price and trade prices closer to 2% may spell good news for the index.

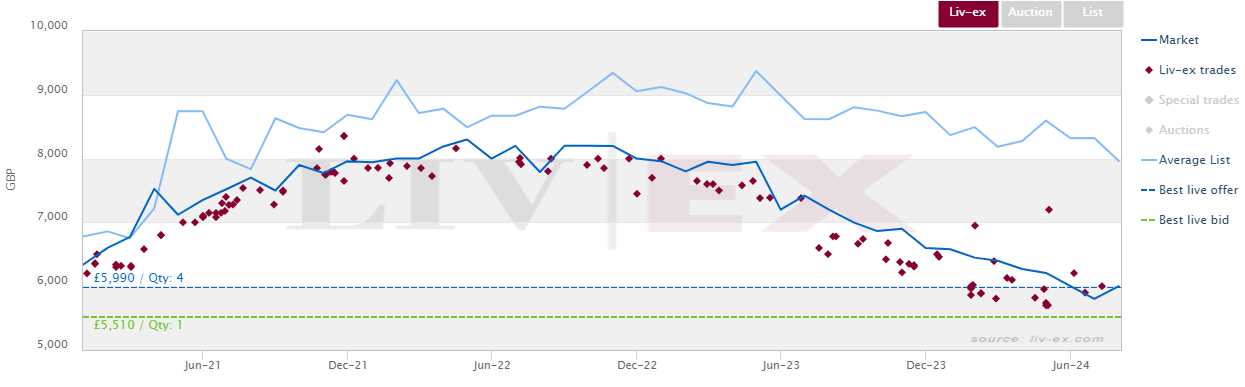

Looking at prices and trades of Château Lafite Rothschild 2016 over the same period, we can observe this pattern at a more granular level.

Trades of Château Lafite Rothschild 2016 on Liv-ex

From early 2021 to early 2022, the gaps between trading prices, Market (lowest listed) Price and average list price grew increasingly tight. After this stage, all three began to diverge. Of particular note is the average list price, which has hardly fallen since the turn of the market.

It is not unusual for LIVE offers to be lower than listed prices. But in a bear market, this discount becomes more exaggerated, presenting buyers with a greater opportunity. Considering only the Liv-ex Fine Wine 50 so far this year, trades triggered by buyers have occurred 1.7% below Market Price, while trades triggered by sellers have occurred 5.0% below Market Price. Buyers are holding their bids low, drawing sellers to them. For now, buyers hold most of the cards and are happy to play the waiting game. This said, the aggregated value of LIVE bids has begun to creep up, hinting perhaps that some buyers are beginning to see value.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.