What’s happening in the market?

So far this week, Bordeaux’s trade share has decreased from its close last week at 40.3% to only 24.6%. Of the overall top five wines by traded value, only one – Le Pin 2020 – hailed from Bordeaux.

Burgundy followed, with a 22.5% share of trade. The region was buoyed by trades of high-value wines, including the 2011 and 2014 vintages of Domaine Leroy’s Romanée-Saint-Vivant, and the 2016, 2017 and 2018 vintages of Domaine de la Romanée-Conti’s Richebourg.

Salon Le Mesnil 2012 took the top spot as overall top-traded wine by value, pulling Champagne’s share of trade up to 16.0%.

Isole e Olena Cepparello 2021 was released in Italy in April and has now entered the UK market. This week, it comes in as the fourth most-traded wine by value from Tuscany, behind two vintages of Sassicaia (2018 and 2020) and Tignanello 2021. As reported by Jancis Robinson, the estate was acquired in 2022 by the EPI group, and the 2021 vintage is the last produced by Paolo de Marchi.

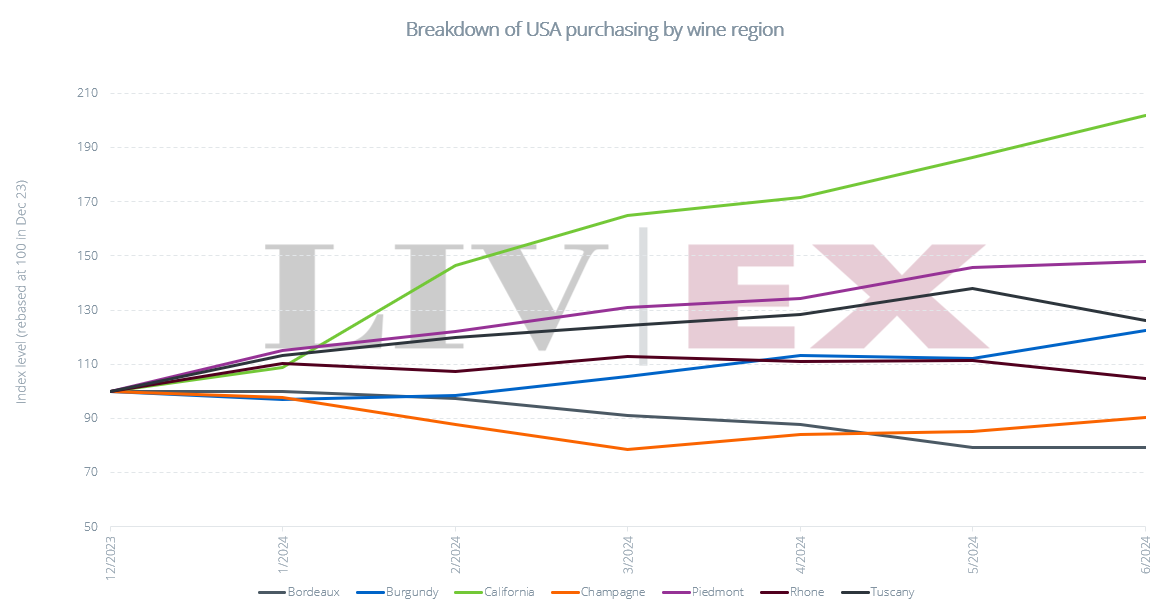

Today’s deep dive: which regions are US merchants buying?

In H1 2024, US-based Liv-ex members accounted for 32.5% of all purchased value on the exchange, second only to UK-based buyers, who accounted for 34.3% of all purchases. US purchasing has been steadily rising, solidifying the country’s prominence in the secondary market. In today’s deep dive, we look at US buying habits over time.

While US purchasing volume in H1 2024 is up by 4.1% on H2 2023, purchasing value is up by only 0.8%. Overall, US merchants are buying more wine, but spending less per trade. Though, in part, this can be explained by declining prices, it is also clear that buyers are opting for lower value wines. This is not, however, the case across all wine regions. The chart below shows a rolling 6-month average of US buying by value since the start of the year, broken down by region.

Since the start of 2023, US buyers have focused increasingly on wines from California, Piedmont, Tuscany and the Rhone. They have been turning to these regions in lieu of Bordeaux and Champagne, which have both seen decreased purchasing from US buyers.

While produced on their doorstep, US buyers are increasingly turning to the secondary market for Californian wines. The value bought by the US in H1 2024 has more than doubled on H2 2023. Volumes however have increased by only 75%, pointing to greater demand for higher value wines. This growth has affirmed the US as prominent buyers of the region. While they accounted for only 5% of purchases of US wines in 2023, YTD this number has increased to 16.5%.

Given how tightly allocated the top Californian wines are, buyers may be attracted to the liquidity on the exchange. It may also be the case that US buyers have been capitalising on lower international pricing.

As we reported in May, the strong dollar has provided US buyers with an opportunity to buy more cheaply abroad. Taking the most popular Californian wine amongst US buyers from H1 2024, Joseph Phelps Insignia 2019, as an example, we can analyse the difference in UK and US markets. The cheapest listed price in the UK is £2,060 per 12×75, while the cheapest listed price in the US is $2,938 (considering only stocked wine prices). Using the current pound:dollar exchange rate of 0.77, this equates to £2,273. In April, at an exchange rate of 0.81, this would have been even higher – £2,380. Whether US buyers have been turning to the secondary market for liquidity, or thinking more consciously about buying abroad while the dollar is strong, there are lucrative opportunities available to them.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.