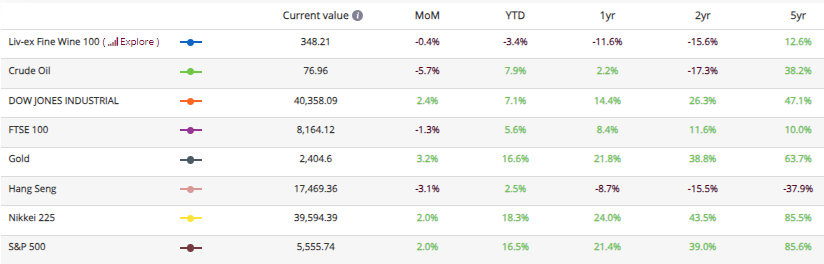

The fine wine market in H1 2024

Introduction

H1 2024 saw the fine wine market’s downward trend continue. With the market still looking for where the bottom might lie, H2 is likely to see participants tip-toeing their way through a weak market.

As we reflect on the first half of 2024, a period marked by significant geopolitical upheavals and increased volatility in global financial markets, it’s clear that many of the challenges of 2023 have run over to this year.

Sustained tight monetary policy has left consumers short on cash while businesses continue to hold back on investment. With political uncertainty and global conflict dominating the headlines, investors are spending more carefully than ever.

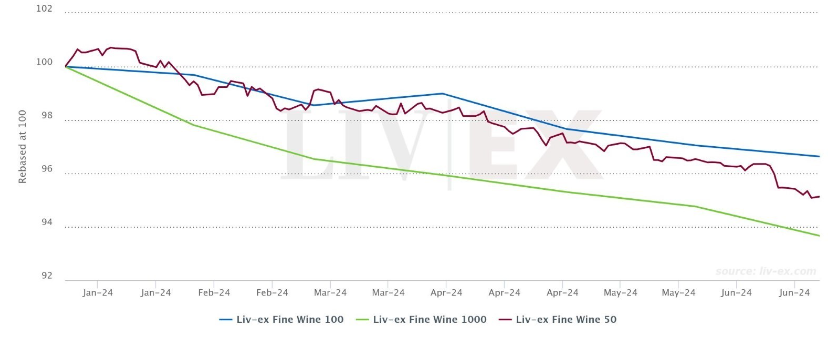

The fine wine market has not been immune to the uncertainty marking the wider economic landscape. 2024 has so far been marked by falls across all the major Liv-ex indices, with buyers and sellers still wondering where the bottom might lie. However, there have been upticks, if only temporary, across some pockets of the market, suggesting it may be looking for a turning point.

In April, the Liv-ex Fine Wine 100 (the industry-leading benchmark which tracks the 100 most-traded fine wines on the secondary market) recorded its first positive movement in 12 months, hinting at light at the end of tunnel.

The back end of H1 was dominated by the Bordeaux 2023 En Primeur campaign, with wines released into a market that was 13.4% down since the release of the 2022s. Despite some significant reductions on the 2022 release prices, the campaign has faced criticism from all sides and the sustainability of the entire system has been called into question.

The market is still trending down and while there are some green shoots, the next six months will likely see participants tip-toeing their way through a weak market.

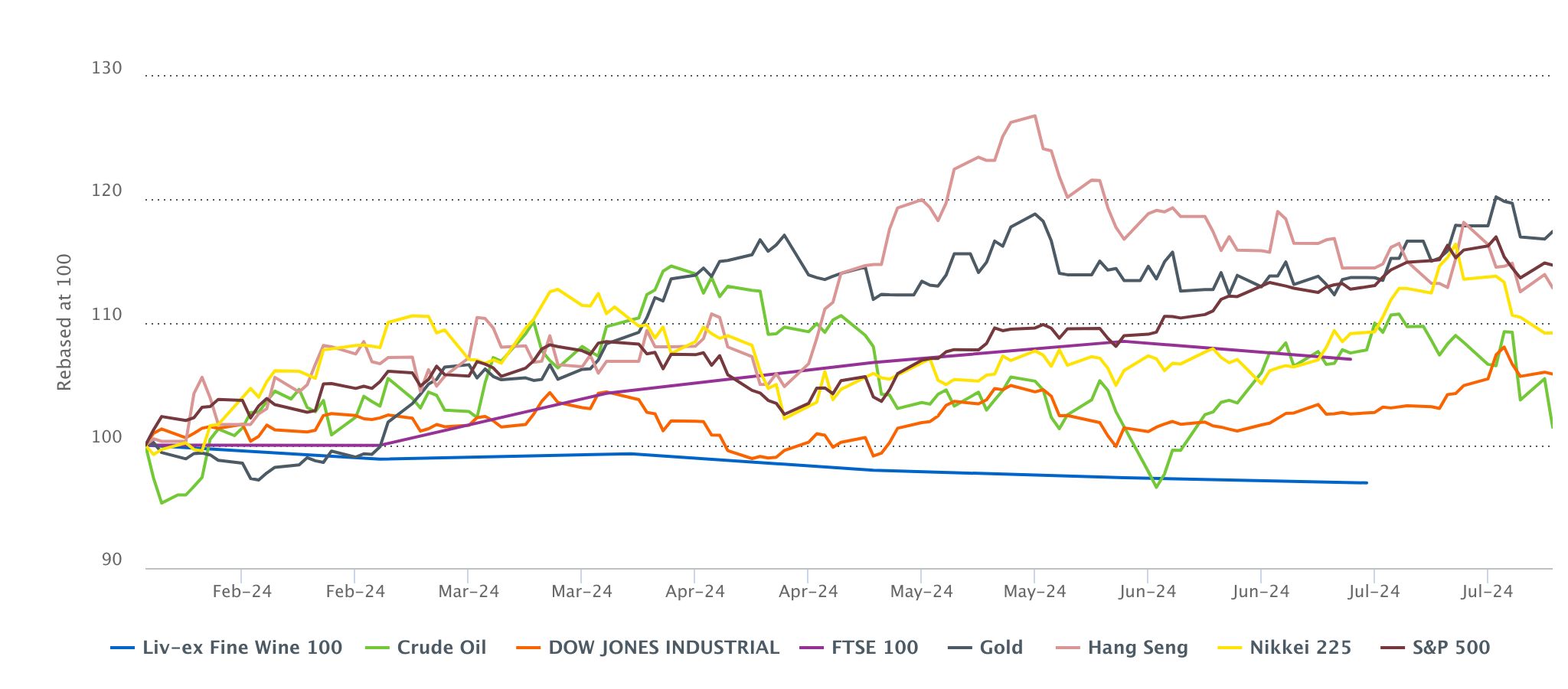

Fine Wine 100 vs equities

*made using the Liv-ex Charting Tool. Data taken on 24.07.2024.

In contrast to the fine wine market, all other major indices recorded increases in H1, of between 3.8% and 18.3%. The fine wine market (represented by the Liv-ex Fine Wine 100) fell by 3.4%, continuing the downward trend that started towards the end of 2022. It ended H1 down 17.9% from its September 2022 peak.

While the fine wine market’s slide continued through H1, the Hang Seng enjoyed a reversal of fortunes from February onwards, overturning its earlier falls to record a 3.9% increase over the period. It has, however, since given back some of these gains. The Nikkei 225 continued the bullish run it’s been on for the past two years, adding a further 18.3%.

While Crude Oil, whose supply chain has been severely threatened by geopolitical insecurity this year, displayed significant volatility, the Dow Jones Industrial recorded modest but relatively stable growth.

*made using the Liv-ex Charting Tool. Data taken on 24.07.2024.

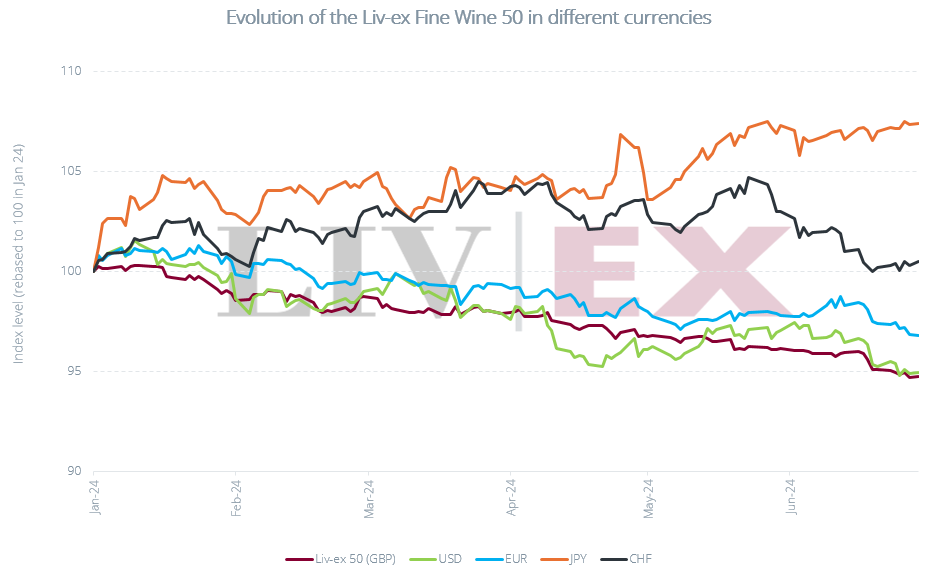

Currency overview

In H1, the US dollar generally strengthened against other major currencies. Largely due to the Federal Reserve maintaining high interest rates, dollar-denominated assets became more attractive to investors.

The relative strength of the dollar continues to be felt on the secondary fine wine market, where US buyers accounted for 32.5% of all purchasing by value. This is just above its share during H2 2023 (31.1%). For comparison, the UK accounted for 34.3% of all purchases.

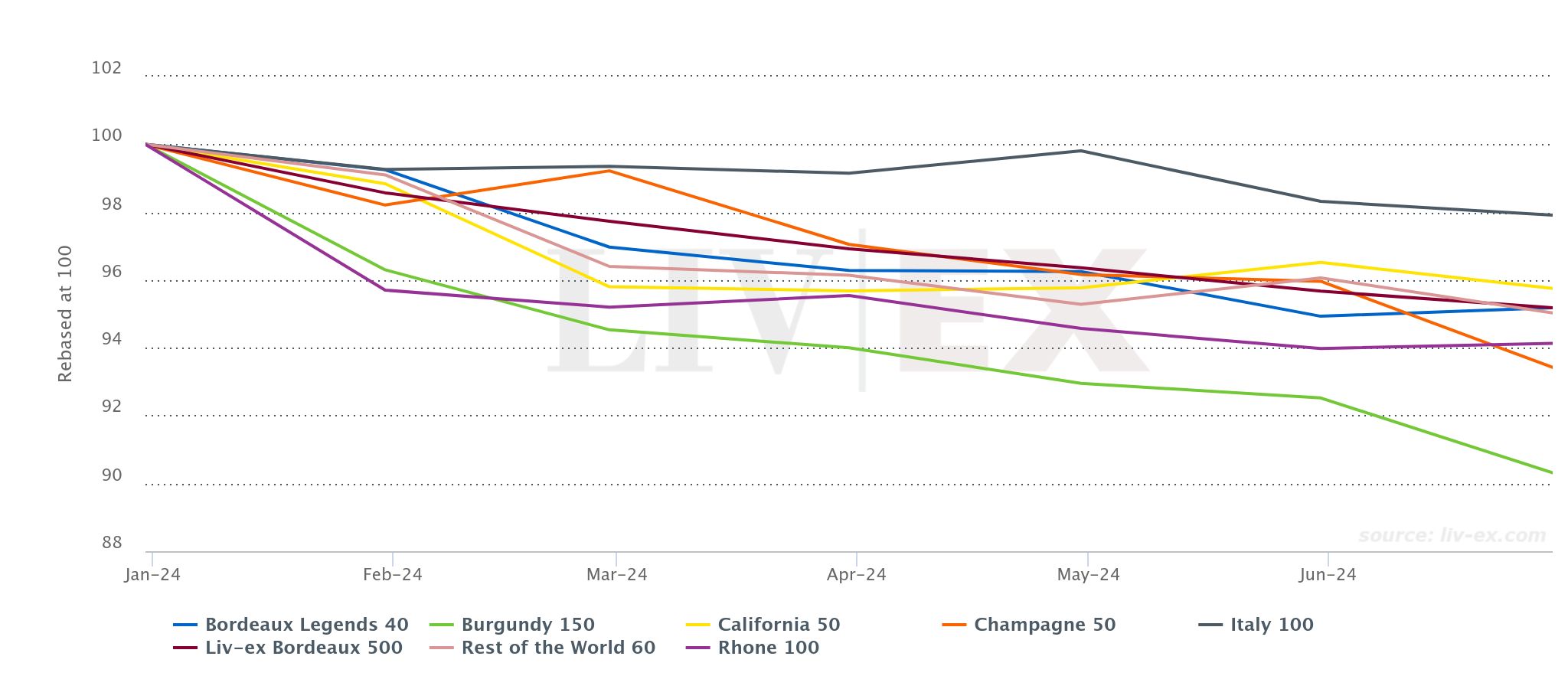

Liv-ex 1000 sub-indices

*made using the Liv-ex Charting Tool. Data taken on 17.07.2024.

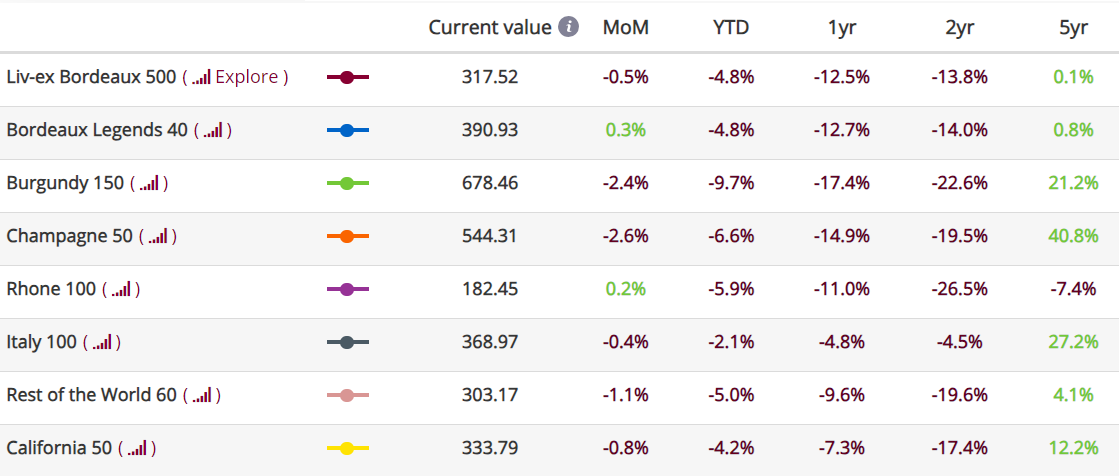

When we drill into sub-indices of the Liv-ex 1000, we can see that various pockets of the market offered greater shelter in the storm. At the end of 2023 we dubbed the Italy 100 the face of resilience, and it has continued to be so in 2024. The Italy 100, which tracks the price performance of the ten most recent physical vintages of five Super Tuscans and five other leading Italian producers, has been the best performer among the sub-indices of the Liv-ex Fine Wine 1000. Year-to-date it has declined 2.1%, compared to 4.2% for the California 50, the next best performer. At the other end of the spectrum are the Burgundy 150 (-9.7%) and the Champagne 50 (-5.9%).

The current downturn has come with a shift to safe havens in the market – specifically older Bordeaux vintages. In the last six months this can be seen by the slight June uptick (+0.3%) for the Bordeaux Legends 40 which tracks the price performance of a selection of 40 Bordeaux wines from exceptional older vintages. Furthermore, the Liv-ex Fine Wine Investables Index, which was designed to track the highest-scoring Bordeaux wines commonly found in investment portfolios has only dropped 3.3% year-to-date.

*made using the Liv-ex Charting Tool. Data taken on 17.07.2024.

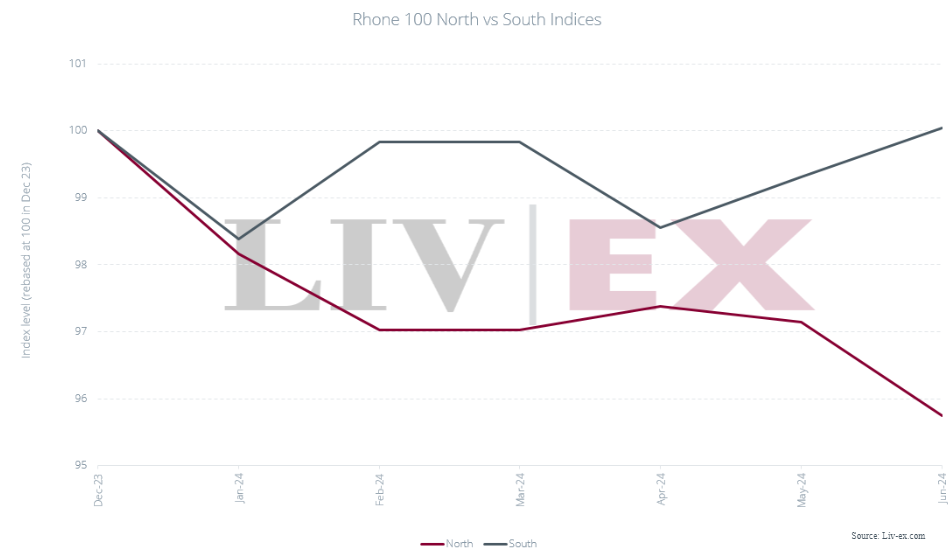

Pockets of relative stability in the Liv-ex 1000

Drilling down into the performance of individual wines from the Liv-ex 1000 over H1, we see a number of Châteauneuf-du-Papes have performed relatively well.

The region tends to fly under the radar, accounting for 1.7% of total trade value for H1. Furthermore, opinion of the region’s performance tends to be tightly tied to that of the region’s great outlier – Château Rayas – whose prices have fallen significantly over the past 18 months. However, if we look beyond, splitting out the Northern and Southern constituents of the Rhône 100, we can see that the Southern Rhône index – comprised of leading Châteauneuf-du-Pape wines excluding Rayas – ended H1 flat.

Trade overview

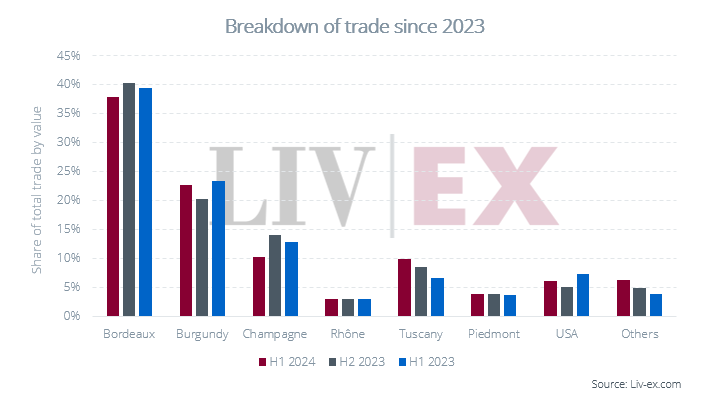

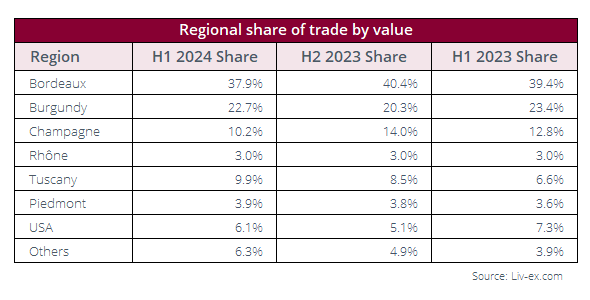

Overall, trade value for H1 2024 is down by 4.5% on H2 2023, a far milder decrease than the 9.3% decrease between H1 2023 and H2 2023. Trade volume in the first half of this year represents only a 0.3% decrease on H2 2023, once again down from the 2.2% decrease between the first and second half of last year. This is welcome news for the fine wine market – though prices are still falling, they are doing so less sharply, and investors are continuing to buy.

In the first half of 2024, Bordeaux retained its lead in the fine wine market. The region’s 37.9% share of trade by value, however, represents a decrease on H2 2023’s 40.4% and H1 2023’s 39.4%.

Burgundy has taken a greater share of trade than in H2 2023 (20.3%), but still less than in H1 2023 (23.4%). High-value wines from Domaine de la Romanée–Conti, Emmanuel Rouget and Domaine Armand Rousseau have buoyed trade value in the region.

Champagne is down 4% from its close at 14% in H2 2023. Several new vintages from the Grandes Marques have been released so far this year, though many have been considered overpriced.

Demand for Tuscan wine has increased steadily, with wines from the region constituting almost 10% of traded value. As expected, Super Tuscans led the charge, with Tenuta San Guido’s Sassicaia and Antinori’s Tignanello taking the largest share of trade value in the region. From Brunello di Montalcino, wines from Biondi-Santi, Marroneto and Argiano saw the most action.

The ‘Others’ category has risen continuously since 2023. Spain accounts for the lion’s share of traded value in the category and has proven more popular in the first half of this year than last year. This is mainly thanks to increased trade of Vega Sicilia’s wines – both traded value and volume have more than tripled since H2 2023.

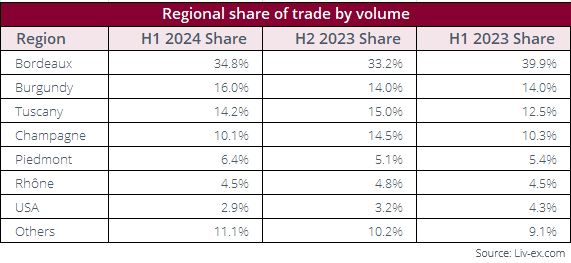

Breaking down the trade share by volume provides further context.

While Bordeaux lost a proportion of trade by value since H2 2023, its share of trade by volume is slightly up. Champagne’s share of trade volume has fallen at a very similar rate to its share of value. Within the ‘Others’ category, Spain accounted for 3.6% of trade volume in H1, and so took a greater share than the USA.

Top-traded wines

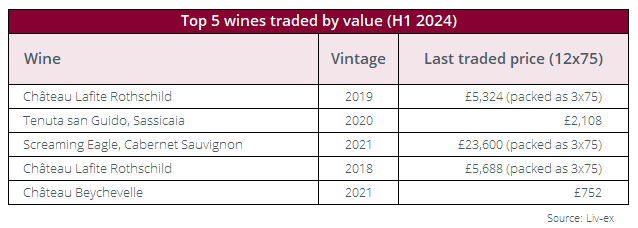

Château Lafite Rothschild 2019 took first place as the top-traded wine by value during H1. While the wine topped the list of most-searched-for wines during Q4 2023, it did not feature amongst the top-traded.

Screaming Eagle Cabernet Sauvignon 2021, recently rescored 100 points by Antonio Galloni (Vinous), represents the only California wine amongst the top five wines traded by value this year. This is the first time a wine from the region has placed amongst the top five over a half year. As expected with an allocated California wine, a majority (73.0%) of sellers hailed from the US, while 97.2% of buyers were located in the UK.

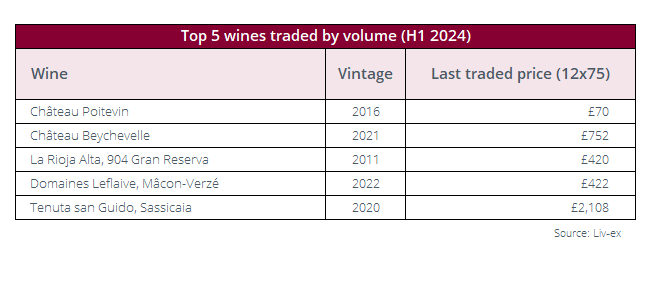

Thanks to a small number of high-volume trades, Château Poitevin 2016 came in first as the top-traded wine by volume in H1 2024. Château Beychevelle 2021 followed, buoyed somewhat by trades of imperial (6L) size bottles immediately after the release of the 2023 vintage.

Tenuta San Guido’s Sassicaia 2020 featured in the top five traded by both volume and value, reaffirming its demand in the secondary market.

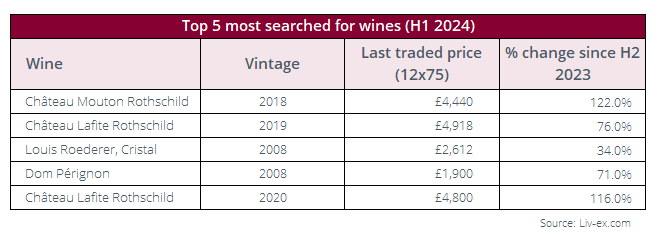

Most-searched-for wines

Château Mouton Rothschild 2018 topped the list of most-searched-for wines in H1 2024, with searches up 122% on H2 2023. Despite not featuring amongst the top five top-traded by value or volume, traded volumes of Mouton 2018 are up by 230% and traded value is up by 168%.

Unsurprisingly, given the producer’s dominance in the top-traded wines by value, two vintages of Château Lafite Rothschild, the 2019 and 2020, were also included in the list.

While trades of Champagne are down, two wines from the region, Dom Pérignon 2008 and Louis Roederer Cristal 2008 are amongst the most-searched-for on the exchange. Traded volume of Dom Pérignon 2008 is up by 33% on H2 2023, but traded value is down by 2%. Though the wine has enjoyed increased popularity, it is trading at lower prices than last year.

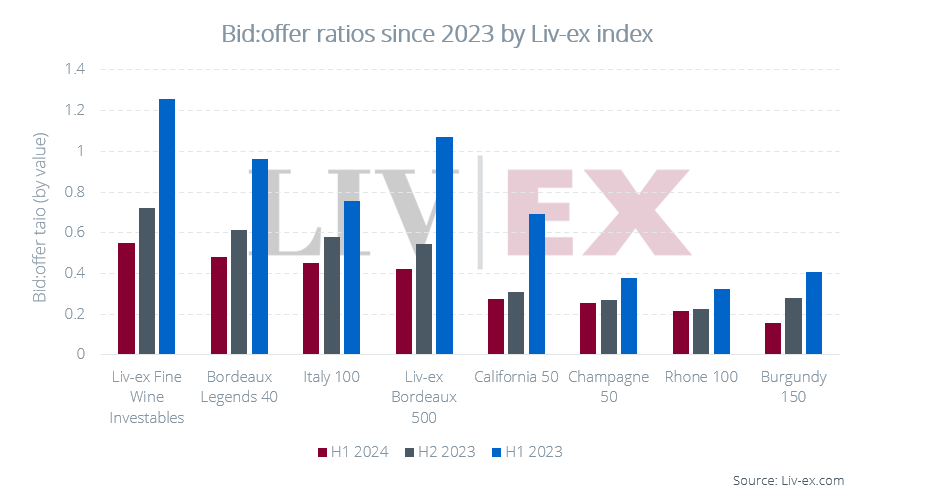

H1 bid exposure

Across the board of Liv-ex’s major indices, bid:offer ratios are low, and have fallen significantly since H1 2023. However, while ratios fell sharply over 2023, the downward trend during H1 2024 was much more subtle. Considering bid:offer ratios as a measure of market sentiment, we may infer that, though confidence levels are low, they may be finding their floor.

Ratios for the Rhone 100, California 50 and Champagne 50, for example, all remain fairly flat on the last half of 2023. While all are under 0.3 – an indication that the current bearish trend is holding strong – the stagnation of the bid:offer ratios tells us that sentiment in these markets is only marginally worse than it was during H2 2023. In a market like today’s, this is an encouraging sign.

The Liv-ex Fine Wine Investables is the only index currently with a bid:offer ratio above 0.5. A ratio sustained above this threshold tends to signal strength, or at least stability in the medium run. The index is composed of several vintages of each of Bordeaux’s top wines, including the First Growths and several high-value Right Banks. True to its name, it appears the index’s constituent wines provide buyers with a reasonable level of confidence, even during market downturns. Unsurprisingly, the five First Growths and Petrus compose the top six wines by bid exposure on the exchange overall.

The Burgundy 150 has the lowest ratio, currently sitting at 0.16. As we recently reported in a Market Update, a low ratio may present buyers with opportunities, particularly when changes in the bid:offer are driven more by an increase in offers than a decrease in bids. Since June 2022, offer exposure for Burgundy has increased dramatically, while bids have seen a relatively milder decrease. Amongst the top six wines by offer exposure on the exchange in H1 2024 are three cuvées from Domaine de la Romanee Conti and Domaine Leroy’s Musigny Grand Cru.

Conclusion

So where does this leave the fine wine market for the second half of 2024? Within the wider context of continued geopolitical insecurity, including a fractious US presidential campaign reaching its conclusion, it remains to be seen whether any of the green shoots that have momentarily sprouted during H1 will start to put down firmer roots. With trade volumes almost flat on H2 2023, we can take heart that buyers haven’t lost faith in the market. Still, prices are likely to remain uncertain as investors tentatively feel their way for these pockets of relative safety.

The recent rumblings on La Place seem set to continue, with certain players putting their heads above the parapet to call for systemic change. In this context it will be interesting to follow September’s Beyond Bordeaux releases, into which the likes of Ernst Loosen and Schloss Johannisberg have recently announced they will be launching new wines. Despite the 2023 En Primeur campaign generally falling flat, the region’s position as the barometer of the fine wine market remains intact.

About the Liv-ex indices

Our indices track the prices of the most traded fine wines on the world’s most active and liquid marketplace; Liv-ex.

They are calculated using our Mid Price; the mid-point between the highest live bid and lowest live offer on the market. These are firm commitments to buy and sell at that price; transactional data rather than list prices. It represents the actual trading activity of 620+ of the world’s leading fine wine merchants. Because Liv-ex does not itself trade, this data is truly independent and reliable.

Stretching back over 20 years, the Liv-ex 100 is quoted on Bloomberg and Reuters screens.

About Liv-ex

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines. Independent data, direct from the market.

Share this article | Print this article