Bordeaux 2023 – A small step in the right direction

Share this article | Print this article

- Bordeaux faced an uphill battle this year. A very difficult market, off 13.4% since the release of the 2022’s, and waning engagement amongst En Primeur regulars, made for a challenging backdrop.

- While vintage quality was variable across the region, commenters broadly agree that Bordeaux 2023 was a middling year overall.

- On average, release prices were 22.5% lower than for the previous vintage. Ranging from 41.1% decreases, or a little as 6%.

- While some Chateaux priced their wine attractively compared to the vintages available on the market – others missed the mark, pushing collectors into the arms of back vintages.

- Unlike in previous campaigns, there were no significant efforts by the chateau to tie offers together – requiring purchases of one less attractive wine to secure an allocation of something more sought after.

Introduction

The 2023 En Primeur campaign was never going to be easy. This year, Chateaux were tasked with releasing a good – but not great – vintage into one of the most challenging markets in over a decade. In many parts of the world, growth is slow, inflation is high, and sentiment is cautious. The fine wine market is no healthier. As our pre-En Primeur report, In the Balance, explained, the market for top Bordeaux has been drifting for the past two years. Supply has outpaced demand on the secondary market, and prices continue to fall.

On top of this, the En Primeur system has suffered from many self-inflicted wounds. In recent years, release prices have been unsustainably high. Too often, buyers are seeing wines enter the physical market below or equal to their En Primeur release prices. The large new cellars sprouting up in Bordeaux act as a visible reminder of stock building in the region for a later sale. This has collectively eroded confidence and interest in En Primeur across the supply chain.

In this context, buyers needed very good reasons to consider purchasing this year. But would the chateaux provide these reasons? Before the campaign, we questioned how many producers really remain committed to selling wine En Primeur. In recent campaigns, there are many examples of wines that have not been priced to sell through. Often, when prices have been attractive, volumes are limited. Instead, many producers have ambitions of selling stock later at higher prices.

Overall price drops for the 2023 vintage suggest some level of commitment to En Primeur. They represent a small step towards a healthier system, but slow sales this year equally suggest that the cuts did not go far enough.

Quality: A Middling Vintage

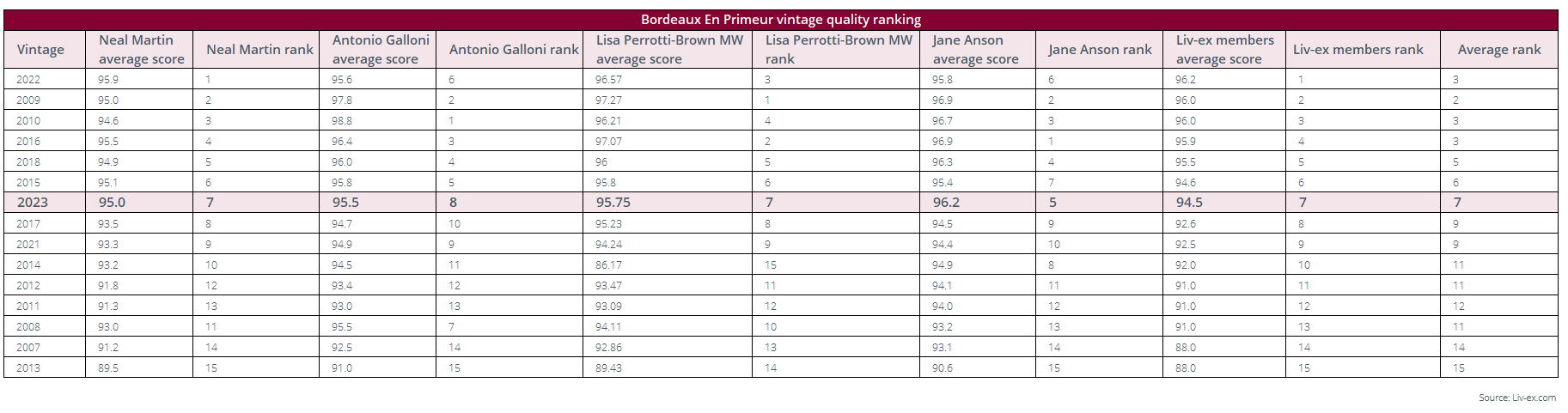

Commentors broadly agree that Bordeaux 2023 was a middling year overall. After the En Primeur tastings, Liv-ex surveyed its merchant members – the largest pool of professional fine wine traders in the world – to take a temperature check on vintage quality. Respondents scored it an average of 94.5 points. This positions it as the seventh best of 15 recent vintages that they’ve rated (2019 and 2021 are omitted – there were no surveys for these vintages due to the global pandemic).

*Click to enlarge.

*Average scores are taken from the Bordeaux 500 Index components. Liv-ex members were asked to give an overall score to the vintage in our annual survey.

The four critics shown above – Neal Martin (Vinous), Antonio Galloni (Vinous), Lisa Perrotti-Brown MW (The Wine Independent), and Jane Anson (JaneAnson.com) all awarded slightly higher scores on average compared to Liv-ex members, but they each position 2023 somewhere in the middle of recent years. Both Martin and Perrotti-Brown are aligned in ranking it seventh. Anson rates it slightly higher, while Galloni puts it in eighth place.

This offers a useful overall picture, but the reality was more complicated, with quality variable across the region. In his report, Martin declared 2023 “The Dalmatian Vintage”. He explained: “Spots of astounding quality are scattered from Bordeaux’s head to toe. Outside those spots, then there are all manner of shortcomings, including some of its more famous names. Nobody will deny that, unlike 2022, 2023 is a heterogeneous vintage.”

This, he went on, precludes 2023 from being considered a great vintage, meaning it can’t really be considered as a peer of 2016, 2020, and 2022. Despite this, he wrote, some producers “pulled out magical wines from their top hat”.

Generous Yields

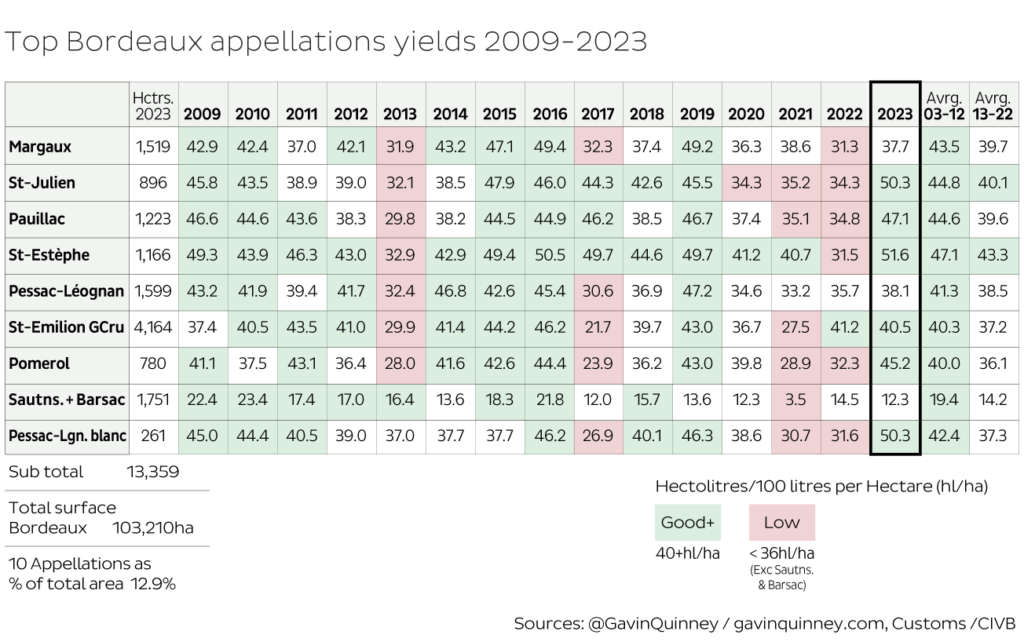

The question of yields is similarly nuanced. As grower, winemaker and writer Gavin Quinney wrote in a recent report, Bordeaux saw a relatively small overall crop in 2023. The region produced a total of 384m liters, a touch below the previous year’s 411m liters, and well below the 2011-2020 average of 487m liters. But 2023’s low figure reflects a difficult year for Bordeaux’s generic appellations. The most prestigious appellations – those that are the focus of the En Primeur campaign – instead benefitted from a generous crop. Communes such as Pauillac saw yields increase by over 30% on the previous year. With more wine to sell, producers appeared well positioned to absorb all-important price cuts.

Pricing: Shifting Lower

During En Primeur week, many producers that Liv-ex spoke to were open to engaging in conversations about the difficult state of the market. They seemed receptive to the idea of making price cuts. Overall, they followed through. Prices have, indeed, been reduced on last year. Release prices were 22.5% lower than for the previous vintage on average.

Often during En Primeur, the smallest price rises (or largest price drops) happen during the earliest stages of the campaign. Then, as time goes on, prices creep higher. This year, it was a tale of two halves. Leoville Las Cases released early with a large price drop – then price declines become very slightly smaller before the campaign went on a brief hiatus while the trade focused on Vinexpo Hong Kong. After the pause, the strategy seemed to change – lower prices, lower volume. Respected estates such as Pichon Lalande, Palmer and Montrose reportedly released 20-30% less wine so as not to flood the market.

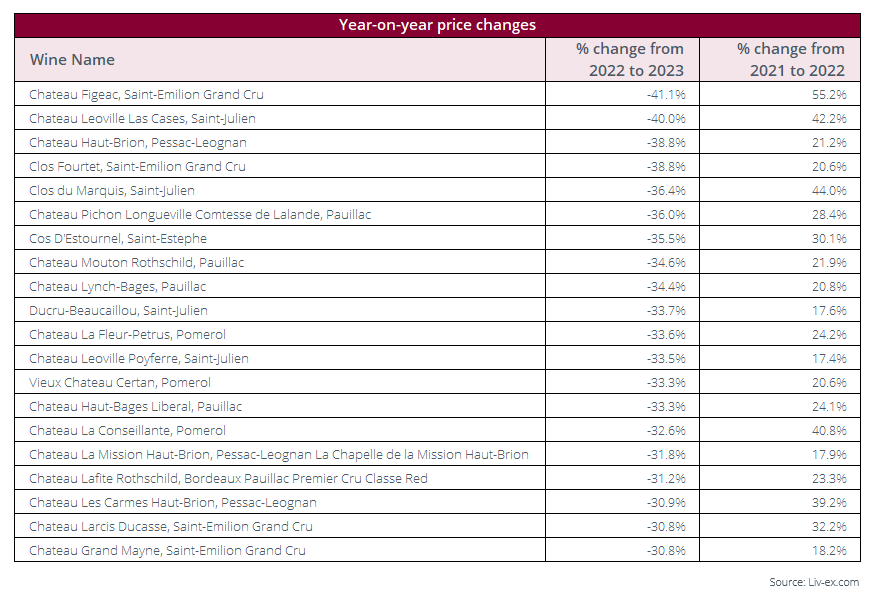

Prices have dropped by as much as 41.1%, in the case of Figeac or as little as 6% in the case of Pape Clement. If the vintage quality resembles a spotty dalmatian, so too do the price changes.

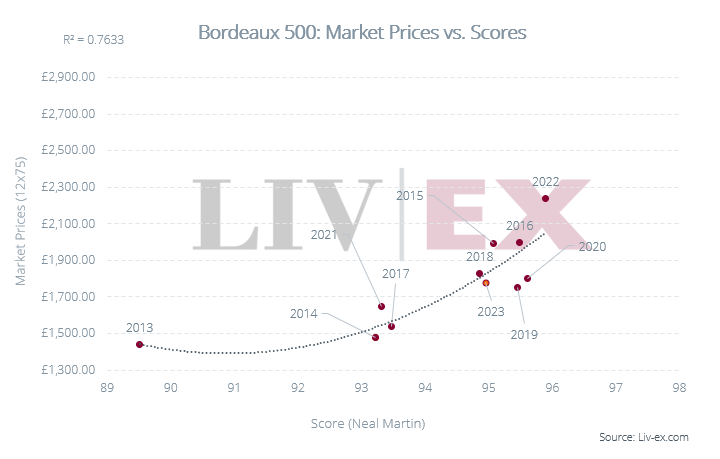

Further, while an overall 22.5% drop on last year might sound like a large concession, it bears remembering that the 2022 vintage was widely considered to have been overpriced by a large margin. Before the 2022 campaign, Liv-ex members predicted a 7% price rise – in reality, the average price increase was 20.8% compared to 2021. On top of this, fine wine prices have dropped since last year. The Bordeaux 500 Index, which tracks the prices of 50 leading Chateaux – is down 13.4% since May 2023.

Another way of looking at this year’s release prices is to compare them to vintages currently available in the market. On average, 2023 release prices were in line with (+2.8%) the average current* prices of the previous ten vintages. When last year’s overpricing and recent market conditions are considered, this year’s price drops are negated overall.

*Data taken on 14.06.2024.

Highs and Lows

High points (low prices)

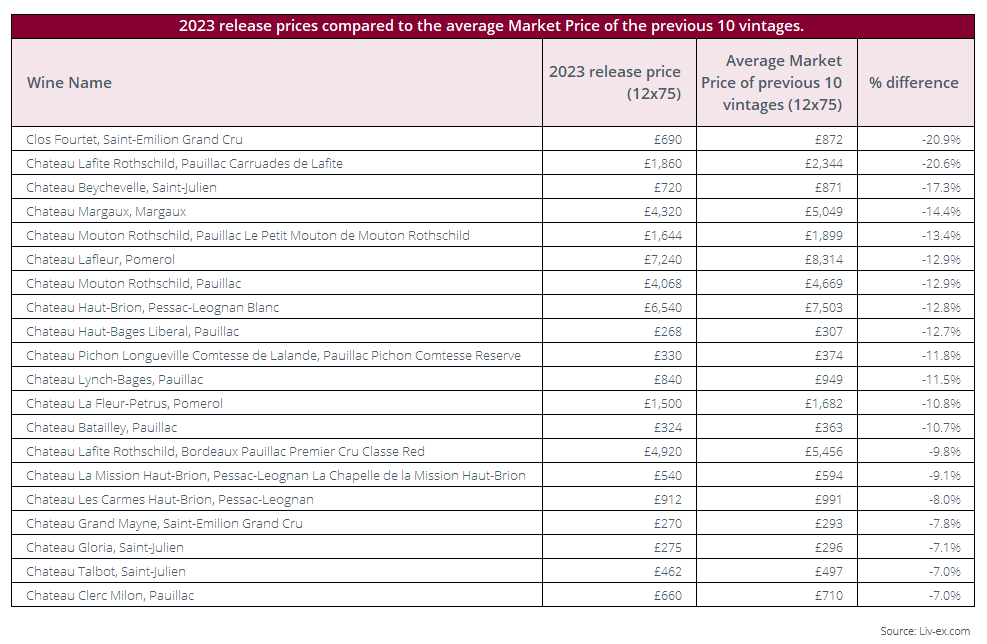

As always, some producers provide more compelling offers than others. In our opening report, we highlighted the small number of Chateaux that have consistently offered positive returns to En Primeur buyers in recent vintages. These included Lafite Rothschild (including Carruades), Beychevelle and Calon Segur.

The chart below shows which Chateaux priced their 2023 release most attractively relative to the current prices of other recent vintages in the market. That the same names crop up again in this table suggest a handful of producers committed to offering value at En Primeur.

Another hit for 2023 was Pontet-Canet. It was offered by the trade for £790 per 12×75. This represented a 26.9% decrease on the 2022’s opening price but no discount (+9.9%) to the average price of other vintages in the market. Despite this, many merchants were happy to back this release, pointing to its high critic scores which were in line with, or in some cases higher than, scores for the First Growths.

Several members reported healthy sales for Pontet-Canet. One large UK merchant said that they sold twice as many cases as last year, though they added that “this is because we are a merchant and not an investment hub!” This illustrates that with a strong brand story, producers can find relative success at En Primeur with prices that are fair, even if they are not positioned low enough for investment.

Low points (high prices)

Several wines were released into the market above current prices of back vintages. Cos d’Estournel offers an interesting illustration of how price cuts last year provide insufficient context for whether a release offers good value. The chateau dropped its price by 35% on 2022 – one of the biggest cuts of the whole campaign. However, this followed a price increase of 29% last year that pitched the 2022 well above all other recent vintages. This year’s decrease brought prices back down to earth but remained 11% above other recent vintages on average. This made it a challenging sell.

A Buyer’s Market

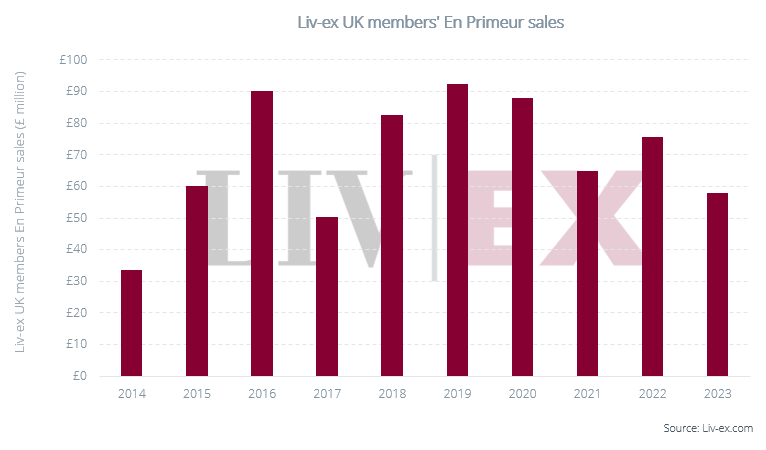

One underlying dynamic of this year’s campaign was the sense that we are firmly in a buyer’s market for Bordeaux. This was explored in our opening report, where we showed how there is more than three times as much Bordeaux for sale than the fine wine market is looking to absorb.

This sentiment has extended to En Primeur. Unlike in previous campaigns, there were no significant efforts by the chateau to tie offers together – requiring purchases of one less attractive wine to secure an allocation of something more sought after. Producers likely lacked leverage to apply this strategy this year due to low overall demand.

Similarly, no producers have offered wine in tranches this year. This is where an initially low-priced offer is used to test the market, before second and third releases come out at higher prices. This may be due to the simple fact that almost no wines have sold out. Even wines that have been considered relatively successful, such as Pontet-Canet and Lafite Rothschild, remain available for purchase at opening prices through most merchants.

Negociants, in a bid to move cases, have reportedly been offering discounts of up to 10% on some high-priced releases. One merchant that Liv-ex surveyed described a 5% discount as “industry standard these days”.

This has all contributed to an overall sense of an “open bar” for buyers who are free to cherry-pick the best opportunities at their leisure. En Primeur too has become a buyer’s market.

Disengaged Consumers

In our opening report, we warned that overpricing could cause the international trade to disengage further from En Primeur. This year En Primeur week was well attended, and many merchants, particularly in traditional European markets such as the UK and Switzerland, have worked to support the campaign.

This has been challenging. Many UK sellers of En Primeur, as well as the negociants themselves, expect sales to be down 25% on 2022, which was also a slow campaign. One UK merchant commented that “the numbers are way down” and that its efforts to energize consumers fell flat: email open rates dropped 20% from the beginning of the campaign.

While some collectors are not price sensitive and will continue to buy out of habit, there is a sense that others have switched off from En Primeur. Too many traditional buyers are getting used to the idea that it does not offer value, having been stung in recent years when wine became available in the market at more attractive prices later. These regular buyers also have large cellars of undrunk wine.

For new, often young, and tech-savvy collectors who are aware of pricing issues and are more open to buying fine wine from a wide range of global regions, En Primeur lacks a strong value proposition. Bordeaux cannot assume that it will occupy a large share of their cellars by default as it did for previous generations.

This is frustrating for merchants who have dedicated significant resources to the campaign. As one put it: “En Primeur is sucking up all the oxygen but still selling less than 2022.”

Conclusion

Bordeaux faced an uphill battle this year. A very difficult market, off 13.4% since the release of the 2022’s, and waning engagement amongst En Primeur regulars, made for a challenging backdrop. Producers were fully aware of this when En Primeur kicked off. They needed to cut prices and cut them hard. Happily, yield increases presented them with the opportunity to do just that. But they did not go far enough.

Our opening report questioned the overall level of commitment to En Primeur among the chateaux, several of whom now prefer to release wine at (hopefully) higher prices when in bottle. The price cuts throughout the campaign indicated a general willingness – if not unbridled enthusiasm – to continue with a system that has served Bordeaux so well over the years. In response, merchants in traditional markets did their utmost to support the campaign. In some cases, where strong brands were accompanied by attractive prices, sales were good. But far too often, prices made little sense and the releases flopped. The campaign became narrower still.

And so, the challenges grow. Stock levels continue to rise at the chateaux, at the negociants (despite many refusing allocations this year) and, perhaps most importantly, in collectors’ cellars. Traditional Bordeaux buyers are ageing and, in many cases, have enough wine to see them through. The next generation has more choice than ever from across the wine growing regions of the world and are less inclined to hold wine for the medium to long term. Recent poor returns and the rise in the cost of capital have given them plenty of reason to sit back.

This year’s price reductions represented an olive branch to those who have supported Bordeaux over the years but who have increasingly reaped little reward. While the price cuts were a step in the right direction, what the market needed was a leap. For En Primeur to be sustained, a new committed collector base will need to be found – and that might well require a price reset. All eyes turn to Bordeaux 2024.