What’s happening in the market?

Bordeaux started the week with 39.9% of trade share by value, with multiple 2021s, including Château Lafite Rothschild Premier Cru Classe and Le Pin finding buyers. Blue-chip back vintages also buoyed the region with notable trades of Château Cheval Blanc 1998, Château Haut-Brion 2000 and Château Latour 2003.

Champagne has taken 9.7% of trade by value so far this week, led by Dom Perignon, P2, 2003. The 2008 vintage also proved popular, specifically Krug Vintage Brut, Louis Roederer, Cristal and Taittinger, Comtes de Champagne Blanc de Blancs.

Today’s deep dive: Relative stability in white Burgundy

As we highlighted in a recent market update, 18 months into the market downturn it is obvious that Burgundy is one of the regions feeling the price correction the hardest.

However, white Burgundy has remained relatively unaffected by this trend.

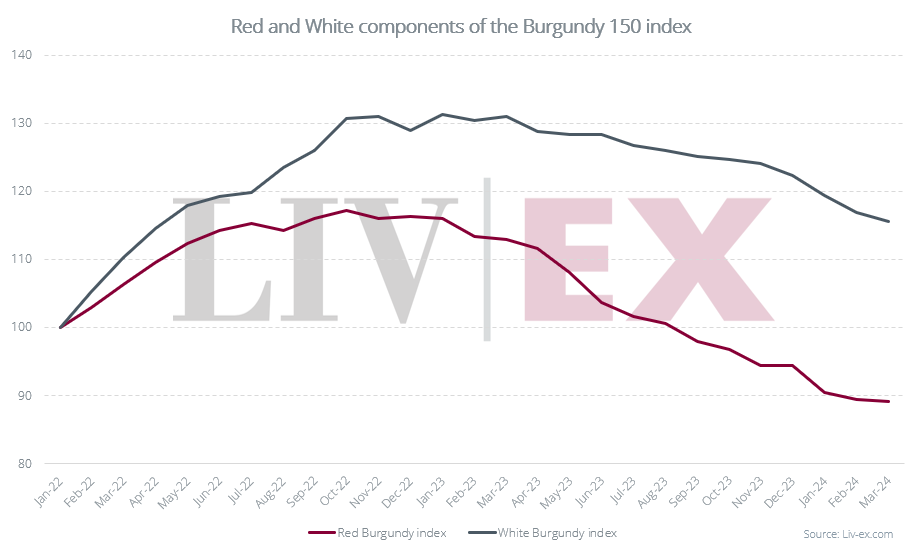

Yesterday, we noted that out of the top-traded Burgundian wines by value, three of the top five were white wines. In fact, since 2022 the white components of the Burgundy 150 index have outperformed both the index as a whole and its red components.

White Burgundy wines are cheaper on average than their red counterparts (with a few exceptions), but the former’s price performance has also been much stronger. This is in part because white wines are primarily earlier drinking wines, which means stock reduces relatively quickly upon their release, keeping prices stable.

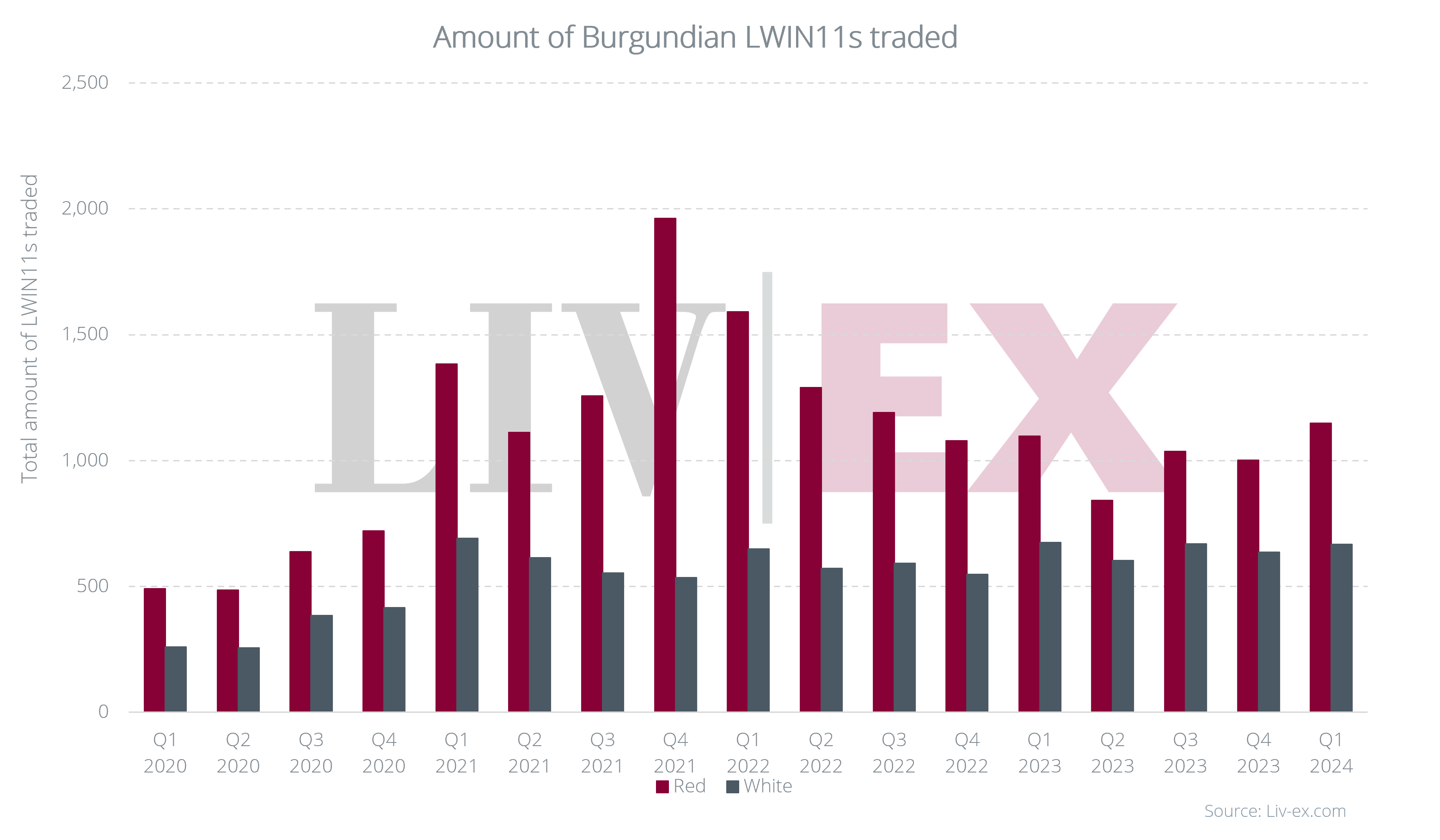

The graph below shows, how as prices of red Burgundy wines soared in the run up to the peak of the market, the number of individual labels (LWIN11s) almost doubled. The rise in global demand led to a broadening of the market as buyers searched for value, as well as stock, in ‘new’ labels from the region – think of the rise in popularity for producers such as Arnoux-Lachaux. Since the market turned down and the speculation bubble popped, the number of distinct labels traded has fallen.

In comparison, the number of individual white Burgundy LWIN11s traded has remained stable since 2020 as trade has concentrated around a group of unwavering brands.

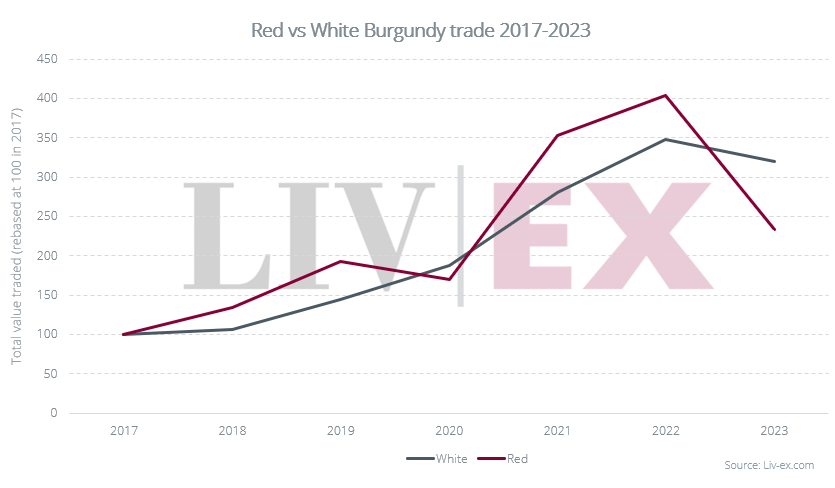

The growth of Burgundy’s trade since 2017 can be seen in the chart below. The value of red Burgundy trade dropped 42.3% from 2022 to 2023, while white Burgundy dipped by just 8.2%.

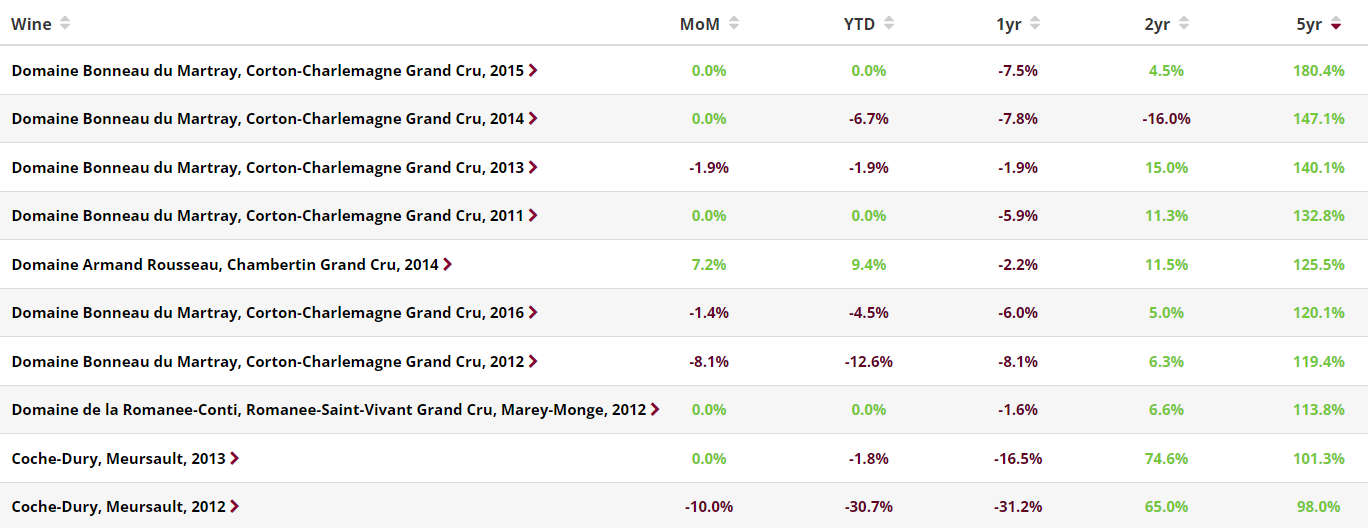

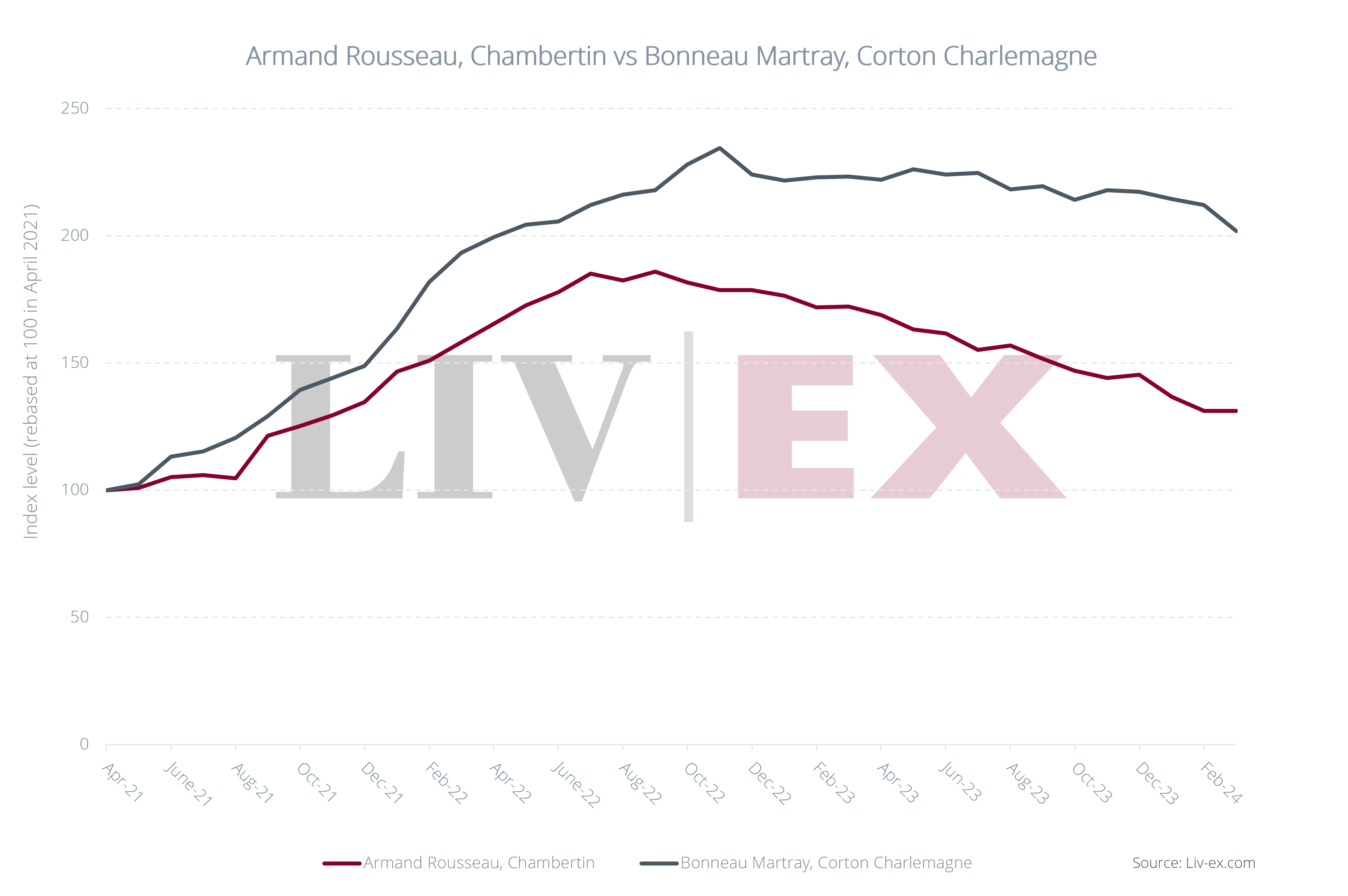

Looking at the components of the Burgundy 150 index over the last five years, Domaine Bonneau du Martray, Corton-Charlemagne Grand Cru has four of the top price performers: 2015 (+180.4%), 2014 (+147.1%), 2013 (140.1%) and the 2011 (+132.8%). While Armand Rousseau Chambertin Grand Cru 2014 occupies fifth place.

The chart above illustrates Bonneau Martray’s stability, only dropping 13.9% since the peak of the market, compared to a 29.4% decline for Rousseau.

There are currently over 3,522 LIVE white Burgundy offers on Liv-ex. Log in to your exchange to view them.

In case you missed it

Here’s what we’ve been reading:

- Liv-ex – April Market Report

- The Economist – Where are all the British robots?

- Decanter – No room for Bordeaux en primeur price rises, says report