November Market Report

Share this article | Print this article

- All major Liv-ex indices fell last month.

- The Rest of the World 60 rose by 0.2% again, buoyed by Californian wines.

- The Wine Spectator’s Wines of the Year are having their usual impact on the market, causing a flurry of trading activity surrounding the selected wines.

- Technical analysis of the Champagne 50 finds that its long-term bullish trend is still intact.

- Ten years on, we looked at the 2013 Burgundies rescored by Neal Martin.

- And finally, we explored how trade prices fare in a downward market.

Introduction

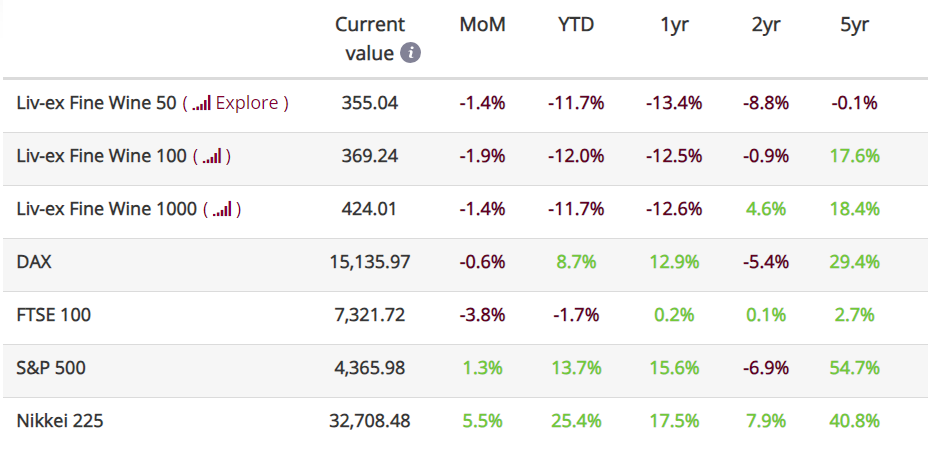

*data taken on the 7th of November 2023. The FTSE 100 was last updated on the 31st of October. The Liv-ex Fine Wine 50 is updated daily.

In September, the market briefly paused its decline as merchants returned from summer holidays. However, the downward trend resumed in October, with the Liv-ex Fine Wine 100, the industry benchmark, dropping by 1.9% to close at 369.24. The Liv-ex Fine Wine 50, which tracks First Growths, also fell by 1.4% month-on-month (note: this index is updated daily).

Looking at the broader fine wine market, the Liv-ex Fine Wine 1000 dropped by 1.4% in October, surpassing the 1.0% fall the month before. Year-to-date, the index has fallen by 11.7%. These movements contrast with other financial indices which recorded gains in October, such as the S&P 500 (+1.3%) and the Nikkei 225 (+5.5%).

With prices falling across the board, the ball is currently in the buyer’s court; wines within the Liv-ex 100 traded on average 3.1% below their Market Price in October, compared to just 1.7% below in September. Some have been making the most of this downward-trending market; trading activity increased in October, as did the number of monthly transactions on the exchange. Market breadth continued to expand steadily, with 2,243 individual labels (LWIN11s) traded on Liv-ex last month.

The market’s price correction continued, with trade value increasing in October despite general price declines (as reflected in major indices taking a hit). The indices’ individual components have shown volatility, pointing to a lack of confidence within the market. One year on from the start of the downturn, will end of year festivities and critics’ yearly roundups be enough to lift the market? We investigate.

Major Market Movers – The Rest of the World 60 continues to rise

In September, two sub-indices of the Liv-ex 1000 rose: the Italy 100 by 0.6% and the Rest of the World 60 by 0.2%. October saw the Rest of the World 60 rise by another 0.2%. The index, which contains ten of the most recent physical vintages of Vega Sicilia Unico, Seña, Screaming Eagle, Opus One, Dominus and Penfolds Grange, was largely buoyed by Californian wines.

53% of the Californian wines within the Rest of the World 60 index recorded a positive movement in October, with the top three performers within the index all hailing from the region: Screaming Eagle 2015 rose by 11.1%, Screaming Eagle 2012 by 11.0% and Dominus 2011 by 11.1%. However, it’s worth noting that these three wines have seen significant year-to-date declines in their performance.

While October saw a decrease in the volume of Californian wines traded compared to September, their trade value was the highest since March this year, pointing to a flight to quality in region. Screaming Eagle is a good example of this: the 2015 and 2012 vintages, which recorded double-digit increases last month, were both scored 100 points by The Wine Advocate. On the other hand, the wine’s lower-scoring 2017 and 2011 vintages saw their Mid-Prices decline by 8.1% and 6.2% respectively.

Liv-ex members can see price movements of individual wines in all the Liv-ex indices in-app using the Indices Explorer.

News Insight – The Wine Spectator’s top wines of the year

It’s that time of the year again – not quite Christmas, but the release of major publications’ top wines of the year rankings. So far, we have had James Suckling’s ‘Top 100 World Wines 2023 and Wine of the Year’, who gave Laurent-Perrier’s Champagne Grand Siècle Iteration N.26 the number one spot, and The Wine Enthusiast’s Top 100 Cellar Selections 2023, which named Poggio di Sotto, Brunello di Montalcino 2018 as its top recommendation.

This week, the Wine Spectator has been gradually revealing its top ten wines of the year, culminating in the announcement of the top pick later today. The publication’s full top 100 will come early next week. For the wines recognised on the list, publication day is basically Christmas: over the last few years, most of the Wine Spectator’s top wines have enjoyed significant trading activity and an uptick in price.

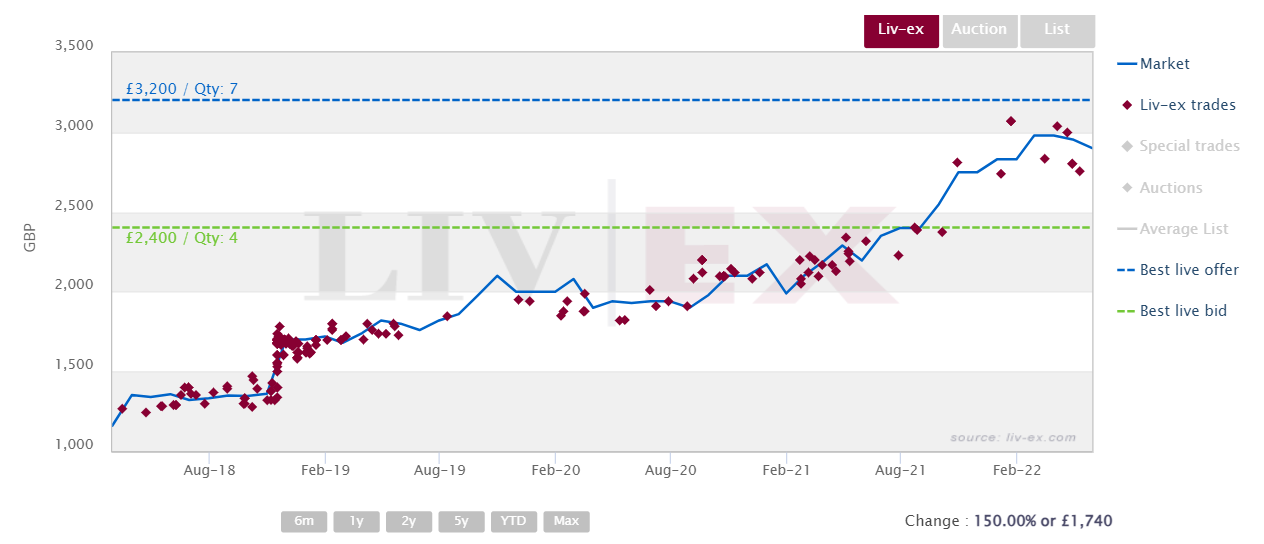

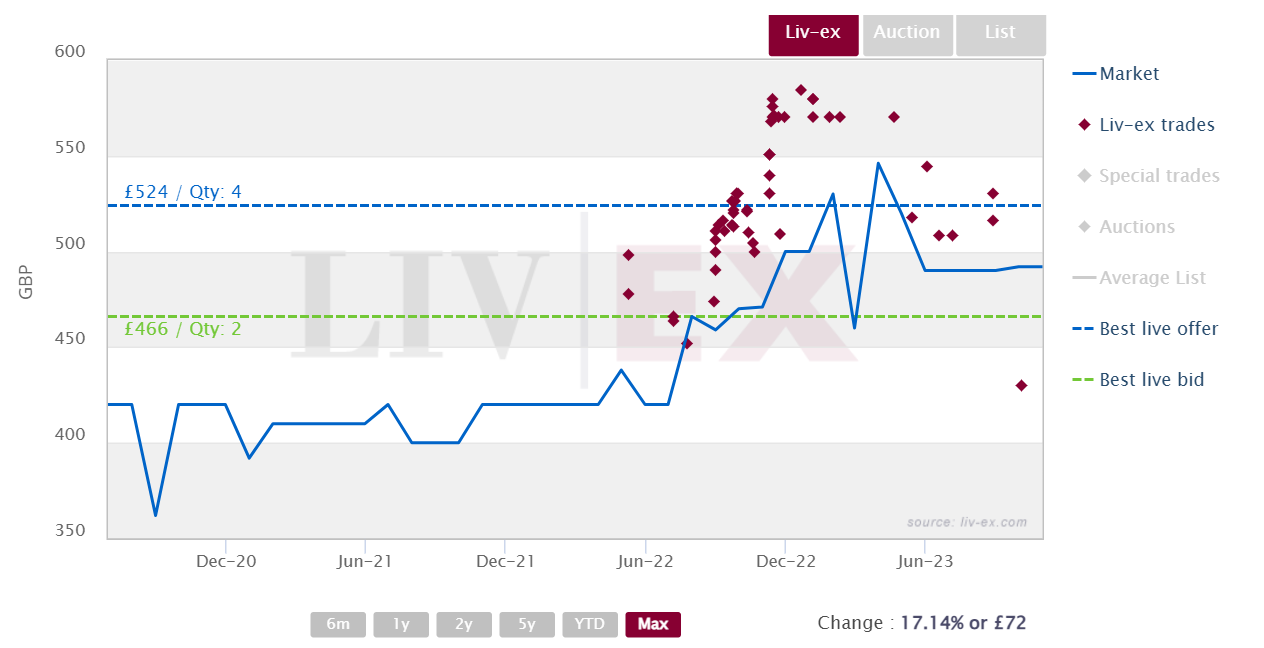

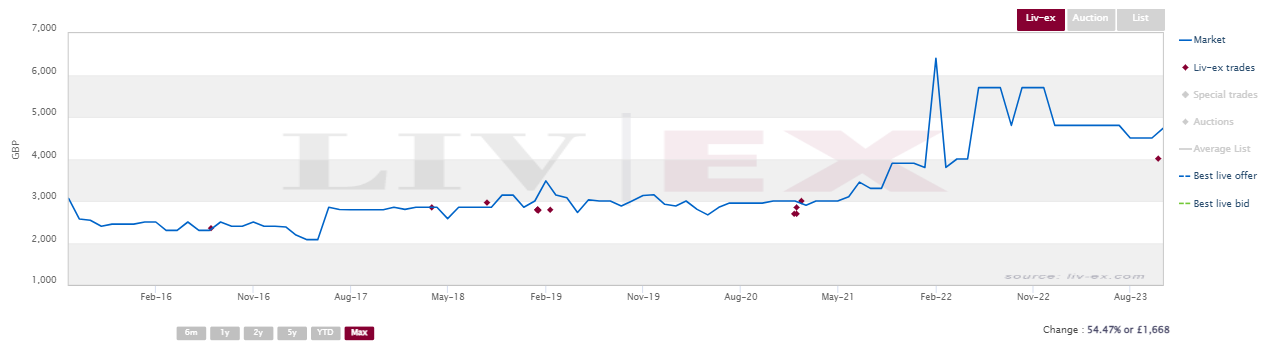

In 2018, the Wine Spectator’s wine of the year was Sassicaia 2015 with a score of 97 points and a Market Price of £1,350 per case at the time. Immediately after the announcement, the wine saw a flurry of trade on Liv-ex, as shown in the chart below. The wine has since seen its Market Price double to £2,700 per case, but it last traded at £2,400, 11.1% below Market Price.

Sassicaia 2015 trades on Liv-ex

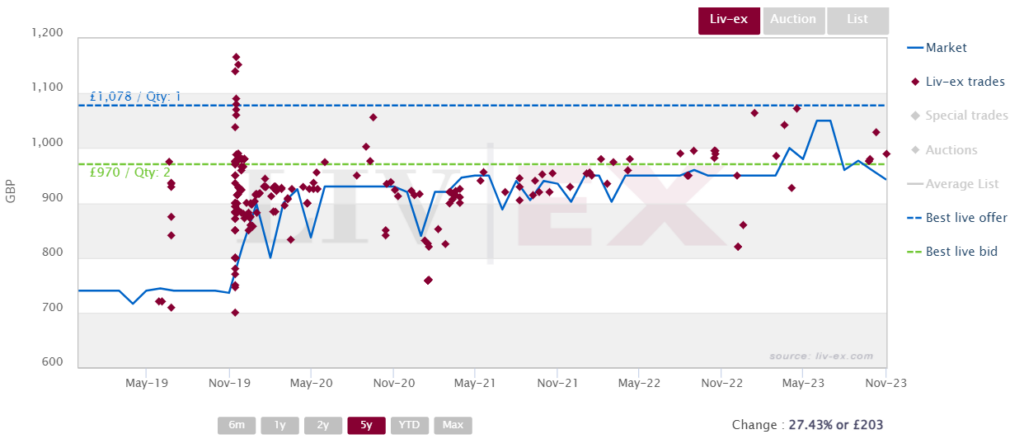

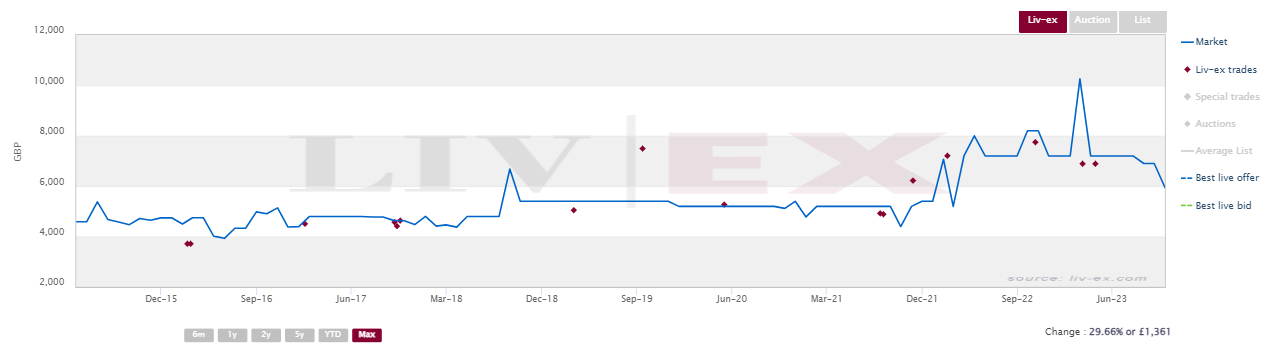

Similarly, in 2019, Château Léoville Barton 2016 was named the wine of the year and also experienced a heightened level of trade off the back of the announcement. At the time, the wine had a Market Price of around £700 per 12×75, which then jumped to roughly £900 per case. It has since further appreciated to a current Market Price of £1,020 per case, and it last changed hands at £990 per 12×75.

Château Léoville Barton 2016 trades on Liv-ex

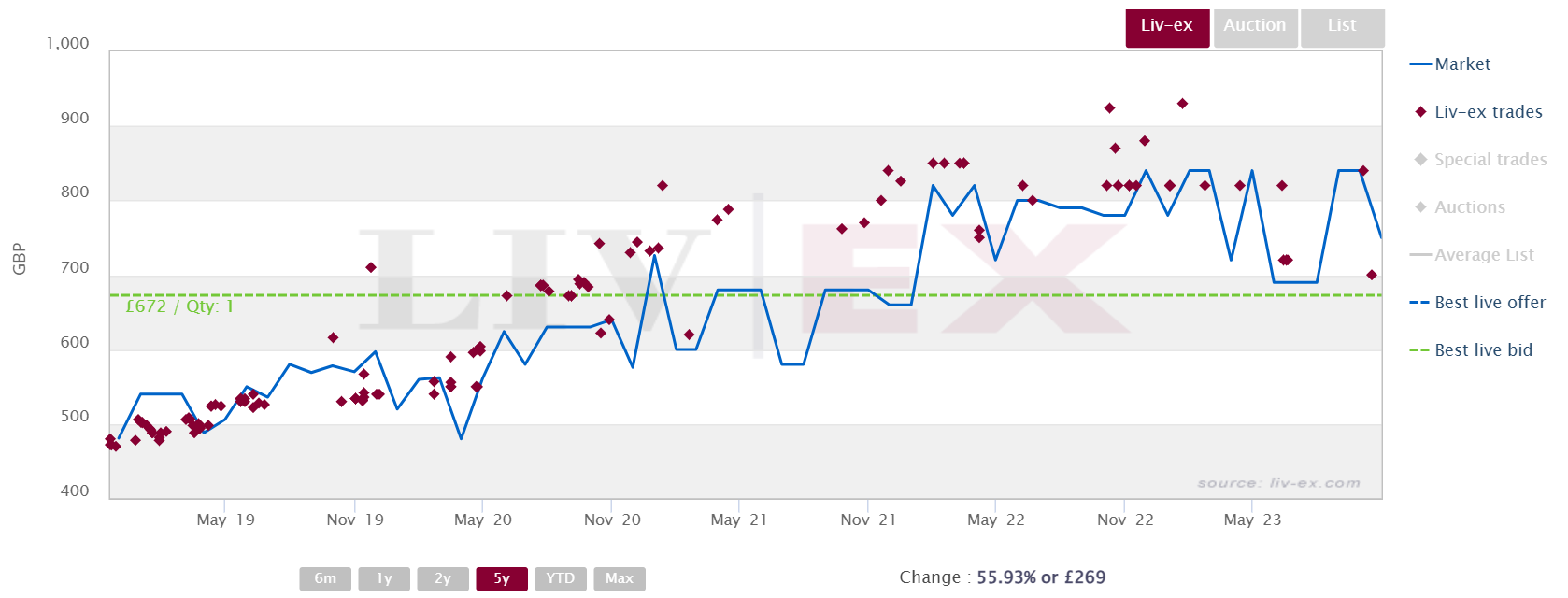

This trading spike isn’t limited to the number one spot on the Wine Spectator’s list, but also filters down to others further down the rankings. Château de Beaucastel Rouge, Châteauneuf-du-Pape 2016 was ranked sixth in 2019 and has seen a steady increase in trade price since then.

Château de Beaucastel Rouge, Châteauneuf-du-Pape 2016 trades on Liv-ex

Château Talbot 2019 was ranked number four in 2022 and set a new all-time high trade price soon after:

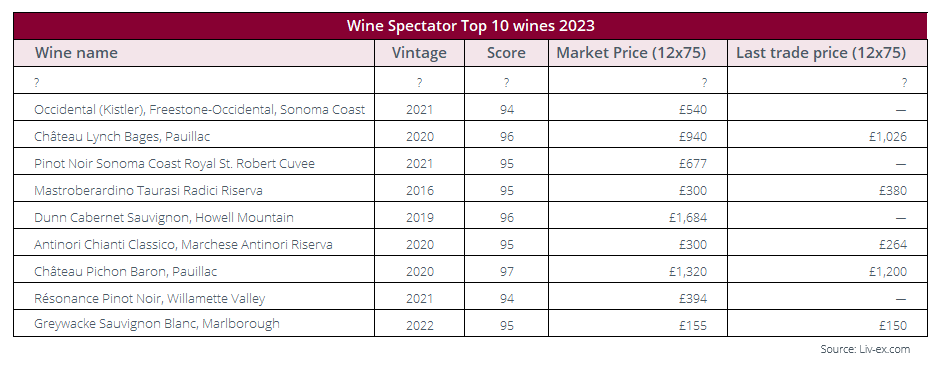

This year, the Wine Spectator has announced the below as its top wines of 2023:

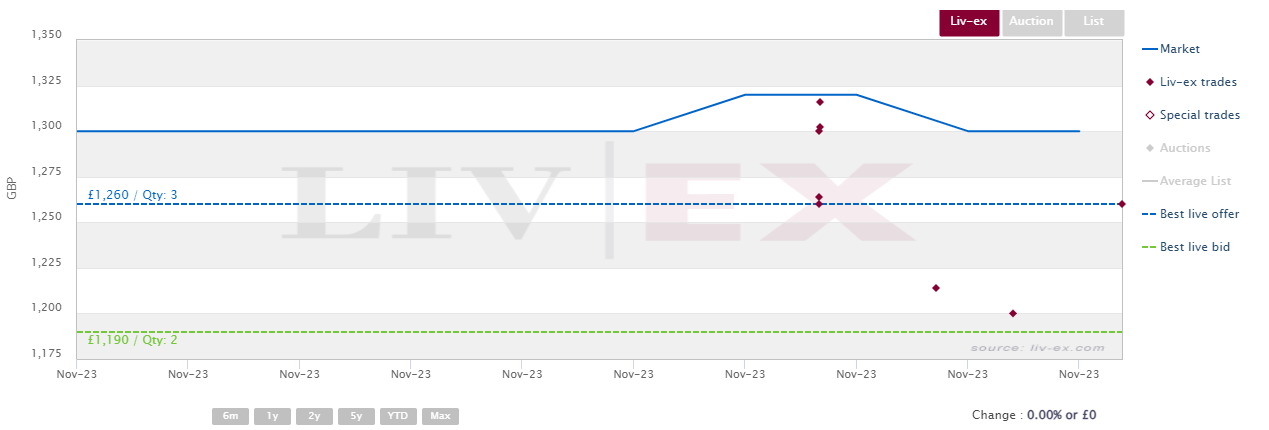

Château Pichon Baron 2020 traded 16 times since it was announced as one of the top wines of 2023, having previously not traded in two months; interestingly, the impact on its price so far has not been as positive as for previous years’ picks.

Château Pichon Baron 2020 trades on Liv-ex

We will be monitoring how the market reacts to these top wines, and whether this critical acclaim can have a significant impact on their trading activity (and crucially, on their price) despite the current downturn.

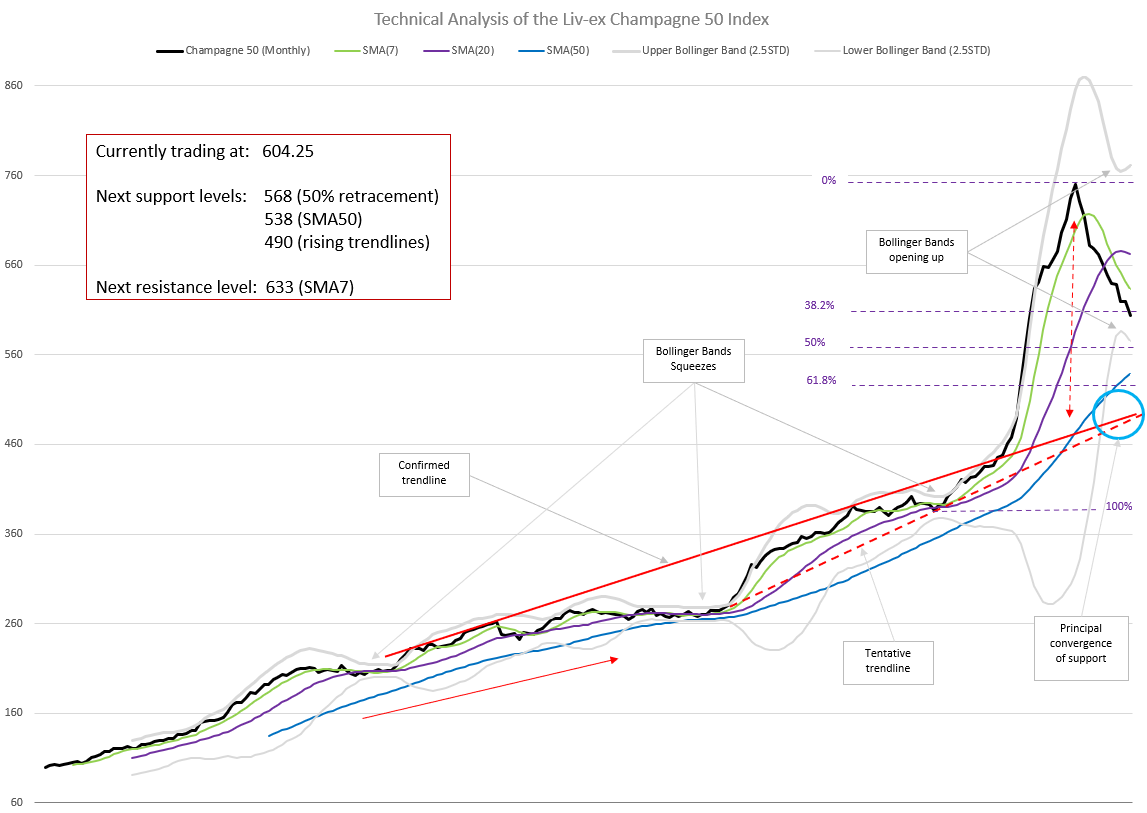

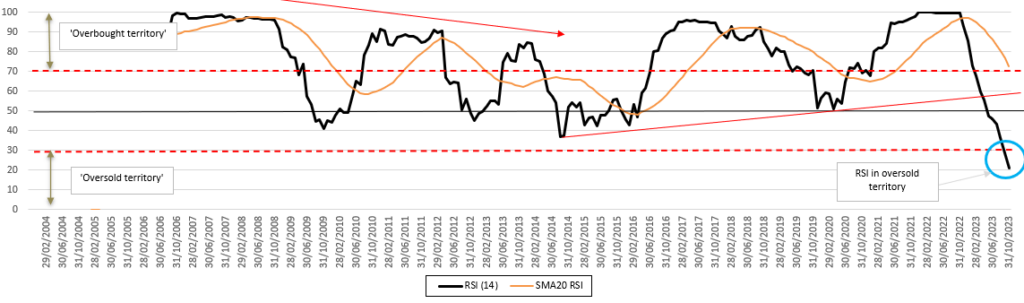

Chart of the Month – The Champagne 50’s bullish trend isn’t out of gas (yet)

The recent price action for the Liv-ex Champagne 50 index confirms the correction we have been discussing since March 2023. Can we still call a 20% drop a correction, or has the index entered a bear market?

Given the brutal move up from early 2020 (the index doubled in the last two and a half years), we would continue to view the current price retracement as a correction so long as the Simple Moving Average 50 months (SMA50, in blue in the chart above) and the rising trendlines hold. These long-term indicators signal that while the index is moving down, the bullish trend is intact.

The momentum remains clearly bearish, as evidenced by the Relative Strength Index (RSI, charted below), which broke the ’30 line’ in September (the ‘acceleration zone’ we mentioned in our August analysis) and is now deeply into oversold territory.

With the Bollinger Bands (BB, in grey on Chart 1) opening up again in September and October and little support around the current price level, bearish momentum is likely to continue. There is no technical sign that the ongoing correction is over. As mentioned back in August, the price action of the Champagne 50 since its peak in October 2022 demonstrates that a correction was indeed needed following ‘excessive’ appreciation.

Nonetheless, the long-term bullish trend will remain in place as long as:

1) the SMA50 holds as support (N.B. the SMA50 will continue to rise in the near future as it has not yet adjusted to reflect the downturn, being a long-term indicator); or

2) the price does not break the long-term trendline resistance turned support, which, fittingly, converges with rising tentative trendline at around 490.

Ahead of Christmas, let’s hope the festive cheer will be enough to keep Champagne from going flat.

Critical Corner – Are 2013 Burgundies ageing like fine wine?

Neal Martin released his Ten Years On: Burgundy 2013 report in October, in which he revisits the 2013 vintage in Burgundy, evaluating how the wines have evolved over the past decade. We looked at the evolution of the 75 white and red wines he reevaluated, identifying which ones have seen a score increase and which have been downgraded.

The wines’ scores decreased by half a point on average, with four wines being upgraded, 57 wines maintaining their previous scores and 15 wines seeing a drop.

The most noteworthy increase in score was observed in Domaine Arlaud Gevrey-Chambertin Aux Combottes Premier Cru 2013. Initially awarded 89 points by Martin in 2018, this wine has now been rescored 93 points. Martin remarked, ‘this is drinking beautifully now but should continue to give pleasure’.

Martin also rescored three other wines upwards by one point each: Château de la Tour Clos de Vougeot Vieilles Vignes Grand Cru 2013, moving from 90+ points in 2015 to 91 points; Corton-Bressandes Grand Cru 2013, moving from 91 to 92 points and Domaine Jean Grivot Echézeaux Grand Cru 2013 from 92+ points in 2016 to 93 points.

On the other hand, some wines experienced score reductions. Within the wines covered in the Burgundy 150 index, Clos de Tart, Clos de Tart Grand Cru 2013 saw its score downgraded from 93-95 points in 2014 to 91 points. While the wine saw a 1.4% increase in its Mid-Price in October, it has recorded a 7.1% year-to-date performance decline. The wine last traded at its peak price of £4,014 per case.

Clos de Tart Grand Cru 2013 trades on Liv-ex

Domaine des Lambrays, Clos des Lambrays Grand Cru 2013 also saw a decline in score, moving from 92-94 points in 2016 to 90 points. The wine last traded at £2,434 per case, slightly below its maximum trading price of £2,500 in November 2022. Its Mid-Price ran flat in October, and it is down 3.7% year-to-date.

Domaine Comte Georges de Vogüé Musigny Vieilles Vignes Grand Cru 2013‘s scoring is particularly interesting; it went from 94-96 points in 2014 to 96 points in January 2016, and 95 points in November 2016 when tasted blind. However, Martin has now rescored the wine 90 points. The wine’s Mid-Price has seen a gradual ascent from August 2021, reaching its peak trade price of £7,752 per case in October 2022 adjusting to its most recent trade price of £6,880 per case. The rescore has potential to accentuate the ongoing correction.

Domaine Comte Georges de Vogüé Musigny Vieilles Vignes Grand Cru 2013 trades on Liv-ex

Other notable downgrades include three 2013 wines from Domaine Ponsot: the Clos de la Roche Vieilles Vignes Grand Cru, which shifted from 95-97 points in 2014 to 91 points, the Corton-Charlemagne Grand Cru, which decreased from 90-92 points in 2014 to 86 points and the Chapelle-Chambertin Grand Cru, which was rescored 91 points, down from a range of 95-96 in 2014.

Describing the 2013 vintage, Neal Martin commented on the ‘very challenging growing season’, which ‘in many ways was a precursor to the infamous 2021 season’. A few months out from the 2021s being released, it will be interesting to see whether they are destined to the same fate.

Final Thought – How do trades fare during market fluctuations?

The fine wine market is currently undergoing a correction and with it, trade prices are shifting. The Liv-ex 100 and 1000 reached their peak in October and September 2022 respectively, after both indices recorded a gradual climb commencing in May 2020.

Year-to-date, the Liv-ex 1000 has retraced 11.7%, while the Liv-ex 100 index has followed closely with a 12.0% pullback during the same timeframe. As for whether this downward trend will evolve into a full bearish market, only time will tell.

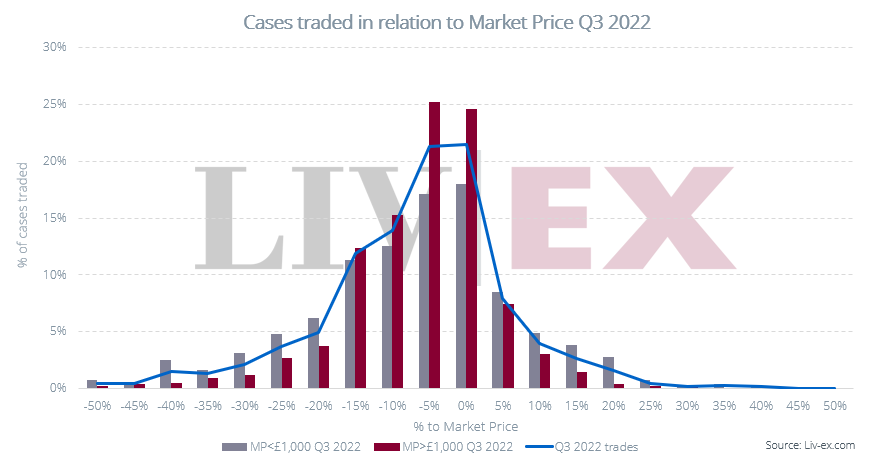

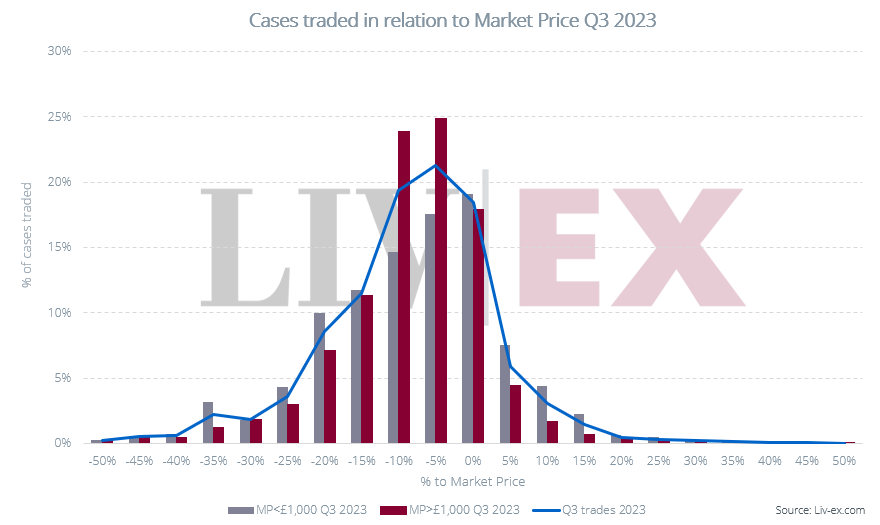

Comparing trading data from Q3 2022, a bullish period in the market and Q3 2023, which was characterised by bearish signals, reveals a noticeable shift in trade prices.

As shown in the chart below, the gap between Market Prices and the trade prices narrowed during the ascent to the peak in Q3 2022, with trades occurring on average 2.85% below the Market Price in Q1 2022. Subsequently, as prices peaked and then began to decline, this gap widened to –3.9% on average in Q3 2022, to then fall to trade prices occurring on average 4.8% below Market Price in Q3 2023.

Notably, this downward trend disproportionately impacted wines with higher price points (over £1,000 per 12×75) compared to those priced below £1,000. On average, in Q3 2022, wines priced above £1,000 per case were trading 3.7% below Market Price, which increased to 6.0% below Market Price in Q3 2023. By contrast, wines priced under £1,000 went from trading at a 4.0% discount to their Market Price on average in Q3 2022 to trading fractionally closer to Market Price (-3.4% on average) in Q3 2023.

Wines with a Market Price exceeding £10,000 fared even worse. In Q3 2022, they traded on average 3.8% below Market Price. By Q3 2023, this discount had deepened significantly to 11.7% below Market Price.

What does this tell us? In a downward market, the assumption is that collectors turn to the ‘safe bets’, making them fairly resilient to downturns. However, the data above suggests now might be a good time to place bids on Rousseau, Romanée-Conti and Pétrus, as even ambitious ones might be rewarded.