February Market Report

- The value of live offers hit a new high at £70million.

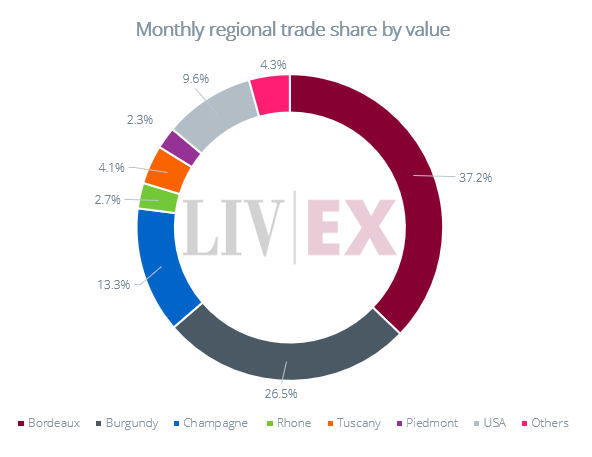

- Burgundy (26.5%) and the USA (9.6%) saw substantial increases in trade share.

- Some of the best price performers in January came from Burgundy.

- The top traded Opus One vintage, the 2019, received Lisa Perrotti-Brown MW’s highest score in her latest vertical tasting.

- La Place de Bordeaux distribution system has continued to grow in importance thanks to new labels from outside of Bordeaux.

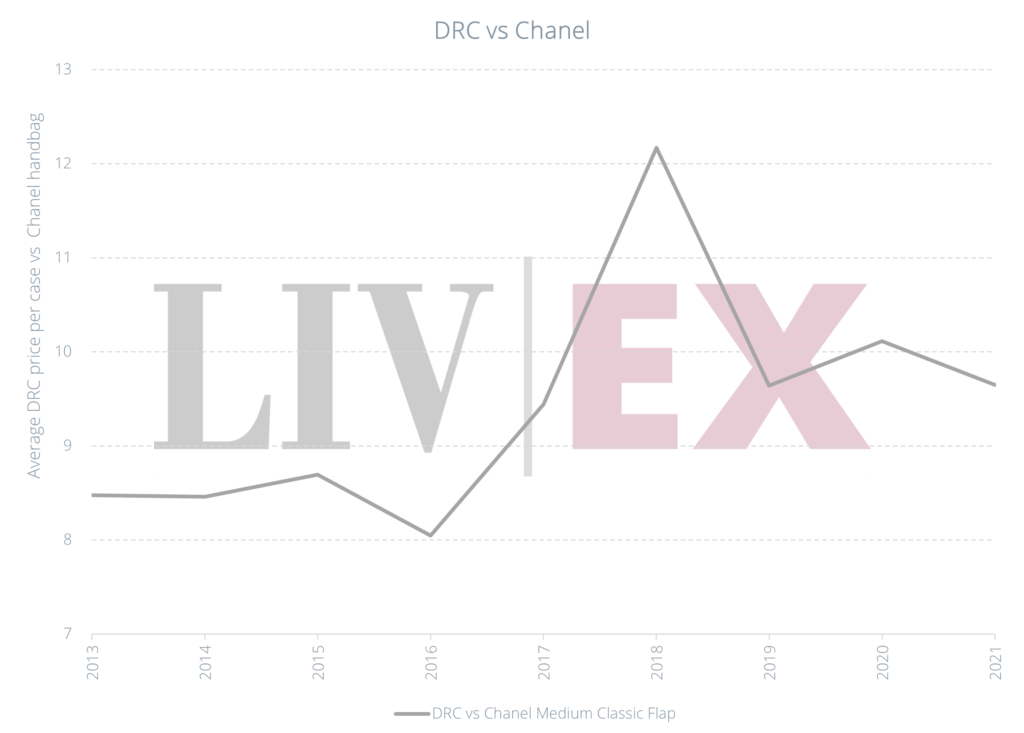

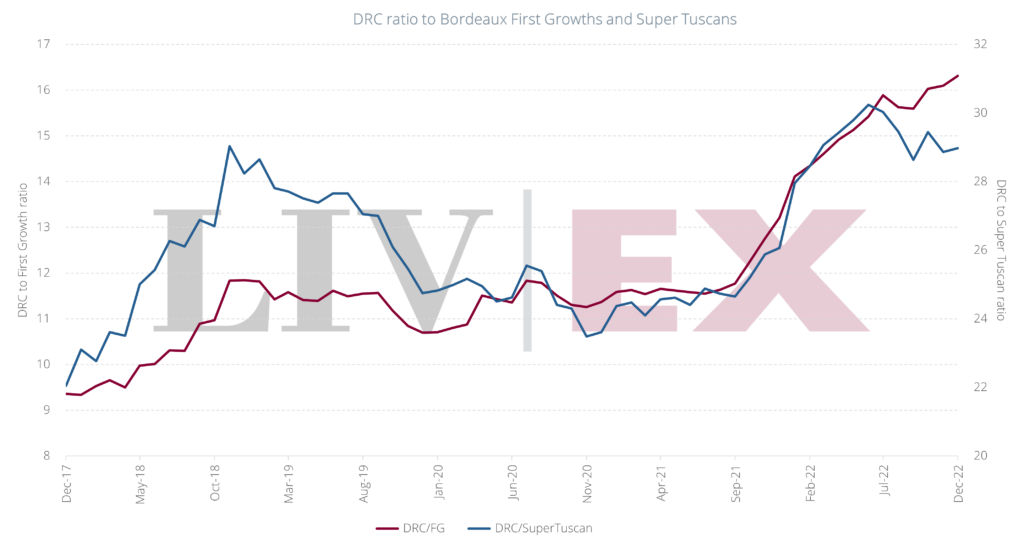

- For the same price of a case of Domaine de La Romanée-Conti, one can get 16.3 cases of First Growths, 29 cases of Super Tuscans or ten Chanel handbags.

The value of live offers hits £70million

The total value of live offers on Liv-ex hit £70million in January. The number of wines on offer also set a new record, with close to 7,000 labels (LWIN7s) and 17,000 distinct wines including vintages (LWIN11s). These numbers show the continuous broadening of the market and the diversity of fine wines now available online.

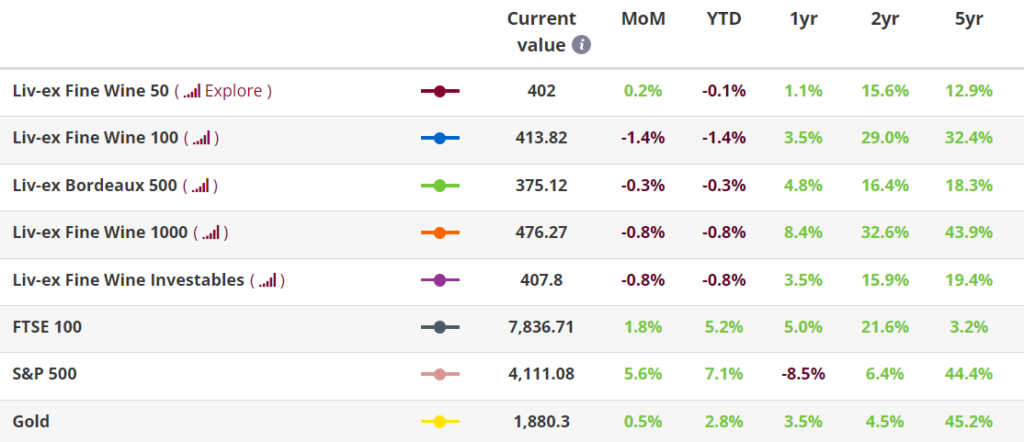

January was also a good month for mainstream markets. As fears of heightened inflation receded, the FTSE100 rose 1.8% and the S&P 500 5.6%. This was not the case for fine wine prices, however, which declined last month. The market was somewhat distracted with Chinese New Year holidays, and the launch of Burgundy’s 2021 vintage, which proved challenging in terms of prices and volumes. Buyers also expressed more general concerns about the macro-economic picture, as the results of our annual survey showed.

As a result, the industry benchmark, the Liv-ex 100 index, experienced its biggest dip since November 2015. Meanwhile, the broadest measure of the market, the Liv-ex 1000 index, fell 0.8%. For the third month in a row, the Champagne 50 sub-index was its worst performer, falling 4.3%. Of the Liv-ex 1000 sub-indices, only the Burgundy 150 managed to rise – up 0.4%.

First Growth prices did however squeeze out a small gain, up 0.2% in January. ‘Off’ vintages were the best-performing wines in the index, namely Château Mouton Rothschild 2013 (6.2%) and 2011 (2.5%), and Château Lafite Rothschild 2017 (2.6%).

Chart of the month

Strong start of the year for Burgundy and the USA

During its annual En Primeur campaign, Burgundy enjoyed increased secondary market demand. Its share of total trade by value rose from 22.8% in December to 26.5% last month. The 2020 and 2018 vintages were the most traded. The most active wine by value in January also came from Burgundy – Louis Latour Romanee-Saint-Vivant Grand Cru Les Quatre Journaux 2020.

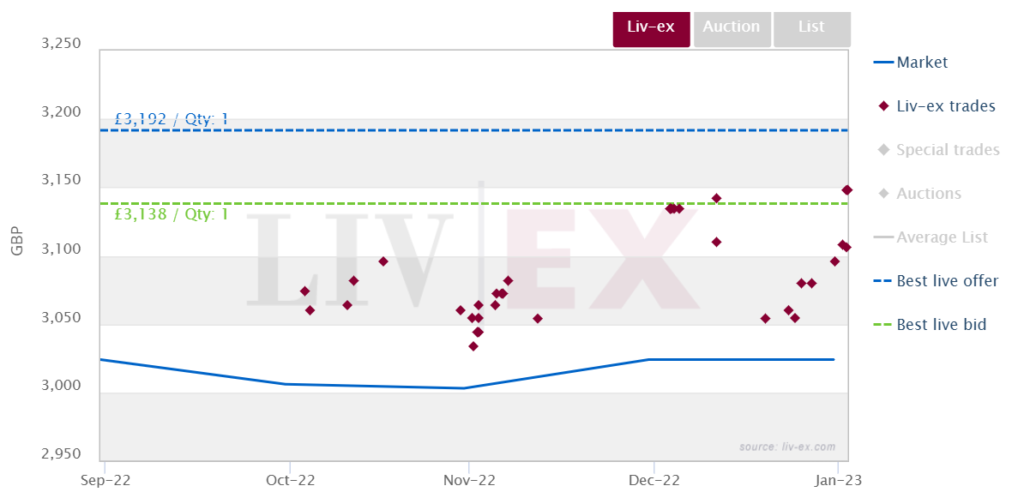

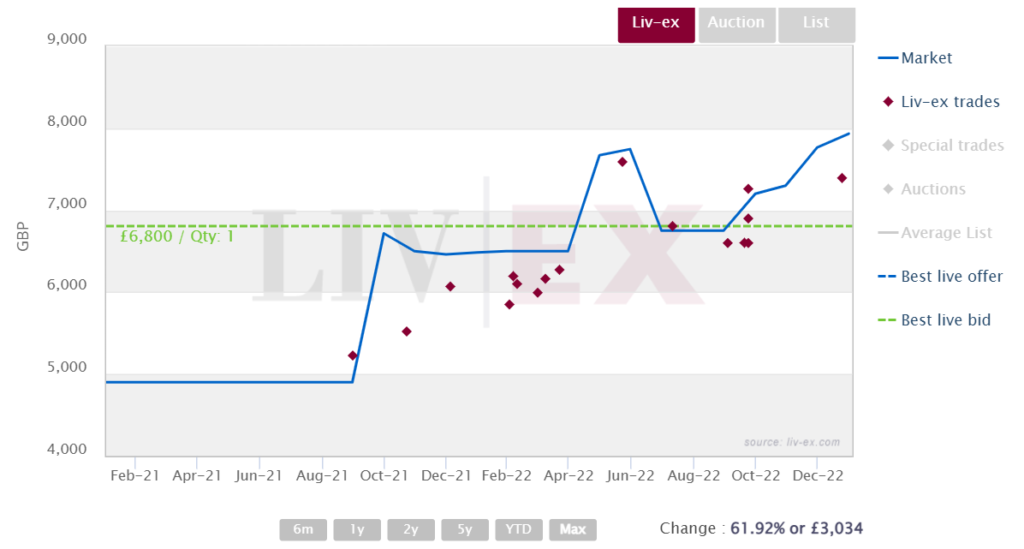

The USA continued to build its momentum, with its share rising from 7.1% to 9.6%. Screaming Eagle The Flight 2019 and Opus One 2019 led trade by value. The latter set a new trading high of £3,148 per 12×75, up 4.1% on its release price.

Opus One 2019 trades on Liv-ex

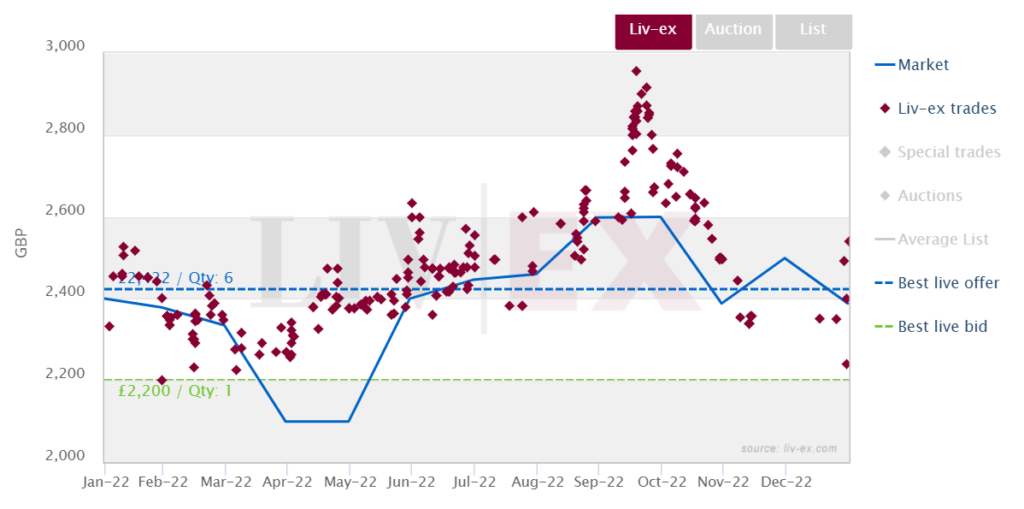

Champagne was the only other region to increase its market share in January, albeit only slightly, and on falling prices. Non-vintage Champagne accounted for 29.0% of the region’s trade, followed by the 2014 vintage, which took 17.2%.Louis Roederer Cristal 2014 led the Champagne market by value traded. However, as the chart below shows, in January the wine consistently traded at lower prices than those set in October last year, when demand for the wine was at an all-time high. A few weeks’ later, the wine was also named Wine Spectator’s #10 wine of the year.

Louis Roederer Cristal 2014 trades on Liv-ex

Major Market Movers

Burgundy leads the market in January

After two consecutive months of declines at the end of 2022, Burgundy was the one region to find some cheer

The Burgundy 150 was the only Liv-ex 1000 sub-index that rose in January, and as such, it included some of the top price performers last month. Domaine de la Romanée-Conti Echezeaux Grand Cru 2018 led the way with an increase of 13.4%. Two vintages of Coche-Dury Meursault, 2017 (13.3%) and 2013 (12.5%), also appeared in the rankings.

Joseph Drouhin Montrachet Grand Cru Marquis de Laguiche 2019 trades on Liv-ex

Critical Corner

Lisa Perrotti-Brown’s vertical tasting of Opus One

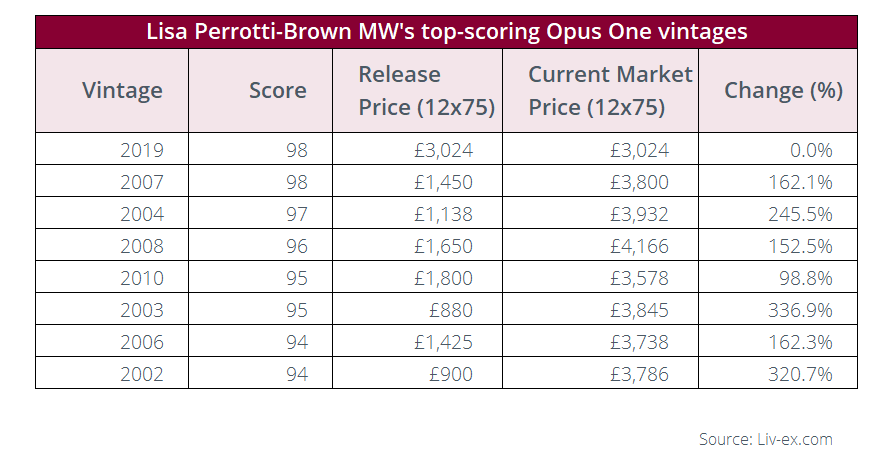

Lisa Perrotti-Brown MW (The Wine Independent) recently reviewed Opus One, the ‘iconic label’ of Bordeaux’s Baron Philippe de Rothschild and Napa’s Robert Mondavi. The vertical tasting comprised of the 2001-2019 vintages.

According to Perrotti-Brown, Opus One ‘remains one of Napa’s largest production, high-quality brands (around 25,000 cases per annum)’. The brand has enjoyed increased secondary market demand in recent years, doubling its trade value between 2020 and 2022. Opus One was the most traded US wine in January.

Its most active vintage and latest release, the 2019, was the culmination of Perrotti-Brown’s tasting with the winemaker Michael Silacci. In her report, Perrotti-Brown said it was ‘undoubtedly one of Silacci and his teams’ most extraordinary achievements thus far, delivering an intense, multi-layered expression of the vintage in a fantastically elegant, medium-bodied package’.

The highest-scoring Opus One vintages from this tasting were the 2019 and the 2007, with both receiving 98-points. While the 2019 has not yet risen in value, the 2007 has enjoyed an increase of 162.1% since release. Perrotti-Brown revealed that 2007 ‘was the first year winemaker Michael Silacci co-fermented all the Petit Verdot with the Cabernet Sauvignon’.

Perrotti-Brown also got a ‘sneak peek’ at Silacci’s ‘newest baby – the 2022 Sink Blend’, which is a ‘proportionally correct blend of all the components harvested that vintage’. She explained that the wine was ‘a very different style from the graceful 2019 expression – 2019 possessing more energy, 2022 delivering more power – yet all signs point to another incredibly successful vintage’.

News Insight

La Place de Bordeaux continues to expand

One of the seven wine trends to watch in 2023, according to Felicity Carter’s latest article for Meininger’s Wine Business International, is the growing importance of La Place de Bordeaux.

Originally a hub for distributing Bordeaux’s finest wines, La Place is a three-tier system where producers sell their wine to a network of over 300 négociants (via a middleman, known as a courtiers), who then sell to merchants in more than 170 countries around the world. The distribution network ‘more or less controls the ex-cellar sales of wines from all of the top estates’.

Carter points out that today ‘it’s the producers of the New World that are building La Place into a powerhouse’. ‘Being listed on La Place remains a sign that your wine is one of quality, and that the quality is recognised by people of taste,’ she writes.

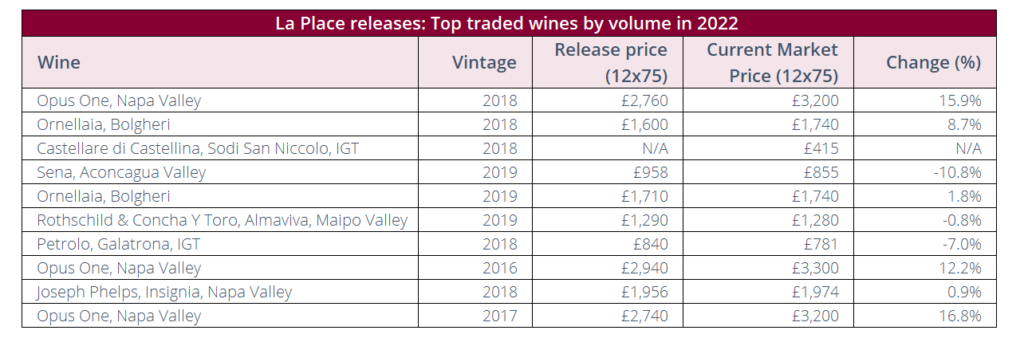

Recent years have seen an expansion of wines offered on La Place. The Chilean brand Almaviva was the first non-Bordeaux wine to be offered via the network in 1998; the list grew to 108 wines from 32 regions across 11 countries, which were released during last year’s campaign. Some of these releases have generated secondary market action and some have seen their prices rise. For the first time this year, the Chilean brand Seña, which is also released via La Place, joined the Rest of the World 60 index as it enjoyed greater demand in the secondary market.

Of the wines released via previous La Place campaigns, the top traded wines by volume can be seen in table below.

Names joining La Place this September include Napa Valley winery Chappellet, Barolo’s Giacomo Borgogno & Figli and Chilean winery Vik.

Final Thought

Burgundy – Global wealth creation and the value of luxury

Our latest extended report, Burgundy – for the few, not the many, pointed out that Burgundy seems to be playing in a league of its own. Stratospheric prices have limited its top names to the ultra-wealthy and value has become harder to find.

The following paragraphs look at some of the additional insights that didn’t make it into our report, including the cause of rising prices for luxury goods, along with other investment options to Burgundy – in the worlds of both fashion and wine.

Global wealth creation boasts Burgundy and luxury goods

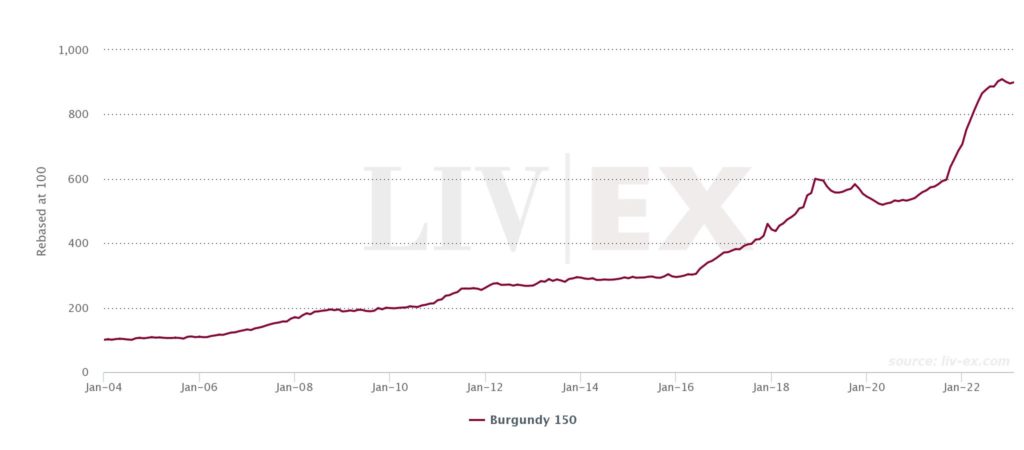

Back in 2018 Burgundy prices appeared to have peaked. They declined consistently throughout 2019 (the Burgundy 150 was the worst performing index, down 8.8%) but the factors behind that slowdown were different from now – as highlighted in our January report.

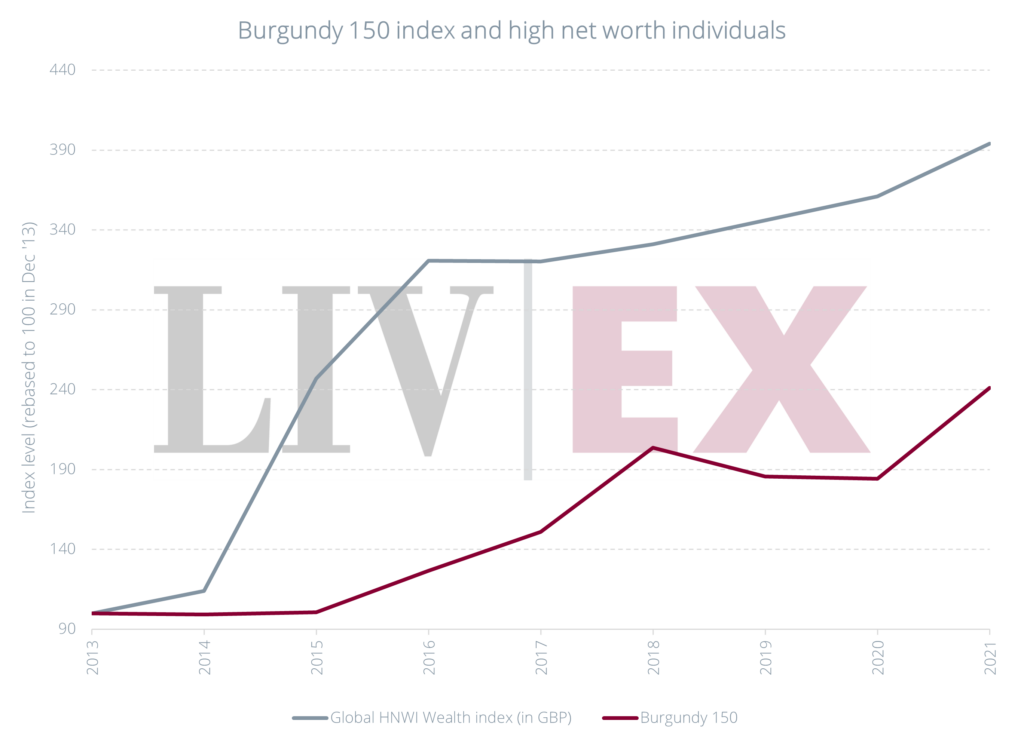

Burgundy’s recovery was triggered by the Covid-19 pandemic and the lockdown that followed in 2020.

Collectors and enthusiasts, no longer able to visit restaurants and hotels to drink the best wines, went online and shopped hard. Speculators joined the party and prices rocketed, as the chart below shows.

The Liv-ex Burgundy 150 index since inception

*made using the Liv-ex Charting tool.

The extended period of cheap money and huge government spending combined with the money saved through lockdown further boosted the wealth of HNWs. As highlighted in our report on the fine wine market in 2022, this money had to go somewhere. First mainstream assets were the big beneficiaries – from equities to residential property. But so too, were alternatives.

As the chart below shows, the rise in the Burgundy 150 index neatly correlates with the rise in the number of high-net-worth individuals (HNWIs) during the pandemic.

Rising prices were not limited to the top-end of the wine market. According to reports by both Deloitte and CapGemini, Covid and the accompanying lockdown sparked renewed interest in other alternative investments from Modern Art to Classic Cars and even, to fashion. For example, the average price of a Chanel Medium Classic Flap handbag rose over 50% between 2019 and 2022.

In 2021, one could get almost ten Chanel Medium Classic Flap bags for the same price of a case of Domaine de La Romanée-Conti (on average).

The DRC ratio

However, for those focussing on fine wine investments, comparing Burgundy’s brightest star (Domaine de La Romanée-Conti) to the top names of other regions shows that the price gap between Burgundy and the rest of the fine wine market continued to widen.

Back in 2019, one could buy ten cases of a First Growth (on average) for the same price of a case of Domaine de La Romanée-Conti. Today, one can get 16.3 cases of First Growths – or 29 cases of Super Tuscans.

The price ratio between DRC and the First Growths has continued to grow since December 2017. However, the price ratio between DRC and the Super Tuscans has been more volatile.

As the chart shows, for the price of one DRC case, one could buy 29 cases of Super Tuscans in both 2018 and today. However, in November 2020, when the Super Tuscans were at the height of the market, as highlighted in our Power 100 report that year, one could only buy 24 cases.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £80m of bids and offers across 16,000 wines.

Independent data, direct from the market.

Sinquisis alor disamet.