Burgundy 2021 – For the few, not the many

Introduction

Burgundy 2021 is a vintage full of paradoxes. On the one hand, it is exciting due to its quality; on the other, it is challenging for growers, merchants and collectors alike due to its limited quantities and pricing. In a recent report, Neal Martin (Vinous) summarised the vintage as ‘the most frustrating, convoluted, brilliant, disappointing, vexing, motley, inspiring, distasteful, delicious, remarkable vintage in recent years’.

To a certain extent, last year’s Burgundy En Primeur campaign should have prepared us for what was to come. Producers were releasing full allocations to make up for the expected shortfall in this year’s campaign. But the resulting 2021 campaign has been worse than most had feared.

Due to the low yields, producers were forced to push prices to cover their costs. To the disappointment of merchants and collectors, release prices were up 25% on average. Some of the top names are being released later than usual as producers decide on allocation and pricing. Some leading merchants have announced that certain highly sought-after wines would not be available on their lists, while others have been allocating one case per client, if any at all.

Critics like Jancis Robinson compiled lists that recommended what to seek out. Perhaps unsurprisingly, hers did not include any Grands Crus ‘as these are now so expensive’. Drastically low volumes and ever-rising prices might lead buyers to consider older vintages in the secondary market, or simply to give up their meagre allocations entirely.

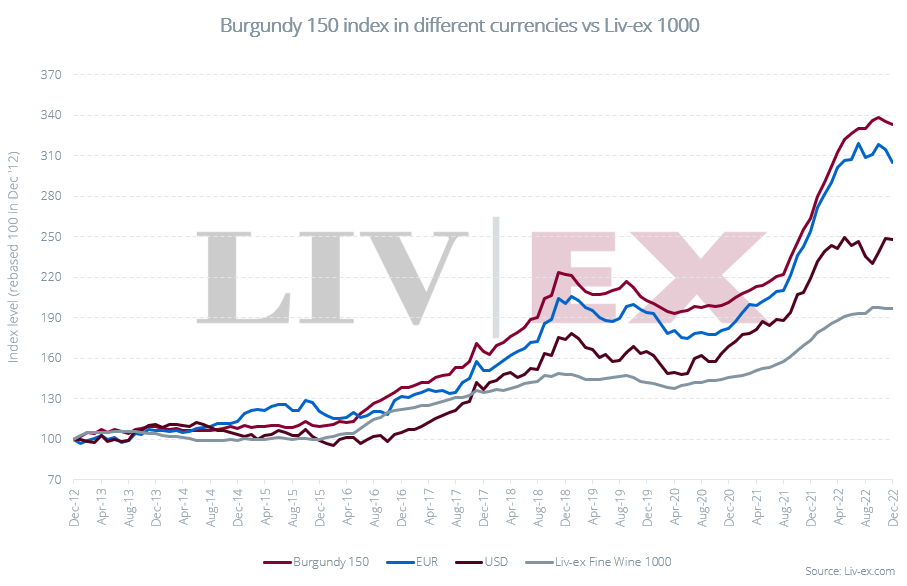

Indeed, the secondary market for Burgundy looks hot on the surface. The 2022 Liv-ex Power 100 was ‘all about Burgundy’ and, in the last year, the Burgundy 150 index rose 26.7%, outperforming all other fine wine indices. Burgundy’s trade share also reached an all-time annual high of 25.9%, and the number of wines traded set a new record at 4,306 (LWIN11s). However, most of these gains were limited to the first part of the year.

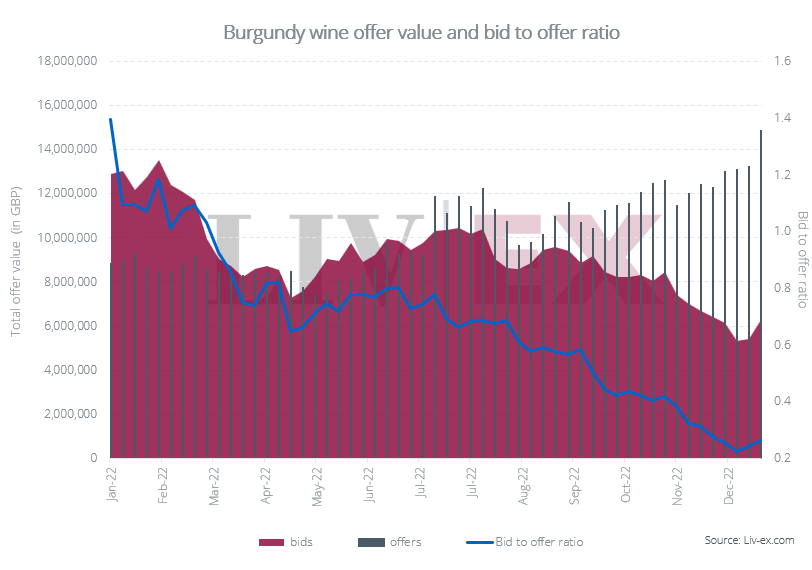

But Burgundy’s 2021 vintage has been released into a market that is increasingly fragile. Market sentiment toward the region has been waning, which in turn is impacting prices. The current bid:offer ratio sits at 0.26, down from 1.1 in January 2022. The Burgundy 150 index has fallen 1.5% in the past two months. The region is faced with the same macroeconomic challenges as other markets, but at these prices, those expecting a return on investment face increased downside risk. Burgundy’s three-year average annualised volatility is also among the highest of all regions at 25.8%. By contrast, Bordeaux, considered a more stable investment, sits at 9.2%.

These stratospheric prices have limited Burgundy to a shrinking number of buyers. As our 2022 Power 100 report highlighted, price increases have not been limited to the Grand Crus of the top Domaines. Indeed, négociant labels, such as Charles Lachaux, have seen some of the biggest rises. There have also been launches of new labels – a trend pointed out by Neal Martin in a recent opinion piece – which has been reflected in the broadening of the market.

In his report, Martin exposed other issues, such as artificial price inflation, and price-matching (‘ensuring your like-for-like Premier or Grand Cru is not cheaper than those of your peers for fear of being perceived as inferior’). He also suggested that ‘market prices imply a gulf in quality between regional Burgundy and Grand Crus’, which is ‘an exaggeration of the Burgundy hierarchy’.

This report aims to unpick some of the issues raised by Martin and considers the future of Burgundy’s secondary market.

Critic and trade views on Burgundy 2021

Drastically low volumes

Volumes have been the focal point of conversation when it comes to the release of Burgundy’s 2021 vintage. An exceptionally difficult growing season resulted in one of the smallest harvests in recent history. The biggest issue was the April frost that destroyed much of the crop. The vintage then received further setbacks, including regular rain, localised hail, downy and powdery mildew and even botrytis. Due to the cooler conditions, harvest began a month later than in 2020.

The Bourgogne Wine Board (BIVB) pointed to a crop of 900 to 950,000 hectolitres, representing ‘about 50% of a normal year’, and ‘2/3 of the average in recent years’. The Chardonnay losses were ever bigger than the total average, with some producers in the Côte de Beaune reporting quantities down 70% to 80% (Decanter).

As a result, some merchants announced that they would not be making any 2021 offers this year, while others are allocating only a case per client of the top wines.

Classic Burgundy style

In terms of style, the reds have been described as light and fresh, with typical alcohol levels of 12.5% to 13%, while the whites are complex and concentrated.

According to Jancis Robinson, ‘what 2021 delivers, in the right hands of course, is a return to classicism, the produce of weather more often encountered in the 1970s and 1980s but with first-class plant material in the vineyards and infinitely more skill and ambition in the cellar’.

Matthew Hayes, also writing for the publication, said: ‘2021 is nothing like the vintages we have seen from 2014 through to 2020. It was a timely reminder to all and sundry that before our current climatic travails brought such constant warmth, nature retained (and evidently retains) the power to disrupt, and perhaps ultimately resolve, as she sees fit’.

For Neal Martin, ‘the vintage unequivocally harks back to when Pinot Noir was all about bright red fruit and tartness, that elusive combination of weightlessness and intensity, transparency and terroir expression’. However, the critic also observed he ‘cannot hail it as a bona fide great vintage’ but ‘there is a growing sense of mastery in overcoming seemingly impossible odds’.

He noted that ‘some wines magically transcend the season’ and ‘there are gems to find’. ‘It’s just that you might not be able to buy them, and if you can, you might have to remortgage the house.’

The price of rarity

Unlike Bordeaux, which is driven by critic scores, the Burgundy market has long been moved by rarity. In the case of the 2021 vintage, rarity is a given. But Neal Martin suggests that some have taken advantage of these market forces. He gives an example of acquiring ‘finished wines from a struggling co-operative’ who have limited ‘production to a dozen bottles and two-thousand NFTs’, bidding up the price until, he jokes, their wines ‘reach parity with Romanée-Conti’. As after all, ‘what tastes better than rarity?’.

However, for Martin, such market manipulation is a car crash waiting to happen. Indeed, the secondary market is already showing signs that Burgundy has become too hot (for many) to handle.

Find the Burgundian trading opportunities live now on the global marketplace

The state of the Burgundy market

The previous peak vs now

In our 2019 report on the region, we questioned the sustainability of Burgundy prices. The market seemed to have peaked and had started to turn. Prices declined consistently throughout 2019 (the Burgundy 150 was the worst performing index, down 8.8%) but the factors behind that slowdown were different from now.

In 2019, trade volumes remained steady suggesting that the market had not lost confidence in the region. After a doubling in price in three short years, the market was due a pause. The decline in fine wine prices back then was also partly related to currency. The pound had just been given a boost after Boris Johnson was appointed as Prime Minister amid renewed hopes of positive Brexit outcome. As a result, the Liv-ex indices, which are denominated in sterling, dipped.

The market was also dealing with the aftermath of the implementation of US tariffs, which led to a fall in Burgundy demand from the US. A further hit to sentiment came in the form of political and economic strife in HK and worsening trade relations between Chain and the US. As a result, spreads began to widen and prices drifted.

Meanwhile cuts to global interest rates upped investor’s appetite for risk, which resulted in fine wine underperforming mainstream assets.

This then changed in 2020 when Covid and the ensuing lockdown sparked renewed interest in alternative investments. After a short pullback, the market raced ahead, led by the hottest wines in the game – Grand Crus Burgundies. Collectors and enthusiasts, no longer able to visit restaurants and hotels to drink the best wines, went online and shopped hard. Speculators joined the party and prices rocketed.

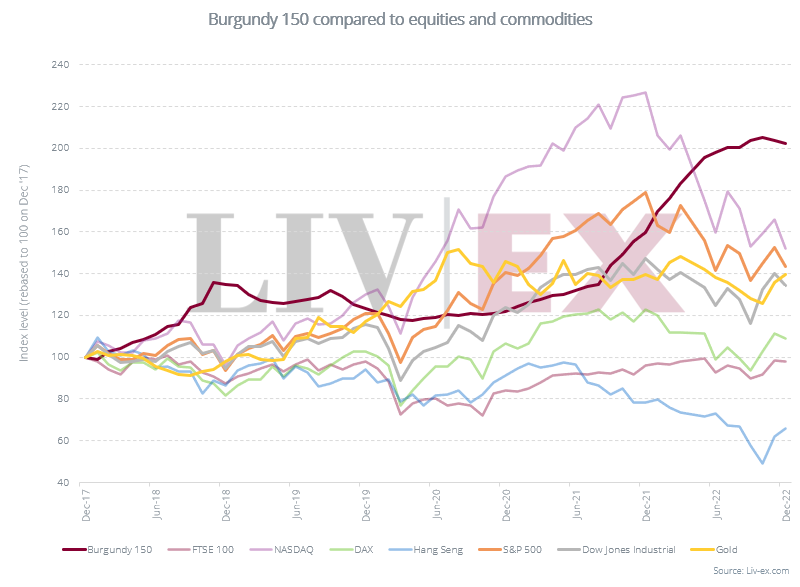

In 2021 and 2022, fine wine bounced back and outperformed global equities, but in the last quarter of 2022, macro-economic forces once again began to weigh on sentiment and thus prices.

Recent performance reveals profound issues

As we wrote in our report on the fine wine market in 2022, the year was ‘a game of two halves’, which was also true for Burgundy. The region’s secondary market performance became increasingly fragile as the year progressed.

The Burgundy 150 index rose 25.4% between January and July. It recorded its first dip of 0.1% in August; but rose 2.6% by end-October. The index then declined 1.5% in the last two months of the year.

Burgundy 150 vs Liv-ex 100 in 2022

")

*made with the Liv-ex Charting Tool.

As prices soared, buyers retreated. This can be seen in the chart below, which shows the rising value of offers and declining value of bids over the course of the year. The current bid:offer ratio – a measure of market sentiment – sits at 0.26, down from 1.1 last year.

Historically, a bid:offer ratio above 0.5 tends to indicate the beginning of an uptrend in the market, or at the very least acts as a sign of price stability. The opposite points to slowing market demand and increased price volatility.

Market sentiment can also be seen upon closer inspection of the Burgundy 150 index components. As the chart below shows, more than half the wines that make up the index fell or ran flat in December 2022. The ratio between the number of wines rising and falling has also been declining since May.

Price rises not limited to the top end

The reason for this change in sentiment might be because Burgundy’s top wines have reached prices that seem increasingly unsustainable. For example, back in 2019, one could buy ten cases of a First Growth (on average) for the same price of a case of Domaine de La Romanée-Conti. Today, you could buy 16.3 cases of First Growths – or 29 cases of Super Tuscans.

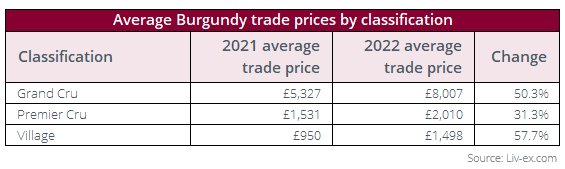

But these price rises have not been limited to the Grand Crus. Some of the biggest increases have actually been for village wines. In 2022, the average price for a village wine that traded on Liv-ex rose 57.3%, from £950 to £1,494 per 12×75 case.

To put this in context, one can buy a Bordeaux Second Growth for the same price as a case of Burgundy village wine. For example, the 100-point (LPB) Château Montrose 2019 has a Market Price of £1,485 per 12×75 at the time of writing. Other options include fellow Second Growth, Château Leoville Las Cases 2011 (£1,476) and Haut-Brion’s sibling, Château La Mission-Haut-Brion 2013 (£1,414).

Closing the price gap

Due to the exponential price increases of village wines, the price gap between village and Grand Cru wines has been closing. This has been especially true for some of the bigger names.

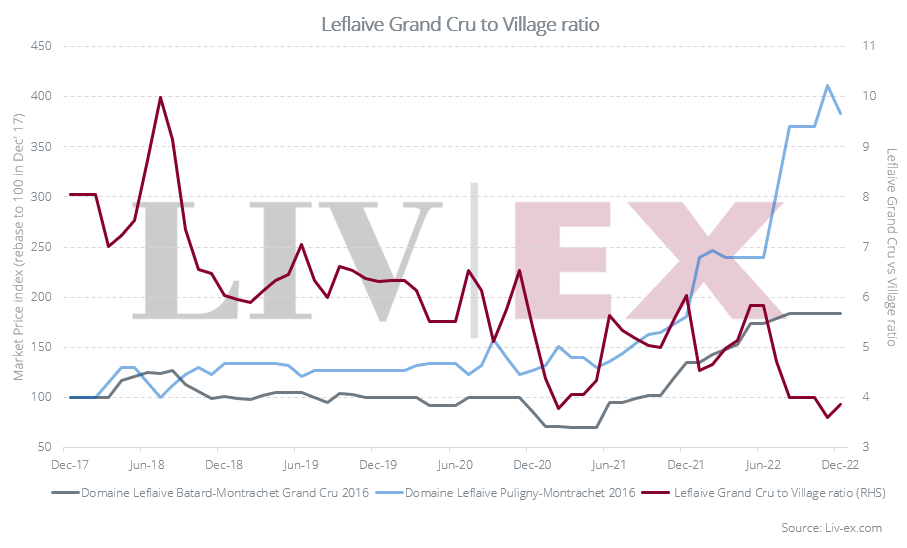

The chart below, for example, compares the performance of Domaine Leflaive’s Grand Cru, Batard-Montrachet 2016 with its village wine, Puligny-Montrachet 2016.

Over the last five years, the Grand Cru has risen 83.7% in value, while the village wine is up 283.6%. The price ratio between the two stood at 8.05 in December 2017, compared to 3.86 at the end of the 2022.

Similarly, in 2021, Domaine Dujac’s Bonnes Mares Grand Cru 2016 was trading 17 times higher than its village wineMorey-Saint-Denis 2017. In 2022, it was just 12 times more expensive.

Find the Burgundian trading opportunities live now on the global marketplace

The rise of the négociant label

As our 2022 Power 100 report pointed out, négociant labels have been subject to some of the biggest price increases. A good example of this is Domaine Arnoux-Lachaux, one of the rising stars in this year’s rankings. In the secondary market, its total trade (by value) rose 617.6% year-on-year. On average its prices were also up 487.2% but some of its wines rose more than 1,000%.

Some of Arnoux-Lachcaux’s biggest price rises were for its négociant label Charles Lachaux, which (like Leroy) offered a more accessible point of entry to a sought after grower.

The expansion of négociant labels has been a growing trend over the past ten years. While the domaine wines are restricted by ownership of Grand Cru and Premier Cru vineyard plots, the production of négociant wines is effectively unlimited. Some producers who have embarked on this trend in recent years include Alain Hudelot-Noëllat, Fourrier and Dujac (Dujac Fils and Pere).

However, Neal Martin highlighted the problem with this approach in his report – particularly the explosion of micro-negociants:

‘The combination of the Côte d’Or’s Mecca-like status and potential profit has spawned a proliferation of bijou labels that seem to appear overnight. Buy fruit or finished wine, not that either is explicitly mentioned on the label, then go market under your name.’

Burgundy’s prestige and allure has meant that a greater number of wines can be considered ‘fine wines’, in the sense that they might be collector worthy and enjoy global demand. It is precisely this image that has contributed to the region’s extensive broadening. Despite AOC restrictions on land, Burgundy now has the highest number of wines trading on the secondary market of any other region.

Burgundy’s greatest expansion

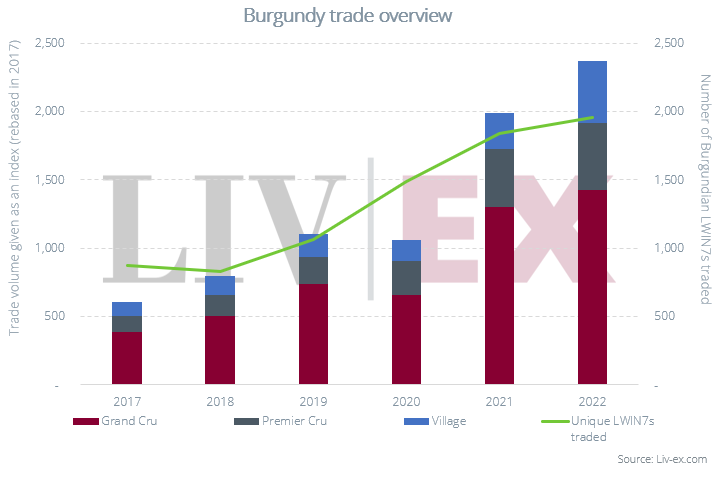

Indeed, Burgundy has also been the fastest expanding region on the secondary market and much of its recent broadening has been driven by village wines.

The number of Grand Cru wines trading over the past five years has increased 79%, compared with 207.5% for village wines over the same period.

The total trade value of village wines has also increased 68.3% between 2021 and 2022, while those of Grand Cru wines have risen just 9.4%.

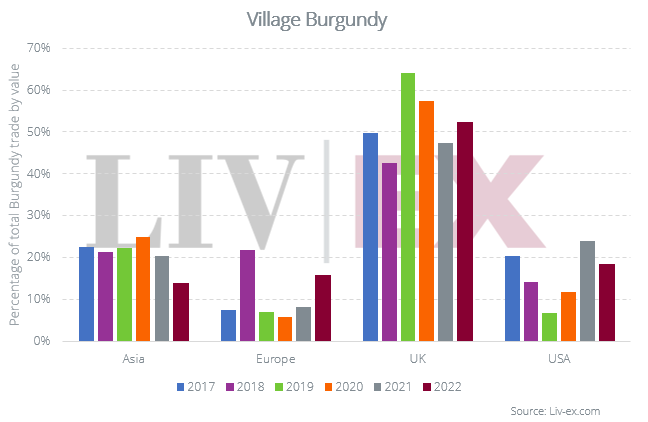

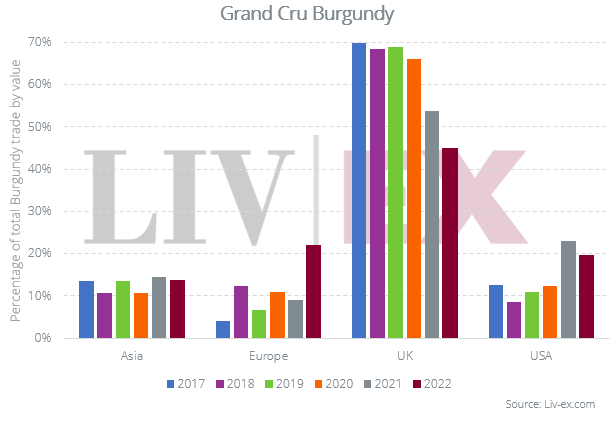

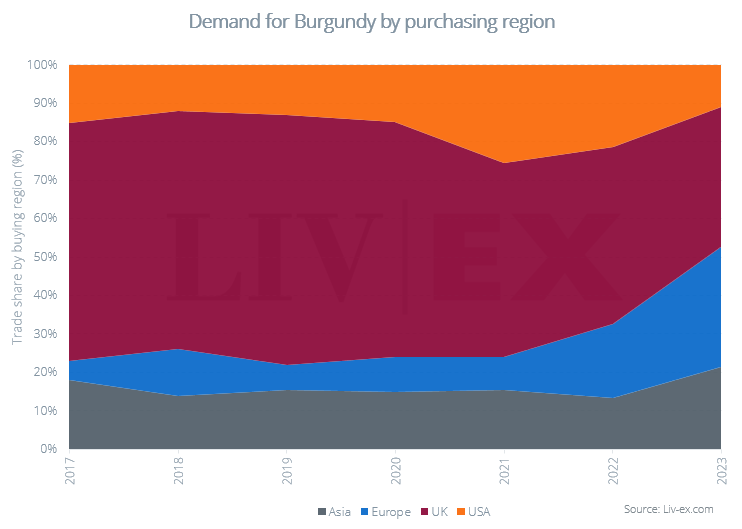

Compared to 2021, this increasing demand for village wines is largely coming from the UK and Europe. UK buyers, in particular, have become increasingly wary of buying into the top tiers. As the chart below shows, UK buying of Grand Cru wines has declined consistently since the region’s previous peak in 2019. Meanwhile, buying of Grand Cru wines has been steady in Asia and has risen in Europe.

This trend is also reflected in the overall demand for Burgundy over the past five years.

The UK’s share of the total Burgundy market has declined from 62% in 2017 to 37% in 2023. Europe has risen from 5% to 31% over the same period, while Asia has gone up from 18% to 21%.

Seeking value in Burgundy

If a few years ago buyers were turning to new growers or lower-classified wines to find value in Burgundy (a trend discussed in our last Burgundy report), the recent price inflation across all Burgundy classifications has complicated matters.

Over the past year, the 2019, 2018 and 2017 Burgundy vintages have been the most traded by both value and volume. But the limited release of the 2021 vintage is adding further pressure and might lead buyers to seek older vintages at comparably lower prices. For example, the 2012, 2014 and 2017 vintages generally command lower prices than 2010, 2015 and 2016.

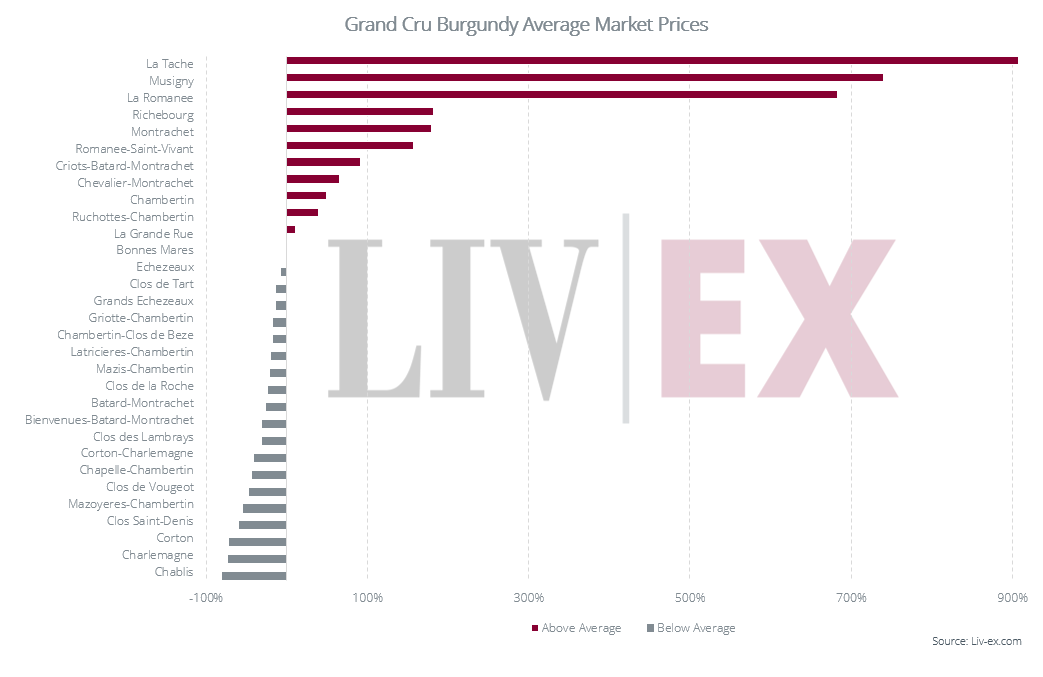

When it comes to the top classification, buyers might find value in Corton-Charlemagne, Corton and Clos St Denis, which sit comfortably below the average Market Price of Burgundy Grand Crus.

Conclusion

Finding value in Burgundy has become harder than ever. When one can buy a Bordeaux Second Growth for the same price as a Burgundian village wine, one might start to question the region’s market dynamics. Price inflation has affected the whole region, which in many cases, has been beyond the producers’ control.

This has certainly been the case with the 2021 vintage, which on average saw volumes down 50% and prices up 25%. While stock sold out, the mood around the campaign has hardly been positive.

Unfortunately, this price inflation means Burgundy is now a region for the few, not the many, limiting the number of market participants that can get involved. This has been fueled in part, by speculation but more generally by the simple economics of demand and supply. Burgundy desperately needs a string of high yielding vintages. Thankfully 2022 is said to be one.

Until then, high release prices and high secondary market prices will continue to deter buyers – particularly the old hands, but quite possibly the new too. The falling bid:offer ratio is pointing to this. At these prices, stock (albeit limited) is lingering on lists longer. The UK – which has long been the biggest Burgundy buyer – is taking an ever-declining share of Grand Cru trade. The Burgundy 150 index, which tracks the performance of the most traded Burgundy wines, began to slow in the second half of 2022 and fell 1.5% through November and December, while spreads widened.

Beyond the region-specific challenges, the economic outlook for the year is looking pretty bleak. The International Monetary Fund predicted weak global growth in 2023, highlighting ongoing issues such as high inflation and central bank tightening, Russia’s invasion of Ukraine, and the Covid aftermath, especially in China. Since then, however, China has unlocked and there are hopes that this will usher in a new wave of buying for the fine wine market as a whole, and Burgundy in particular. Indeed, financial markets have started the year in good cheer suggesting a lifting of the gloom.

During uncertain times, as an alternative asset class fine wine tends to perform well due to its inherent stability. But Burgundy seems to be playing in a league of its own. It has become riskier to buy, and harder to sell. While its secondary market is getting broader, the group of buyers of its finest wines is getting narrower. The question perhaps is this – if collectors are to commit new money to the fine wine market, will it be to Burgundy, or to other regions that this money gravitates?

Use exclusive tools to analysis and visualise the fine wine market –

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £80m of bids and offers across 16,000 wines.