Recent trading activity

Champagne’s rising trade share continued into the weekend. The region accounted for nearly 30% of trade, a little behind Bordeaux (34.9%) but more than Burgundy (18.1%). The biggest drivers were Dom Pérignon 2008 and Krug Vintage Brut 2008.

Italy accounted for 9.2% of total trade, with Tuscany at 5.2% and Piedmont at 3.8%. Year-to-date, the country’s average trade share sits at 11.8%, down from a record 15.3% last year. Its most traded wine this weekend was Bruno Giacosa Barbaresco Asili Riserva 2014.

Opportunities in Château Palmer

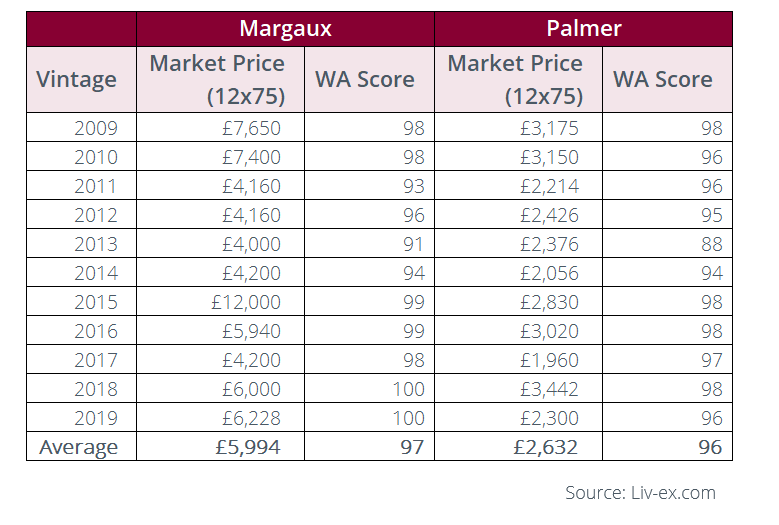

Perhaps unsurprisingly due to its First Growth status, Château Margaux commands a 127.7% premium over Château Palmer on average. However, there is just one point difference between their average scores, with Margaux averaging 97-points and Palmer, 96-points.

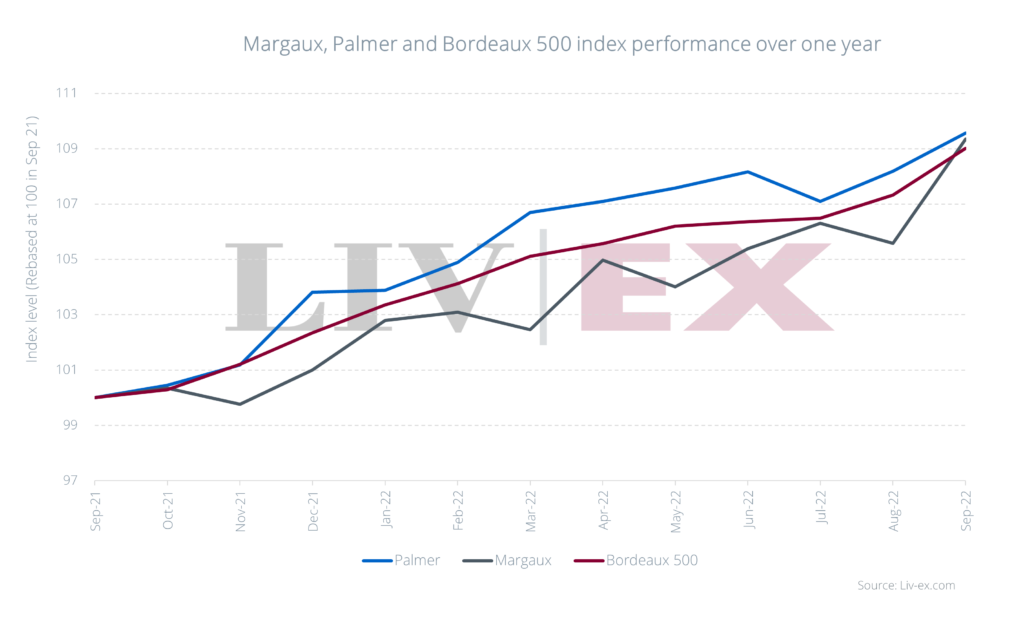

Over the last year Château Palmer has also out-performed its more illustrious neighbour in terms of price performance – albeit very slightly.

As the table above shows, many vintage of Château Palmer offer relative value. Its 2011 vintage, for example, was scored 96-points toChâteau Margaux’s 93-points, but is available at a 46.7% discount.

Château Palmer’s 2009 vintage is also available at a 58.5% discount to Margaux’s, even though they both carry 98-points.

Both estates have risen roughly the same amount over the past year. Yet Château Palmer is up 9.6%, compared to 9.3% for Château Margaux, and 9.0% for the broader Bordeaux 500 index.

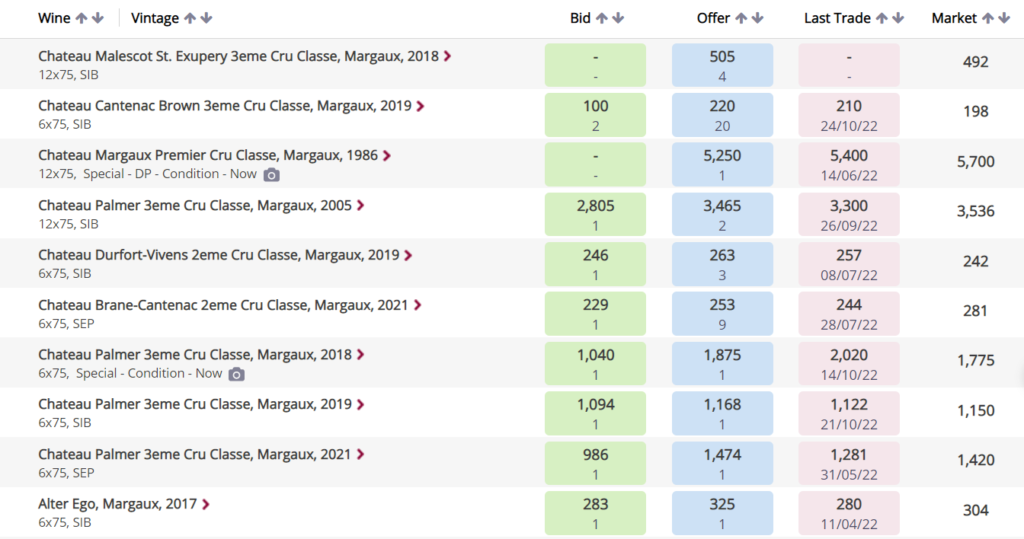

Live Opportunities for wines from Margaux

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £80m of bids and offers across 16,000 wines.

Independent data, direct from the market.