Recent trading activity

Buyers’ focus remained fixed on Bordeaux and Burgundy as the week progressed. Château Lafleur saw trade, alongside Château Haut-Brion 2009, Château Margaux 2015 and Château Beychevelle 2020.

Domaine Leroy continued to see trade, alongside other Burgundies such as Domaine de la Romanée-Conti, Romanée-Conti 2010 and Domaine Armand Rousseau’s Ruchottes-Chambertin, Clos des Ruchottes 2019.

There was also activity around Opus One 2018, as the release of the 2019 vintage early next month draws nearer.

The rising price of DRC

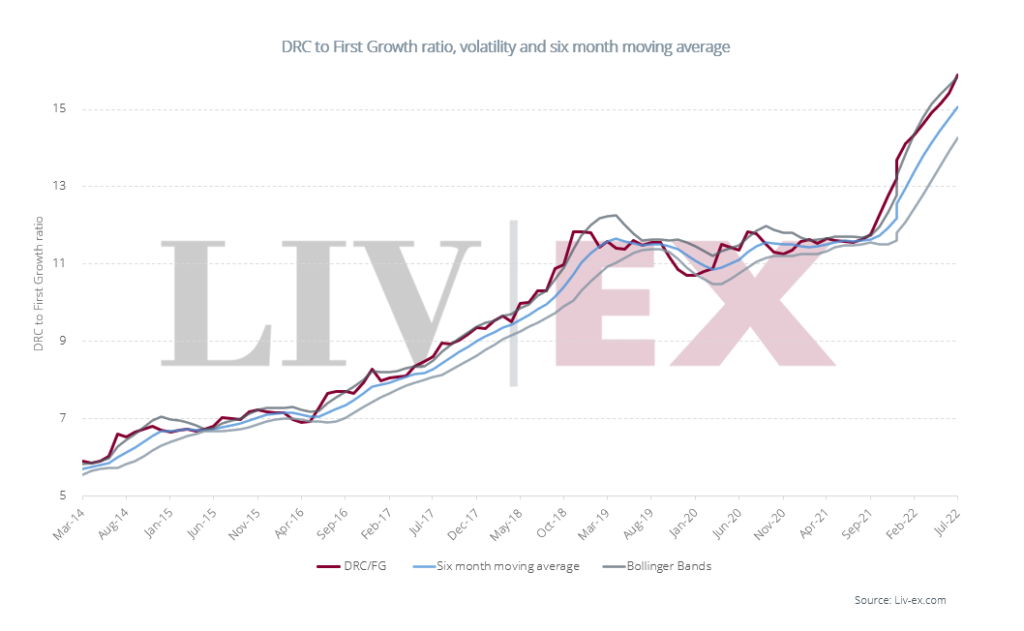

Since 2015, the rising price of what is undoubtedly Burgundy’s most famous domain, Domaine de la Romanée-Conti, has caused many to speculate that it was becoming overpriced relative to others. But those expecting a downturn have been kept waiting.

Since 2015, the rising price of what is undoubtedly Burgundy’s most famous domain, Domaine de la Romanée-Conti, has caused many to speculate that it was becoming overpriced relative to others. But those expecting a downturn have been kept waiting.

The chart above shows the historical relationship between the average prices of the Liv-ex Fine Wine 50 (tracking the First Growths) and the DRC index.

In essence it shows on average how many bottles of First Growth Bordeaux in the Fine Wine 50 one could buy for one bottle of DRC in the DRC index.

It currently stands at 15.89, with a six month moving average of 15.05. Prices of many blue-chip Burgundies, not least DRC, have surged since 2010, while those of Bordeaux have been more sedate.

The DRC Index has risen 40.6% over the last year and 16.9% year-to-date, while the Fine Wine 50 has risen just 7.7% and 2.9% over the same periods.

The ‘Bollinger Bands’ (no relation to the Champagne) in grey either side of the moving average show the highs and lows of an asset’s price over time.

The band will widen or contract depending on market volatility. The wider the band the greater the volatility and vice versa.

As can be seen, when the bands contract this creates a ‘squeeze pattern’. This can be followed either by a period of growth – as was the case from March 2016 to March 2019 and again in September 2021 (which is on-going) – or to a slowdown.

The last time the DRC:First Growth ratio was this great, in early 2019, when Burgundy prices reached an initial peak it was followed by a period of decline for the Burgundy 150 – of which DRC is a key component.

Meanwhile, as prices of DRC refuse to peak, it does suggest buyers might instead look at the relative value offered by the First Growths.

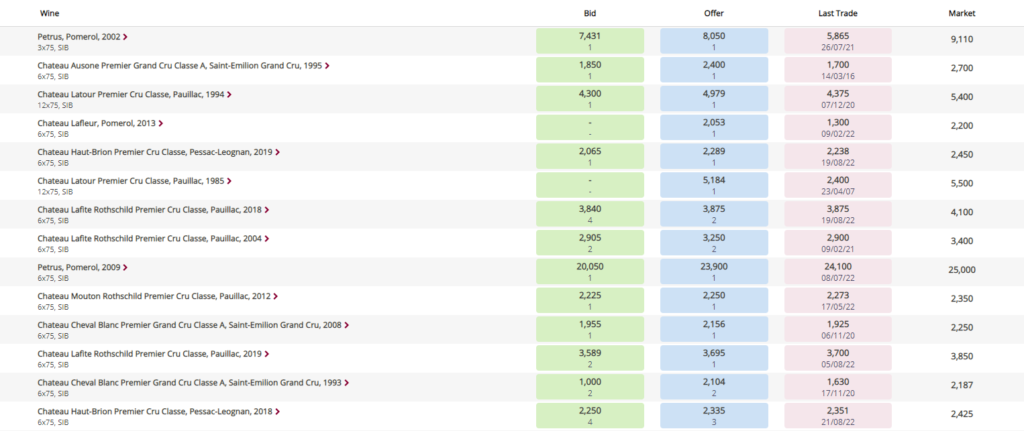

Opportunities to buy First Growths

Buyers looking for all LIVE opportunities among First Growths can find them easily on the blue-chip Bordeaux page on the exchange.

Buyers looking for all LIVE opportunities among First Growths can find them easily on the blue-chip Bordeaux page on the exchange.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £80m of bids and offers across 16,000 wines. Independent data, direct from the market.