In July 2019 we noted that one could buy 2.8 bottles of a second wine for the same price as a First Growth grand vin. This was down from a ratio of almost 6:1 in 2007.

In July 2019 we noted that one could buy 2.8 bottles of a second wine for the same price as a First Growth grand vin. This was down from a ratio of almost 6:1 in 2007.

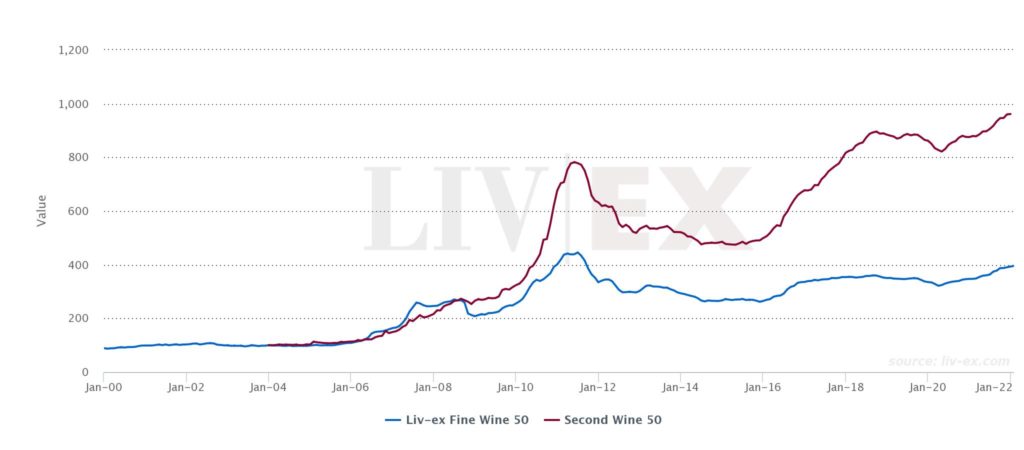

The Second Wine 50 – one of the strongest sub-indices in the Bordeaux 500 – flourished between 2015 and 2019, but since the pandemic began the Fine Wine 50 has started to enjoy stronger price performances (see table below).

This is starting to create widening gaps between the price of some First Growth wines and the price of their accompanying second wines.

This is starting to create widening gaps between the price of some First Growth wines and the price of their accompanying second wines.

As can be seen in the table below, the biggest differences between first and second wine prices is often greatest in highly-rated vintages.

For example, the Chateau Margaux 2015 is currently seven times the price of Pavillon Rouge 2015. However, there are important factors to consider here. The Margaux 2015 was a commemorative year and the last vintage by the late Paul Pontallier, both of which have boosted its secondary market performance.

For example, the Chateau Margaux 2015 is currently seven times the price of Pavillon Rouge 2015. However, there are important factors to consider here. The Margaux 2015 was a commemorative year and the last vintage by the late Paul Pontallier, both of which have boosted its secondary market performance.

The 2010 vintages of Château Haut-Brion and Château Latour are also rare 100-point wines from Neal Martin.

The second wines from these vintages should not be overlooked. Despite their less impressive scores, Martin is full of praise for these wines in his notes.

He said, the 2015 Pavillon was, ‘pure joy, pure class’; the 2010 Forts de Latour ‘frankly puts some of the Grand Vins in the shade’ and the 2016 Clarence de Haut-Brion was ‘full of tension and terroir expression’.

If the price of the First Growths continues to rise and the difference between first and second labels continues to stretch, there will be opportunities for canny buyers among the second wines once again.

View the active markets for the First Growths and their Second Wines using Indices Explorer.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 560+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 16,000 wines. Independent data, direct from the market.