Californian wines shine on the secondary market

London UK: Rising prices and increased activity for Californian wines on the secondary market show that the calibre of top Californian wines is now an accepted fact among the world’s fine wine community.

This is according to a recent report from Liv-ex (the London International Vintners Exchange) on the performance of Californian wines on the secondary market.

The report looks at the development of California’s secondary market trade, the price performance of leading estates, as well as where demand is coming from, and the future of the wine region.

Key findings also show that although Napa Valley dominates trade, Ridge Monte Bello from Santa Cruz Mountains has seen the biggest price rises in recent years.

Liv-ex is the London-based global marketplace for the wine trade, where 550 fine wine businesses from around the world buy and sell wine.

What happens on the exchange is a reliable indicator of the health of the secondary wine market.

An overview of Californian wine on the secondary market

A case of Kistler Vine Hill Vineyard Pinot Noir 1999 kickstarted California’s secondary market presence in 2002, when it became the first Californian wine traded on Liv-ex. Yet California’s cult wines quickly came to dominate trade.

Robert Mondavi and Ridge Monte Bello traded on the secondary market in 2003, followed by Dominus and Opus One in 2004.

Harlan Estate made its first appearance in 2009, and boutique garage winery Sine Qua Non saw its first trade in 2010.

The tipping point came in 2011 when the number of brands traded rose from four to nine. The number doubled again in 2012, from nine to 18.

In 2020, 200 different Californian wine brands traded on Liv-ex, an 809% increase over five years. This growth has significantly outpaced other growing regions; Italy and Australia, for example, have seen increases of 373% and 286% respectively.

So far in 2021, Californian wine accounts for 7% of the total value of traded wine on Liv-ex.

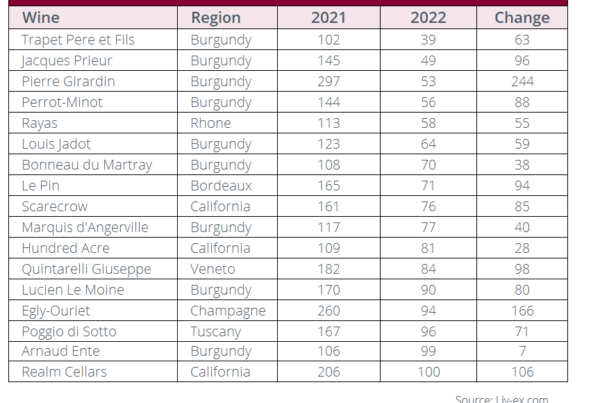

Rising prices for leading Californian wines

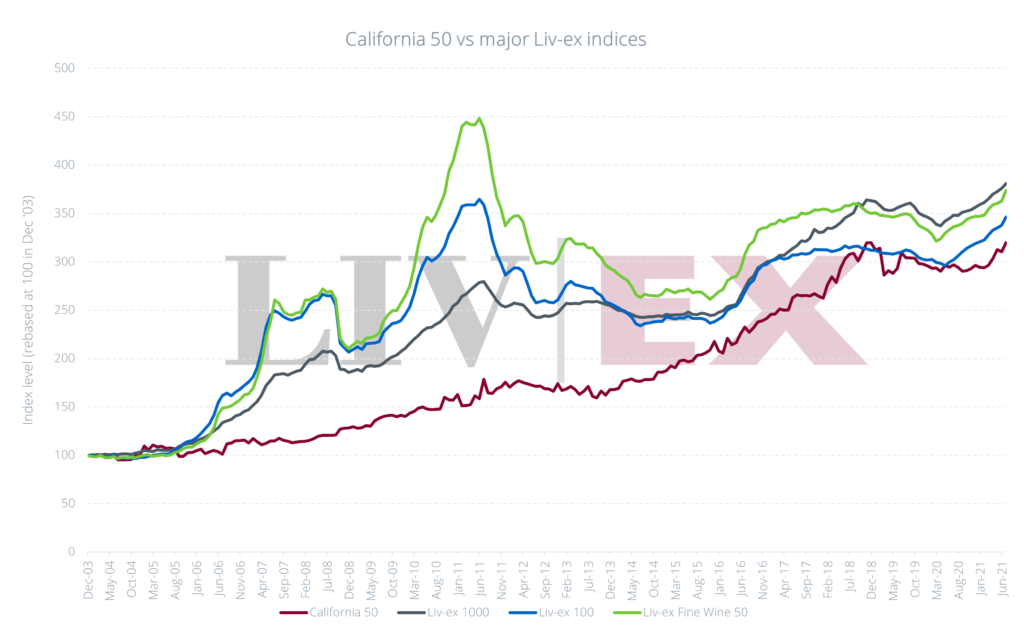

Californian wine prices have been characterised by low volatility and slow but steady increases over the past 18 years.

Since 2003, the average prices for leading California wines have risen 220%, as shown by Liv-ex’s California 50 index.

The California 50 index tracks the price movements of the 10 most recent physical vintages across the region’s most traded brands (Screaming Eagle, Opus One, Dominus, Harlan Estate and Ridge Monte Bello).

The prices in the index are calculated using the Liv-ex Mid-Price, which is based on merchant transactions and is the most robust measure for pricing wines available in the market.

It is calculated by finding the mid-point between the current highest bid price and lowest offer price on the Liv-ex trading platform. Each price is then verified by Liv-ex’s valuation committee to ensure that the number is robust after taking into account all data at their disposal, including merchant offer prices and historical Liv-ex transaction prices.

In July this year, the California 50 index reached an all-time high, having risen 8.7% so far this year.

Napa Valley dominates trade but smaller AVAs are on the rise

Perhaps unsurprisingly, Cabernet Sauvignon-based wines from Napa account for the majority of trade.

However, as more wines trade on the secondary market, Napa Valley has lost ground to other Californian AVAs.

Even within Napa, increasing demand for a wider array of wines has seen a growth in trade for sub-AVAs such as Oakville, Rutherford and Stag’s Leap.

Wines from Howell Mountain (Abreu and Dana Estates) have been traded for the first time this year as well.

Trade for wines from the Central Coast (1%) is largely represented by the boutique Sine Qua Non.

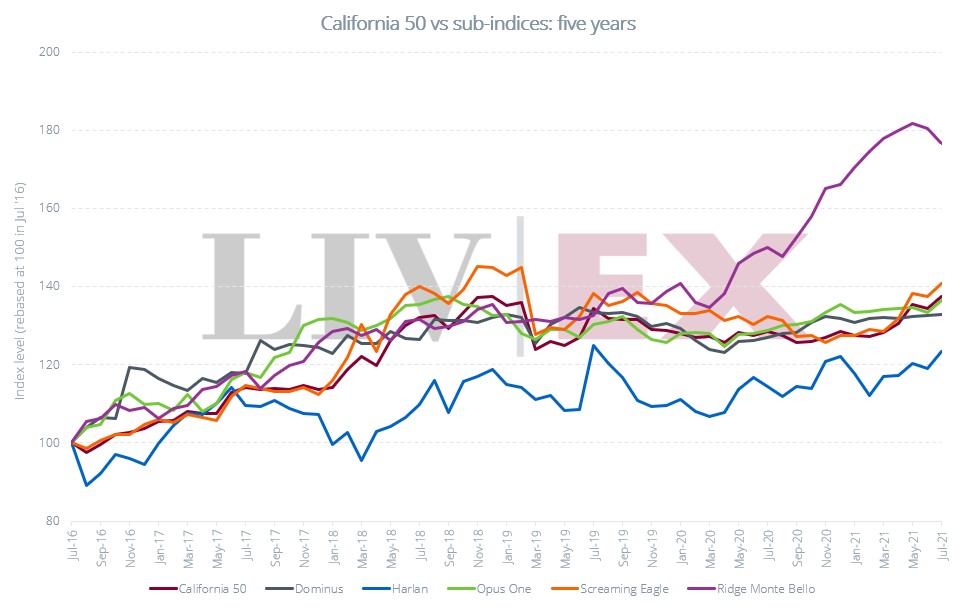

Ridge Monte Bello leads on price performance

Average case prices for Napa Valley’s leading estates are up significantly over a five year period with Screaming Eagle (40.7%), Opus One (36.6%), Dominus (33%) and Harlan Estate (23.4%) all showing impressive growth.

However, a wine from Santa Cruz Mountains has seen the biggest price increases over the past few years – Ridge Monte Bello.

Ridge Monte Bello prices are up 76.6% over five years, as shown by the Ridge Monte Bello index. The wine is the most affordable of the five wine brands in Liv-ex’s California 50 index.

Its production is also low compared to Europe’s top wines, meaning traditional supply and demand dynamics, along with high quality at lower prices have given the wine room to rise.

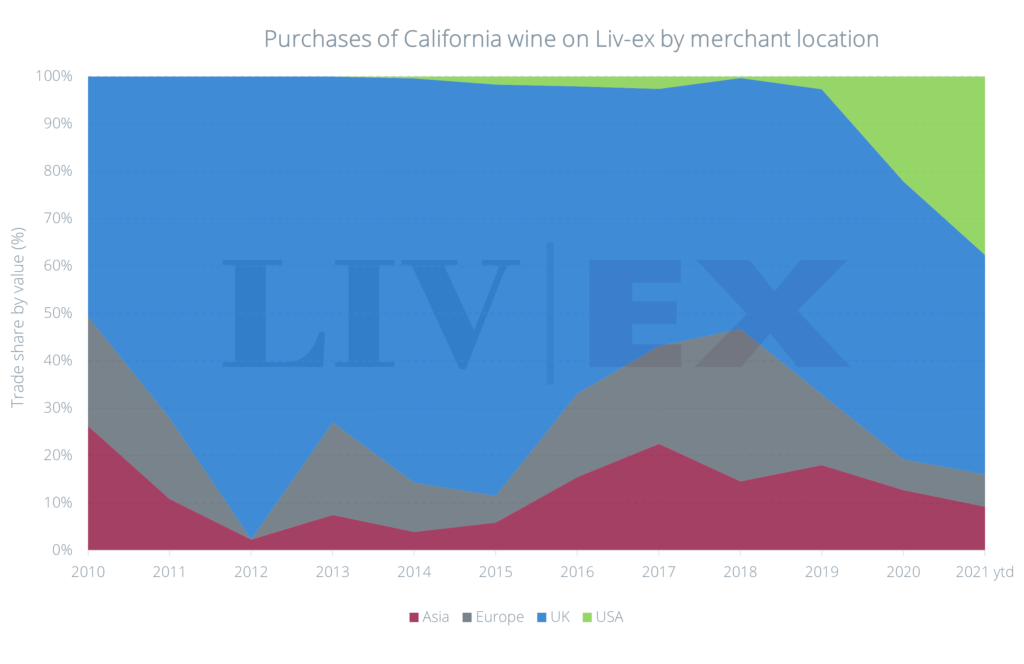

Where does demand come from?

According to the Californian Wine Institute, the top export markets for California wines in 2020 were Canada ($424 million), the United Kingdom ($236m) and the EU ($191m).

In terms of secondary market trade, the UK has historically been the biggest buyer of Californian wine, accounting for 64% of traded value.

The USA has long been an active seller of Californian wine, contributing to its global appeal. Now, US wine businesses are emerging as active buyers on the secondary market too.

Year-to-date, US buyers account for 38% of secondary market trade with the UK sitting at 46%.

In fact, the rising demand prompted Liv-ex to launch a weekly stock collection service to its members across the Golden State, meaning retailers also have a new opportunity to sell local wines, further facilitating trade.

The future of California

In the last few years, unprecedented droughts and fire events have put a question mark over the future of California as a wine region.

Wineries and vineyards have been destroyed by fires and crops tainted with smoke. The cost of water is also rising, piling the financial pressure on numerous operations across the state.

The fires in 2020 proved particularly devastating. There is a steadily growing list of estates, including the likes of Colgin and Schraeder, which have already announced they will be producing no wine from that vintage at all.

The exact impact of these natural hazards on the secondary market is less clear but producers in California are facing climate change challenges that need to be taken into account.

Conclusion

Since records began, Screaming Eagle has been the most traded Californian wine (by value). It is closely followed by Opus One, Dominus and then Harlan Estate.

So far in 2021, wines designated as “Napa Valley” have accounted for less than 90% of California’s trade share by value, down from 93% in 2010, as other Californian regions and varieties have found new buyers.

After years of waiting patiently on the side line, the full force of Californian wines is now being felt on the secondary market.

With a combination of cult wineries dominating trade and increasing diversity, few other fine wine regions offer high-quality and collectible Pinot Noirs as well as Cabernet Sauvignons, Chardonnay and Sauvignon Blanc, Zinfandel and Rhône blends.

Thanks to over 139 AVAs and counting, the Californian wine market is undergoing a massive expansion and is well-poised for future growth.

About Liv-ex

Liv-ex is the global marketplace for the wine trade. Along with a comprehensive database of real-time transaction prices, Liv-ex offers the wine trade smarter ways to do business. Liv-ex offers access to £80m worth of wine and the ability to trade with 550 other wine businesses worldwide. They also organise payment and delivery through their storage, transportation and support services. Wine businesses can find out how to price, buy and sell wine smarter at www.liv-ex.com.

Further information

This press release provides a shortened summary of Liv-ex’s latest report on California’s secondary market performance. The full report covers:

- Where demand is coming from

- The most traded wines by value

- A breakdown of California trade by sub-region

- Average case prices compared to other leading fine wine regions

- Analysis of distribution and secondary market exposure

- Wines from Oregon and Washington State

To request a copy of the report, please fill in this form.