2020 proved to be a solid year for the wine market. But naturally some regions fared better than others. Bordeaux found itself occupying the middle ground – it performed better than Burgundy and California but lagged Italy and Champagne. And it continued to lose market share. But this is a relative game and so does not necessarily reflect the sentiment towards Bordeaux. One of the more effective measures of sentiment is to watch the value of LIVE bids placed on the exchange relative to offers – the bid to offer ratio.

The bid to offer ratio is an indicator of demand for fine wine, the higher the ratio the stronger the demand.

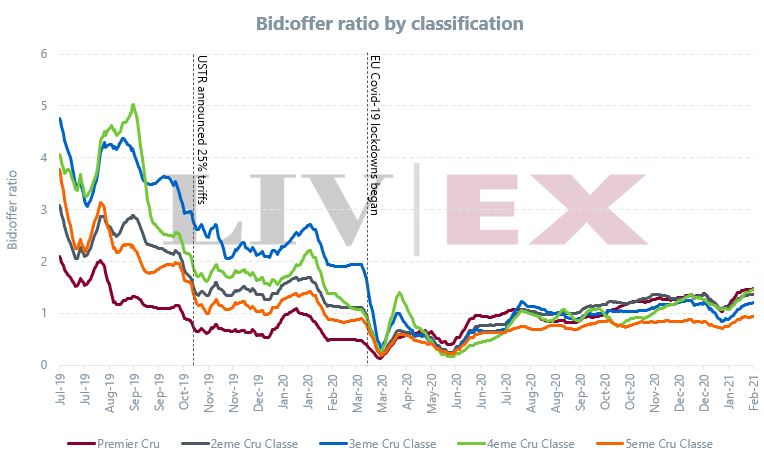

The two-year chart of Bordeaux’s bid to offer ratio, split by classification, can be seen below.

The summer of 2019 was marked by volatility as the Hong Kong protests were at their height. Then in October came the announcement of US trade tariffs. Exchange rate volatility ensued and finally, in March 2020, Covid-19 brought the world to a standstill. Cash was king and so bids collapsed.

Today the picture is beginning to brighten. While we are still some way off the peaks of summer 2019, the rise of bids has been steady, and seemingly sustainable.

Wine prices have been a beacon of stability through these uncertain times. A period of sustained low interest rates is widely expected, driving the value of mainstream assets to new highs. Bordeaux however, remains below its peak. First Growths in particular have lagged the market. The LX50 remains 22% shy of its all-time high set in June 2011. Might it be time to reassess Bordeaux’s relative value?

LIVE bids for all Bordeaux can be viewed here – £20m in total.

The best offers of Blue-chip Bordeaux can be found on our Opportunities Page, ranked by discount to Market Price.