It’s a short week in the UK, tomorrow marks 75 years since VE Day, and the British public will be off work to share in the celebrations. While wines from 1945 failed to trade this week (although several were offered!), a Barolo Riserva from VE Day’s 12th anniversary found the bid.

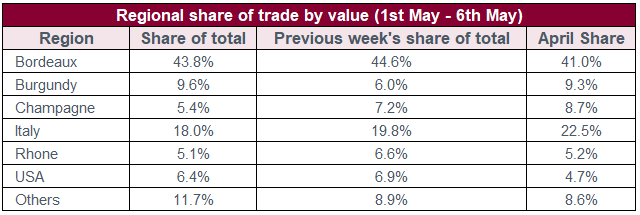

Value of trade was steady on the week prior and the regional share of trade was approximately parallel. The levels are beginning to configure into a new normal, as Bordeaux (43.8%) settles well under its 2019 average of 54.5%.

Italy made up 18% of trade share this week, a slight drift from the previous week but still more than double its 2019 average (8.8%).

Burgundy (9.6%) made a slight gain on the week, while USA (6.4%), Rhone (5.1%) and Champagne (5.4%) all fell slightly.

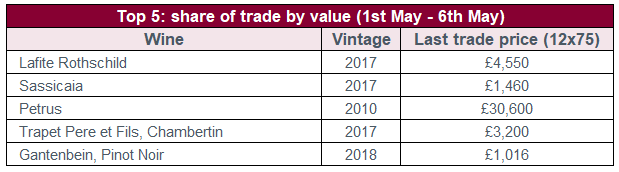

Lafite Rothschild 2017 led trade by value in the first week of May. The 2017 remains the cheapest when compared to the preceding ten vintages. While this could be considered an age discount, the 2017 is a decent 25% discount to the latest 2018 release.

The market has begun to take notice of value in 2017s as the vintage is gaining market share. It made up 18% of trade by value in the week, the single largest portion.

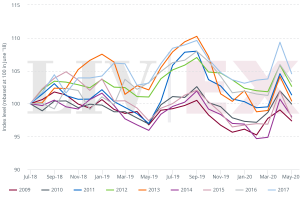

Chart 1: Bordeaux 500 – return by vintage over 23 months

Over the past 23 months, the 2017 vintage has led all other vintages in price performance. It just beat the impressive 2016s, a 1% difference. Although 2017s have risen the most in price, they remain at a hefty discount to the 2016s, 2009s, and 2010s. The “off” vintages of 2011, 2012, 2013 have also performed well in the past 23 months, holding their value. At the same time, the great but more expensive vintages of 2009, 2010 and 2015 have all fallen in price.

Liv-ex Indices in April

The Liv-ex 100 declined 0.3% in April and the Liv-ex 1000 followed, falling 0.4%. The indices have held up relatively well amid the market turbulence. The Fine Wine 50 even increased 0.82% in the month, a testament to the allure of the First Growths.