The political and fiscal responses of governments worldwide to the outbreak of Covid-19 have been closely watched by the financial markets this month. Exchange and interest rates, equities and bonds, have all swung wildly on the perceived effectiveness of their actions.

The FTSE 100 posted its biggest quarterly fall for more than three decades, the Stoxx Europe 600 fell the most on record after the European Central Bank’s measures fell short of market expectations and the Dow Jones recorded its largest single day decline. The final week of the month saw some semblance of calm return to proceedings, but for how long?

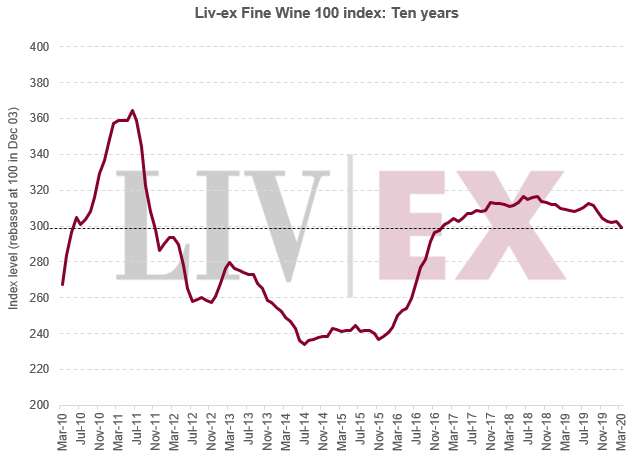

Amidst all this, the Liv-ex 100 declined just 1.06% to close at 299.36, helped in part by the weakness of Sterling which adjusted prices lower when viewed in Dollars, Euros and Swiss Francs. This, along with considerable demand for home deliveries, allowed merchants to hold their prices steady.

With governments worldwide extending their lock down periods, one might expect the demand for home deliveries to continue at whatever price level wine lovers imbibe. However Sterling is now showing signs of strength and Bordeaux 2019 has been put on ice, creating a potential vacuum over the months ahead. Fine wine’s long-term fundamentals remain intact – arguably supply is diminishing at a faster rate than ever – but with so much uncertainty still at play, few are prepared to call the market’s direction from here.