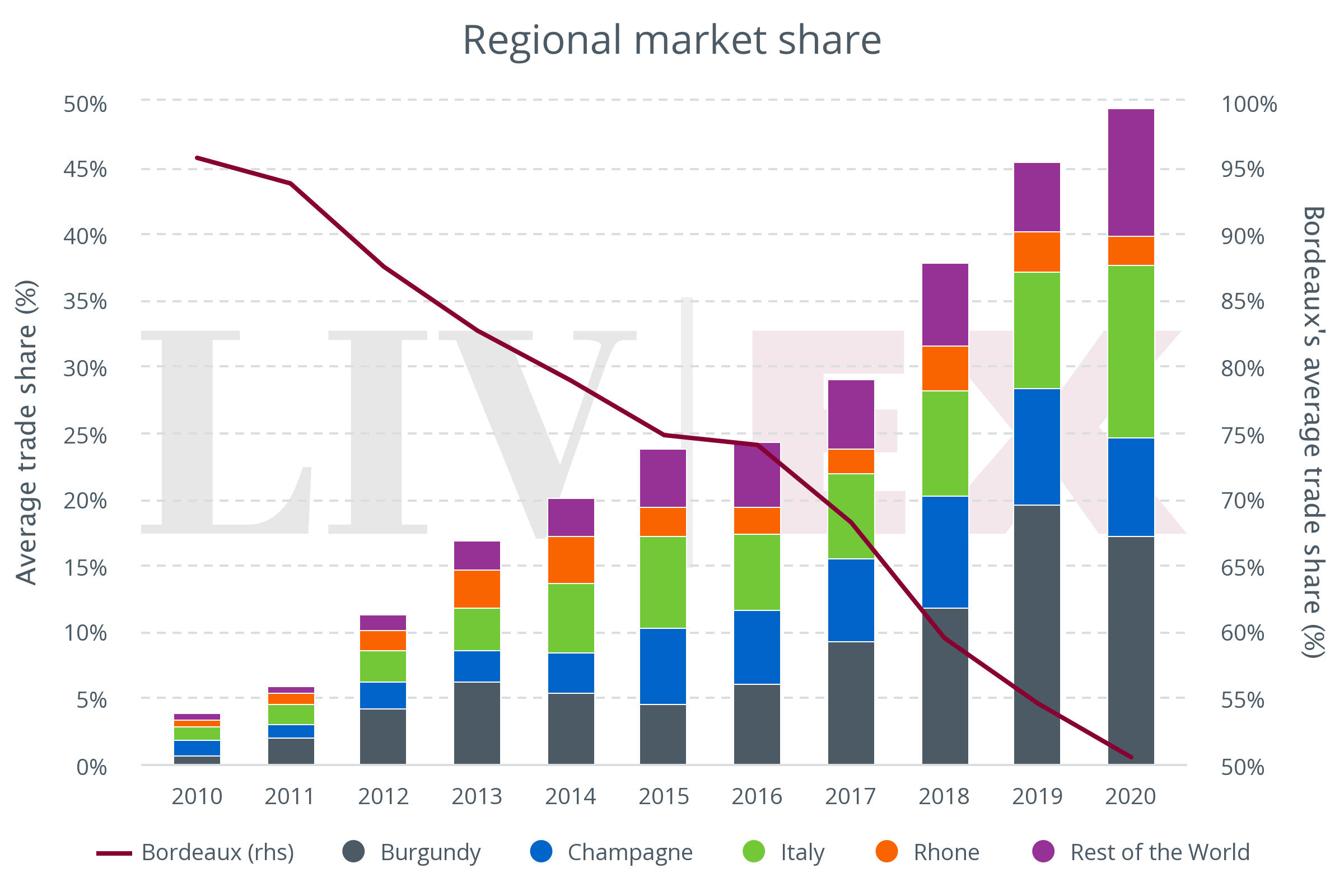

The power balance in the fine wine market has continued to shift throughout the first quarter of the year. Buyers’ interests have been changing, reflected in the regional trade share patterns.

Bordeaux – the fine wine market’s dominant force – has fallen to a record low of 50.5% so far in 2020. The most actively traded vintages from the region have been 2009 (15%), 2010 (12%) and 2016 (11%).

Burgundy, which used to be the main beneficiary of Bordeaux’s decline, however, has also been losing market share, averaging 17.2% this year (down from 19.6% in 2019). Moreover, its price performance has been in decline, with the Burgundy 150 index down 2.5% year-to-date. Champagne (7.4%) and the Rhone (2.3%) have also seen their shares drift, if only marginally.

Exempt from Donald Trump 25% tariffs, and in the midst of strong Brunello 2015 and Barolo 2016 campaigns, Italian wine trading has been on the rise. Italy’s share by value has increased from 9% (2019) to 13% (2020); prices, as measured by the Italy 100 index, have risen 0.6% year-to-date.

More impressively, the Rest of the World has seen its trade share double – from 5% last year to 10% in 2020. Within this, Germany, Spain and Australia have accounted for 1% each but it has been the USA, at 5.3%, that has elevated the RoW category to a record high. Most active wines from the region have been flagship Napa Valley Cabernet Sauvignons, led by Screaming Eagle and Harlan Estate.