$558,000 for a single bottle of 1945 Romanée-Conti

When it comes to investment, wine, art and cars have often been regarded as ‘pleasurable’ assets. Common perceptions exist that these tangible assets, often put under the same roof, simply serve to diversify a portfolio; they are safe yet less liquid, and if worse comes to worst, can always be enjoyed.

The notable distinctions between them, however, are rarely acknowledged. In an article published last year under the title ‘The Best Investments of 2018? Art, Wine and Cars’, the Wall Street Journal commented: “Who beat the market this year? Investors who like the finer things in life”. Financial newswires occasionally report on the performance of these alternatives through published indices, commonly citing Liv-ex with regards to fine wine and Sotheby’s Mei Moses when art is concerned.

Maybach Exelero, a one-off high performance car, costs $8 million

But fine wine as an alternative asset class is not so like art and classic cars – it is easier to value accurately. The price of classic cars, for instance, is often determined by their history, prestige, condition, original features, awards and popularity: a car once driven by someone famous or with an interesting history might demand a higher price. Indices that track the classic car market are often based on auction sale results, such as the K500.

Salvator Mundi by Leonardo da Vinci (c. 1500) is the most expensive painting ever sold as of 2019 for $450.3 million

When it comes to art, every piece is different, and every copy is considered a replica which cannot command the same price as the original. Some argue that art, even sculptures and paintings, is ephemeral, which is part of the joy in collecting and owning it. It can also take decades for the same original piece of art to reappear on the market, making valuation challenging despite the emergence of art indices. Estimations are often the norm and can be based on the auction value of other works by the same artist, as well as demand, liquidity, activity of the art dealers and market data.

Wine is a very distinctive category in that sense. Each year, producers make many bottles of the same wine. Some, like top Bordeaux, is made in significant quantities. Even the smallest producers will make several hundred cases of the same wine each year. As a result, the same products are often available simultaneously from retailers around the world, and change hands frequently. Rare old bottles such as Romanée Conti 1945, which broke a record in October becoming the most expensive wine in the world, are the exception rather than the rule. The vast majority of fine wine – collectible bottles that are built to age – is far easier to value than ‘unicorn’ bottles like these.

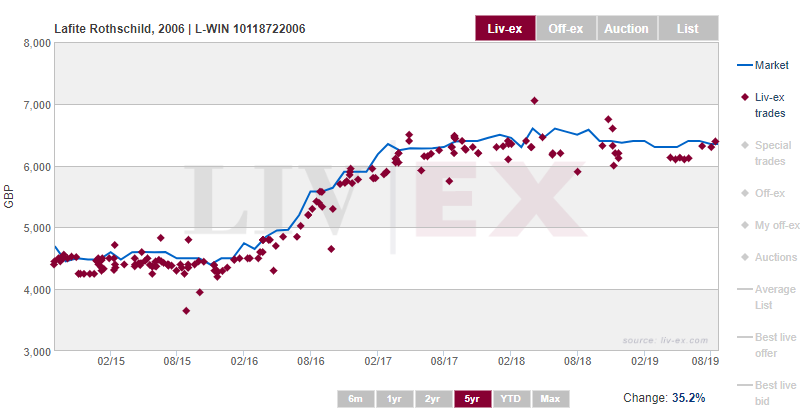

The chart below shows trading activity for Lafite Rothschild 2006 over five years. The red markers represent trades of the wine on Liv-ex. The dark blue line is its Market Price, which is widely used for valuations. As you can see, it tracks transaction prices very closely.

These factors – production volumes, multiple traders, availability and data – make it much easier to arrive at accurate valuations for fine wine than art or classic cars.