Liv-ex Director James Miles gave a presentation on the topic of ‘Speculation is dead. Long live speculation’ at the Wine Industry Conference on 6th November, as part of the Hong Kong International Wine and Spirits Fair.

Notes from the presentation, as well as the corresponding slides, can be found below.

Fine Wine – "Speculation is dead. Long live speculation."

By James Miles, Director of Liv-ex Ltd.

Slide 2

There is an interesting paradox that fine wine speculation is both rather frowned upon and deeply entrenched. I am going to briefly explore this paradox in a moment.

Assuming that wine speculation isn't over, and that this cycle is just another in a long history of boom and bust stretching back many hundreds – perhaps thousands – of years, I am also going to explore where we are in this cycle.

Finally, I am going to briefly explore where value may lie in the current market.

Slide 3

The sense that profiting from wine is rather vulgar has a long history, particularly in France. So much so that in Bordeaux the business roles were historically performed by foreigners. They mostly came from England, Ireland, Scandinavia and Germany and the likes of Johnston, Barton, Lawton and Schroder are still distinguished names in the region today.

This friction between the creatives and suits, common in many creative industries, is referred to by Benjamin Lewin in his book What Price Bordeaux as "Two centuries of mistrust between Chateaux and Negoce".

In 1812, the manager at Latour referred to a prominent courtier as a “vulture with cruel claws”. The writer Francoise Mauriac in the 1920s talked of "something resembling the Cosa Nostra in embryo” developing in Bordeaux with reference to the negociants. Comte Lur Saluces, the former owner of Yquem, once commented that the interests of proprietors and negociants rarely coincide.

Anybody familiar with Bordeaux will know that these frictions are still alive and well.

Slide 4

The reality is that speculation and wine have been closely intertwined since the beginning of time.

The ancient Greeks, Egyptians, Phoenicians and Romans, we are told, were all big traders of wine, and they each understood the impact that climate, weather and vineyard location had on demand, supply and price. The ancient Greeks also understood the importance of temperature controlled transport, developing a system of overnight shipments to Alexandria to avoid the heat of the day.

The English merchants in the middle ages were so rich that they were amongst the leading lenders to the crown, and top Bordeaux has been sought after by the wealthiest men in society for many hundreds of years. Famously, Charles II had Haut Brion in his cellar in 1660: some 350 years ago.

But it wasn't until the invention of bottles and corks in the 18th Century (which allowed wine to be stored for long periods) that speculation really took off. At that time Madeira and Port were particularly popular vehicles for speculation, as was Bordeaux.

One example is the story of Herman Cruse, who bought 90% of the entire Bordeaux crop in 1847, possibly the most audacious act of speculation ever attempted. With revolution threatening to engulf Europe, no one else wanted anything to do with it. When revolution never materialised he cleaned up, amassing a vast fortune.

Slide 5

More recent economic history would seem to point to a reasonably reliable boom and bust cycle every 10 years or so. In World War Two prices rose 600% under a German occupied France and then promptly collapsed by more than 50% once the war was over. There were booms and busts in the ‘70s, ‘80s, and ‘90s, and in the last decade as well.

The 1970s cycle was particularly violent. Between 1970-2, Cru Classé prices quadrupled, only to fall back to 1970 levels in 1974. Most of the leading negociants of the period were wiped out in the process.

Subsequently, in 1975, one particularly hapless London brewer sold 2,000 cases of Mouton 1970 for £74 per case. Just five years later the same wine was worth £990 per case.

Despite this long history of boom and bust, however, wine has produced remarkably consistent returns. A recent academic paper estimated that fine wine returned 4.1% in real terms (after inflation, storage and insurance costs) between 1900-2012, putting it ahead of art, stamps and bonds and only narrowly behind equities.

Indeed, it is perhaps fair to say that wine is now pretty well established as an alternative asset. A 2012 survey by Barclays found that 25% of high net worth individuals had a wine collection and that about 2% of their wealth was tied up in wine.

Slide 6

Our own data seems to broadly back up the academics. Over the last 25 years the Liv-ex Investables Index has returned about 11% per annum in nominal terms, outpacing gold, property and equities in the UK. It has also been less volatile and thus less risky.

Slide 7

The last decade has been a pretty normal cycle by historical standards. The Bordeaux First Growths appreciated 4.5-fold between 2005 and 2011, before falling 41% between 2011 and now. Our broader Liv-ex Fine Wine 1000 index has been less volatile and produced similar returns, suggesting that holding a diversified cellar is possibly a sensible strategy.

While booms and busts in wine are influenced by external factors – in this case, UK pension reform, the collapse of Lehman, the removal of tax in HK and the huge fiscal stimulus in China in 2009 – they also tend to be self-inflicted and tend to start and finish with successful and disastrous En Primeur campaigns, in this case the 2005 and 2010.

Slide 8

So where are we now? After 17 months of consecutive falls, the Liv-ex 100 has recently risen for three months in a row. As this chart shows, despite these small gains, two year and five year returns are amongst the lowest in the last 25 years and are well below trend of between 9% and 11% in nominal terms, depending on whose numbers you use.

Slide 9

As we know, Bordeaux and the First Growths in particular are the main vehicles of choice for speculative activity thanks to the relative size of the market. As this chart shows, both Bordeaux and First Growths as a percentage of Liv-ex trade are currently at the lowest levels in a decade.

Slide 10

Against other assets, this time US equities, bonds and top New York property (perhaps a better benchmark for the Hong Kong collector), fine wine has also dramatically underperformed, suggesting that in relative terms fine wine may be good value.

Slide 11

If final consumers from Hong Kong and China have been the most influential for fine wine in recent years, then this chart also holds cause for optimism. I like to use Hong Kong import numbers from the UK as a good proxy for fine wine demand in Hong Kong and China. You can see the correlation on this chart between demand and prices. After two years of sharply falling imports in 2012 and 2013, imports are up 8% this year.

Slide 12

As always, what is required to kick-start a fine wine cycle is a successful En Primeur campaign, by which I mean a financially rewarding one for the supply chain which includes the negociant, the international trade and the consumer.

As this chart shows, in too many recent campaigns the lion's share of the profits has gone to the Chateau: from 2010 onwards 90% or more, which clearly leaves very little on the table for anybody else. In my mind, after three – arguably four – failed campaigns, 2014 just has to work and prices will have to fall further than many in Bordeaux currently appreciate.

Slide 13

Finally, if the cycle is bottoming out where does value lie? Well it is possible ironically that after four tough years the value lies in Bordeaux. Outside of Bordeaux the market has actually done pretty well since 2011, with most sub-indices of the Liv-ex 1000 Index up over the period. There has been a fairly orderly rotation from Bordeaux to Burgundy, then Champagne, then Italy and most recently the other leading wines in the rest of the world like Opus One, Penfolds Grange, Vega Sicilia, etc.

Slide 14

One of the biggest beneficiaries of Bordeaux's demise has been DRC, which has outperformed the Bordeaux First Growths by nearly 100% in price terms since 2010. For most of this period, this has been matched by increasing demand on Liv-ex. But interestingly, professional buyers appear to be shunning the wine in 2014. Trade is down about 60% this year, even as DRC has continued to outperform the Firsts. This divergence possibly leaves DRC looking a bit exposed.

Slide 15

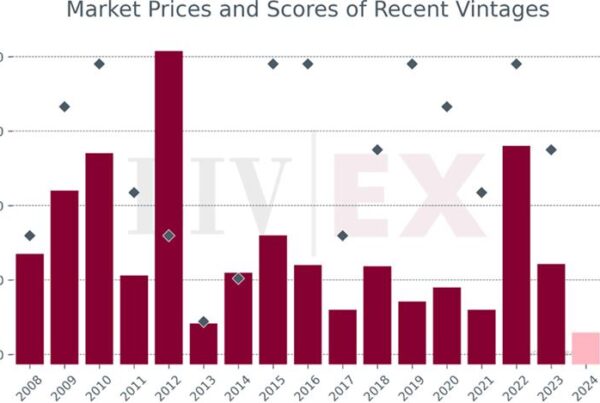

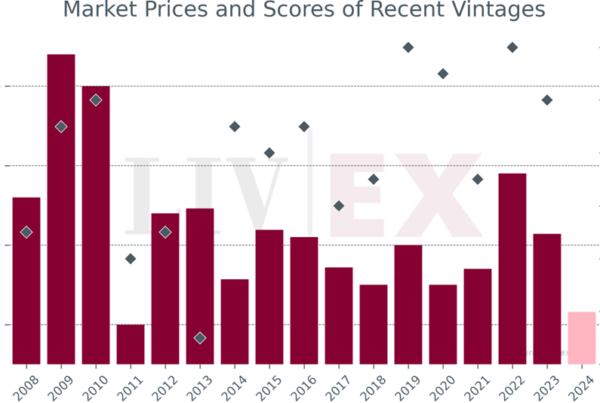

In contrast, many of the Bordeaux First Growths are trading at depressed levels. While Lafite still looks a bit high, wines like Haut Brion and Margaux are trading at close to their post-Lehman lows. It as though the China boom never happened.

Slide 16

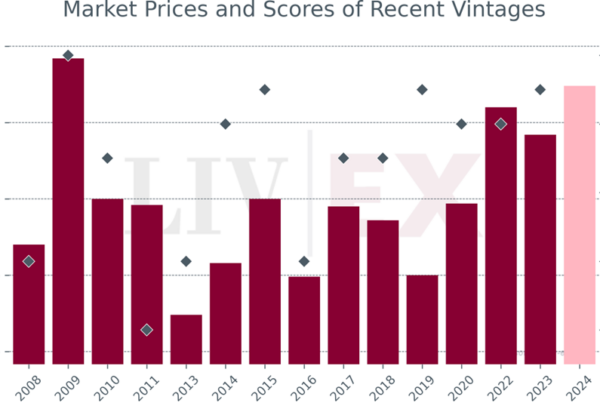

If we look more closely at the First Growths, it is interesting to note that in the last few years Haut Brion, in Robert Parker's view, has been consistently making the best wines, yet is trading at the lowest price. On a price to points basis, this makes Haut Brion look particularly attractive.

Slide 17

Another place to look may be Parker's so-called Magical 20 wines: a group of Bordeaux wines that Parker believes are of First Growth quality, but do not attract First Growth prices. As such, they are, in his words, "undervalued and very smart buys". Interestingly, these have done relatively well through the downturn and despite a sharp fall in Bordeaux trade on Liv-ex, have continued to find buyers.

Slide 18

To conclude, it seems far more likely than not that the ancient cycle of boom and bust is set to continue.

Apart from anything else, speculation plays a vital role in helping to set prices. This attracts a lot of interest and liquidity to fine wine, legitimises many peoples’ passion and allows growers the luxury of making age-worthy wines. Without the prospect of profit, merchants and consumers would be unlikely to buy and effectively provide the finance for wines that can take several decades to mature.

After four years of falling prices, the Bordeaux market is at its lowest ebb since possibly the early 1970s. As then, now may prove to be a good time to enter the market – but a well-priced 2014 vintage is a vital precursor to any kind of sustained recovery. It will be the return to sensible pricing and an environment where everybody wins buying En Primeur that will get Bordeaux out of its current rut.