May Market Report

- While April gave us a glimpse of sunshine, the May numbers remind us that spring often comes with rainy spells.

- Ahead of the 2023 En Primeur campaign buyers have been looking for back-vintage opportunities.

- With the influx of En Primeur 2023 scores, we look the few wines which contenders for perfect scores, and perhaps most tellingly, fewer still are the subject of broad consensus amongst critics.

- Are the Bordeaux 2023 price cuts enough to make up for a string of difficult campaigns?

- The Burgundy index has now dropped by over 20% from its peak and has declined for 14 consecutive months since March 2023 – what does a technical analyst have to say?

- Its good time to be a US buyer – Dollar strength provides buying opportunities.

Introduction

While April gave us a glimpse of sunshine, the May numbers remind us that spring often comes with rainy spells.

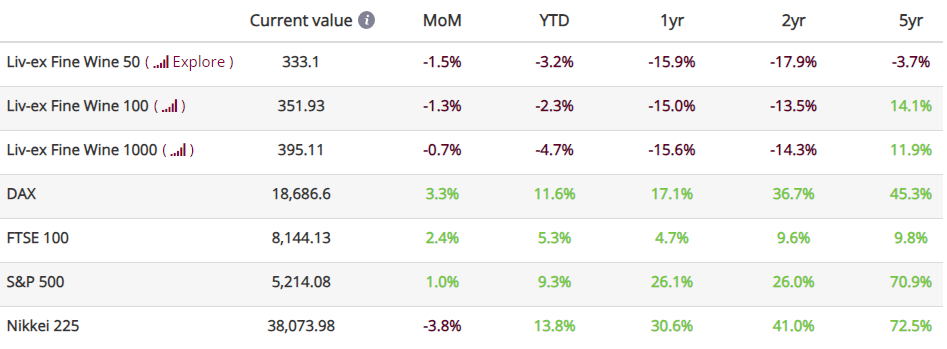

The Liv-ex Fine Wine 100, the industry benchmark fell 1.3% in April following its 0.4% rise in March. The Liv-ex Fine Wine 50, which tracks the movement of the First Growths and is updated daily, also fell 1.3% in April, a sharper drop than its 0.6% drop the previous month.

The Liv-ex Fine Wine 1000, which tracks 1,000 wines from across the world, fell 0.7% month-on-month, in line with its 0.6% fall in March. Of its sub-indices, the Italy 100 was the only one to record a positive movement, rising 0.7% month-on-month. The index has been one of the most resilient since the start of the year – it is only down 0.2% year-to-date.

The Bordeaux Legends 40 remained flat, while its counterpart tracking younger Bordeaux vintages, the Bordeaux 500, recorded a relatively modest fall of 0.6%. The Burgundy 150 and the Rhône 100 did not fare so well, falling 1.3% and 1.0% respectively.

While prices took a further tumble, the mood music in the market is not as sombre as the numbers suggest. Indeed, April saw a slight uptick in trade value and volume on Liv-ex, as well as in the number of labels (LWIN7s) and individual wines (LWIN11s) traded.

Will the En Primeur campaign deliver the prices, volumes and quality needed to further improve the mood?The early signs are not convincing.

Major Market Movers

The Great Bordeaux Run

The Liv-ex Fine Wine 100 closed March on a positive note, its first rise in 12 months, at which point many will have been hoping the downturn was over. May’s update, however, suggests we’re not out of the water yet.

If we’ve noted anything in the past year and a half of the bear market, it’s that in the face of adversity, buyers are quick to revert to safe bets. And in the fine wine market, there is no safer bet than Bordeaux.

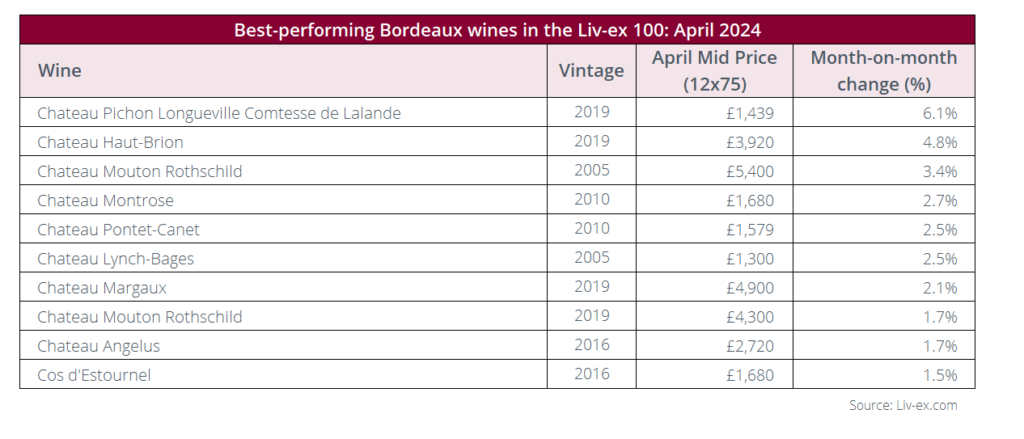

Last month, the Liv-ex 100 was partly buoyed by its Bordeaux components, most of which are from great vintages in the region (2005, 2009, 2010, 2016 and 2019). Ahead of the 2023 En Primeur campaign buyers have been looking for back-vintage opportunities.

The 2005s, for example, are now entering their drinking windows. The 2005 Château Mouton Rothschild boasts a 100-point score from Jane Anson (Inside Bordeaux) and has a Market Price of £5,300 per case. While its Market Price is 30.3% over the 2023’s release price, after factoring in 15-20 years of storage, insurance and opportunity costs, the difference isn’t so stark.

Château Montrose 2010 tells a similar story: it was awarded 100 points in 2023 by Lisa Perrotti-Brown MW (The Wine Independent) and Antonio Galloni (Vinous) and has a current Market Price of £1,765 per 12×75, only slightly up on the 2022’s release price of £1,746 per case.

Cos d’Estournel 2016 boasts 100 points from Neal Martin and a Market Price of £1,660 per case (25.6% below the 2022’s release price, which has a score of 95-97 points from the critic). Likewise, the 2016 vintage of Château Angelus is cheaper and scored higher by Neal Martin than its latest release, the 2023.

Even as the first salve of 2023 releases are delivering prices much lower than previous vintages, there is value to be found in older Bordeaux – some of which is mature enough to drink.

Critical Corner

2023 En Primeur scores – Agree to disagree?

The sudden influx of scores marking the start of the En Primeur can be dizzying. Who to trust, if anyone at all? While we’ve summarised individual reviewers’ scores in their own articles, below is a more general look at the 2023 vintage, as seen by the critics.

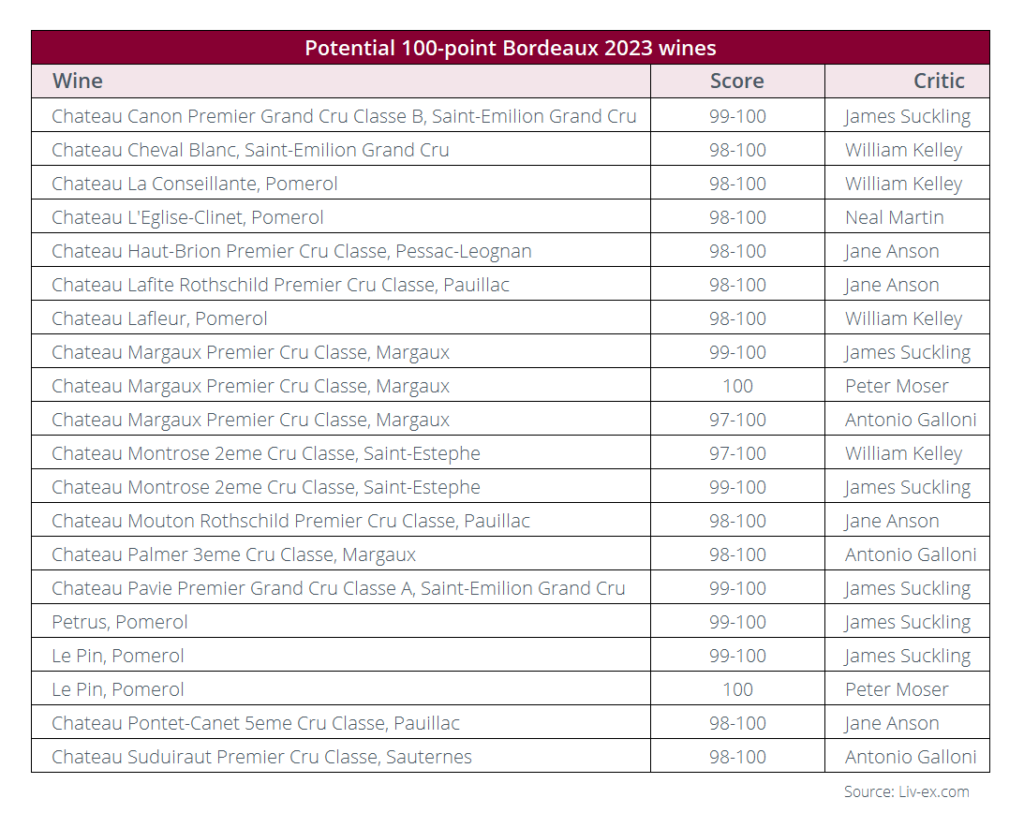

First, it’s worth noting that few wines are contenders for perfect scores, and perhaps most tellingly, fewer still are the subject of broad consensus amongst critics.

Château Margaux is one wine James Suckling, Peter Moser and Antonio Galloni all see the potential for perfection in, awarding it 99-100 points, 100 points and 97-100 points respectively. It was also rated as the favourite 2023 wine by the trade. Le Pin was another favourite of Peter Moser’s and James Suckling’s, and William Kelley and James Suckling see recognised Château Montrose as a contender for 100 points.

Neal Martin only ventured to grant a potential 100-point score to Château L’Eglise-Clinet, while Jane Anson chose Château Haut-Brion, Château Lafite and Château Pontet-Canet. William Kelley has four potential 100-pointers in Château Cheval Blanc, Château La Conseillante, Château Lafleur and Montrose, while Antonio Galloni picked out Margaux and a Sauternes, Château Suduiraut.

As critics struggled to align on their vintage favourites, which wines were the most divisive? The table below shows the wines with the biggest variance in their median scores*.

Château Cantemerle’s median scores were separated by 9.5 points, having received 93-94 points from James Suckling but just 83-85 points from Lisa Perrotti-Brown MW.

It seems 2023 whites were particularly divisive. Château Filhot was the wine that divided opinion the most: Neal Martin scored the wine a range of 82-85 points while Jane Anson gave it a high score of 94 points. Pavillon Blanc du Château Margaux, recieved 88-90 points from Neal Martin, but 96-97 points from James Suckling. Yohan Castaing awarded Cos d’Estournel Blanc 90-92 points while James Suckling gave it 97-98 points.

Domaine de Chevalier Blanc was awarded 97-98 points by James Suckling, compared to just 90 points from Rod Smith. Its red counterpart was also scored 97-98 points by James Suckling and just 91 points by Rod Smith.

This is clearly not a homogenous vintage and even the ‘snow-capped peaks’ (to borrow Neal Martin’s metaphor) were unable to unite the critics.

*This was calculated by taking the median point in every score collected from Vinous, Inside Bordeaux, The Wine Independent, The Wine Advocate, Falstaff, James Suckling, Tim Atkin, Jean Marc Quarin and The Drinks Business. For each wine, the variation was then considered between its highest and lowest median scores.

News Insight

The En Primeur pricing predicament

We’ve looked at the 2023’s scores, but what of their prices? Well, as many had predicted (hoped?), they are considerably down year-on-year across the board.

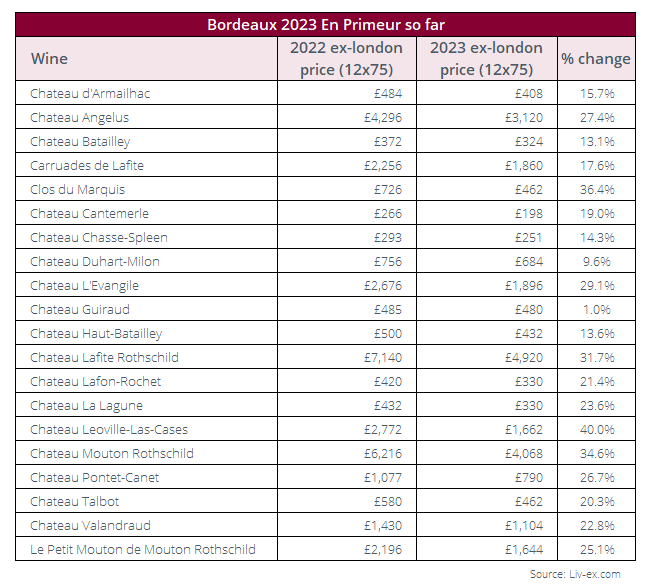

Château Léoville-Las-Cases led the way with the biggest price cut – the 2023 vintage released at £1,662 per case, down 40.0% down the 2022’s release price. Clos du Marquis 2023 was close behind with a release price down 36.4% on the previous year.

First Growth Château Mouton Rothschild 2023 was released 34.6% below the 2022 vintage, at £4,068 per 12×75 while Château Lafite Rothschild’s 2023 release price was 31.7% down on the previous vintage.

Château Guiraud, on the other hand, was released a conservative 1.0% below the 2022’s release price, while Château Duhart-Milon was released just 9.6% below the previous vintage.

So far, releases are on average 22.2% lower than the 2022s. While that goes a long way towards making prices more palatable for En Primeur buyers, let us remind ourselves that 2022 En Primeur prices were 20.8% over the 2021s by the end of the campaign so on average, we’re back where we were two years ago.

While the 2023s are widely considered to be of higher quality than the 2021s, will buyers happily pay prices many weren’t comfortable with two years ago, at the height of the fine wine market boom? Are these price cuts enough to make up for a string of difficult campaigns? The campaign so far has yielded mixed results – next week could be crucial as the volume of releases picks up pace. Hold tight.

Chart of the Month

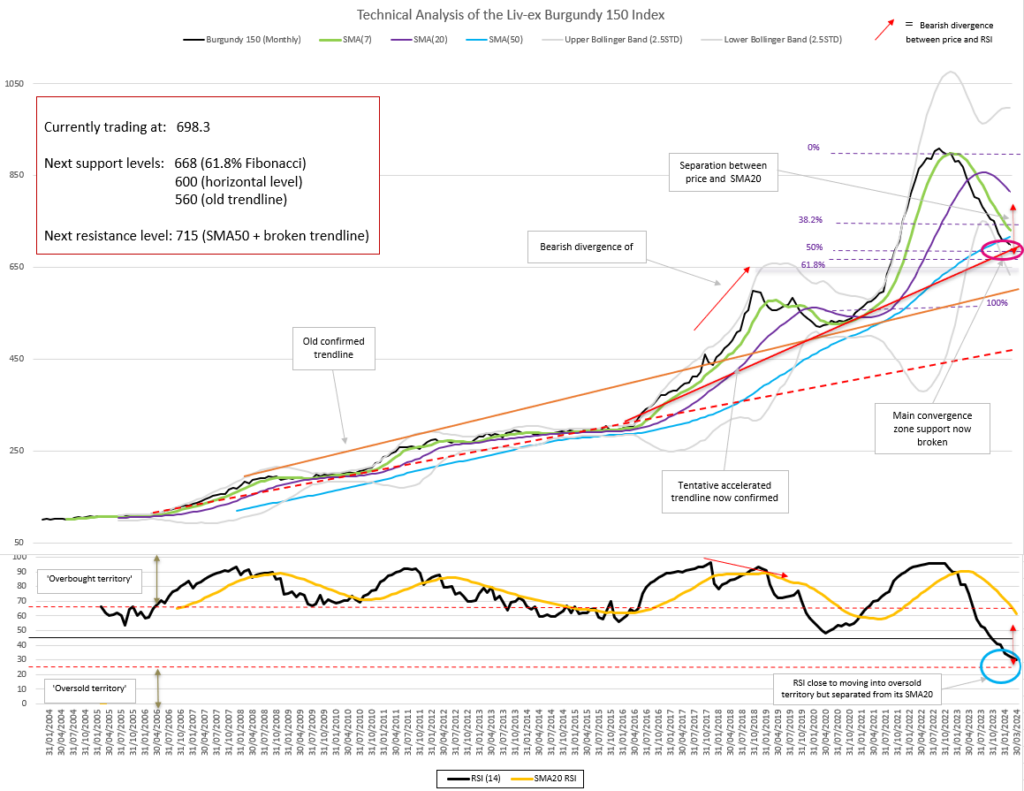

The end of the bull run for the Burgundy 150?

In our September 2023 update, we warned that the Burgundy 150’s long-term bullish trend was becoming more fragile, but was by no means invalidated. Yet.

As a reminder, we noted that proponents of technical analysis would consider a break below the Simple Moving Average 50-Months (SMA50) a more serious threat to the long-term trend, especially if accompanied by a break below the rising tentative accelerated trend line (the ‘main convergence zone’ circled on the chart).

The price has now reached these levels and broken them both. As a result, the tentative accelerated trendline stemming from the 2016 lows (in red on the chart above) was validated. Even though the price is currently only a few points below these support-become-resistance levels, it sends a bearish signal, at least in the short-term.

The index has now dropped by over 20% from its peak and has declined for 14 consecutive months since March 2023. The price has been riding its SMA7 downwards and looks set to continue to do so if the widely-open Bollinger Bands (BB) are anything to go by; as an indicator, they potentially signal the start of a strong price trend.

Technical analysis suggests that momentum is very bearish. This is evidenced by the recent short-term trend in the price and in the Relative Strength Index (RSI). The price looks ‘separated’ from its SMA20 (i.e. there is an unusually large distance between them), while the RSI is separated from its own SMA20. The RSI is also on the verge of the oversold territory, which could trigger a reaction.

Proponents of technical analysis would favour 600 (the 2019 highs) as the next major support level for the price. We will also monitor a possible reaction on the 61.8% Fibonacci retracement level, at 668. However, a move up isn’t impossible, even temporarily; at some point in the next six months, the index may re-test the broken trendline.

The invalidation of the current downward move would at the very least require the price breaking the newly-validated trendline at 715 and the SMA7. In light of the current indicators, technical analysis suggests that this is not the likeliest scenario.

Final Thought

It’s a good time to be a US buyer

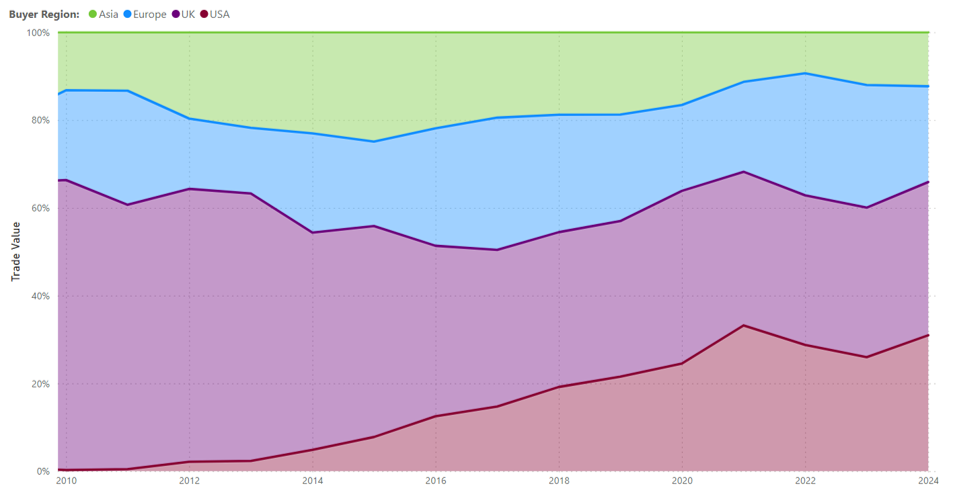

Over the last 15 years, US buyers have been increasing their proportion of trade on the secondary market in the last 15 years, rising from less than 1% in 2010 to nearly 30% of the total so far in 2024.

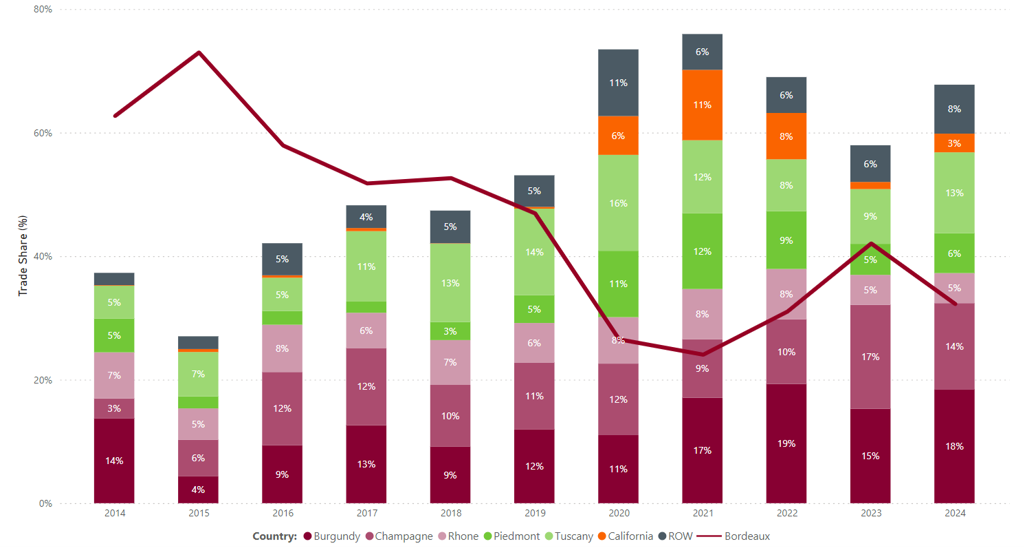

But what have US buyers been filling their boots with? The chart below shows their evolving buying patterns over the last ten years.

Interestingly, while Californian wines accounted for 11.0% of US buying back in 2021, they have since decreased to just 3.0% in 2024 to date.

Bordeaux recorded a gradual fall from grace from 2015, dropping from close to 75.0% of US trade to just over 20.0%, but has since risen back to over 40.0% of total US buying in 2023, at a time when buyers were banking on safe bets amid market uncertainty.

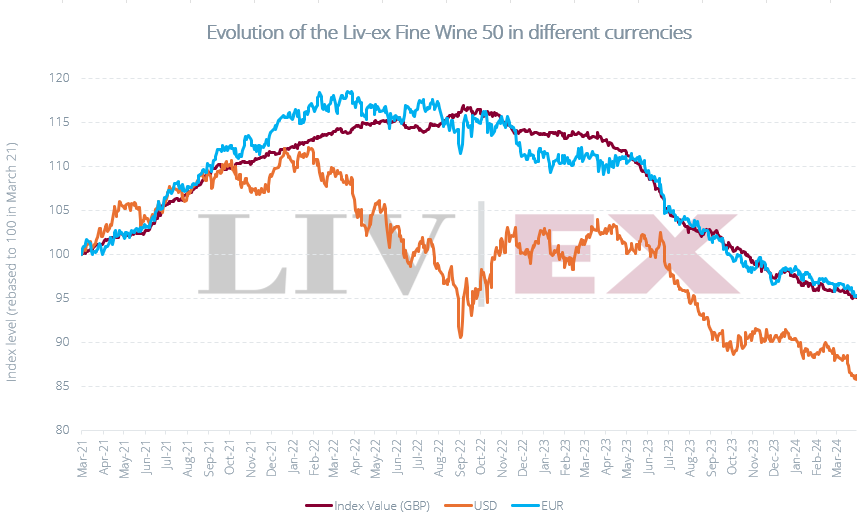

The strength of the US dollar has certainly helped. Looking at the Liv-ex Fine Wine 50, which tracks the price movement of First Growths, in different currencies, its wines are close to 10% cheaper for buyers in USD than those paying in EUR or GBP.

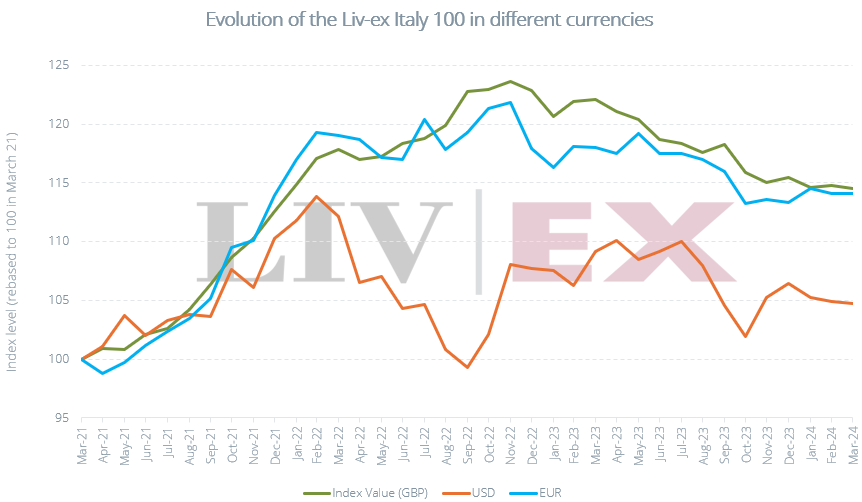

Likewise, US buyers of Italian wines, which have accounted for 19.0% of US trade since the start of 2024, are paying much less than their counterparts who use Euros and Pound Sterling. The Liv-ex Italy 100 in USD sits 10 points lower than its equivalent in GBP or EUR.

‘Buying the dip’ in USD terms could prove a very worthwhile strategy. All buyers (including those buying in US dollars) have access to £99.4 of live offers on Liv-ex.